Advertisement

- United States

- /

- Electrical

- /

- OTCPK:CGEH

Is Capstone Turbine (NASDAQ:CPST) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Capstone Turbine Corporation (NASDAQ:CPST) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Capstone Turbine

What Is Capstone Turbine's Net Debt?

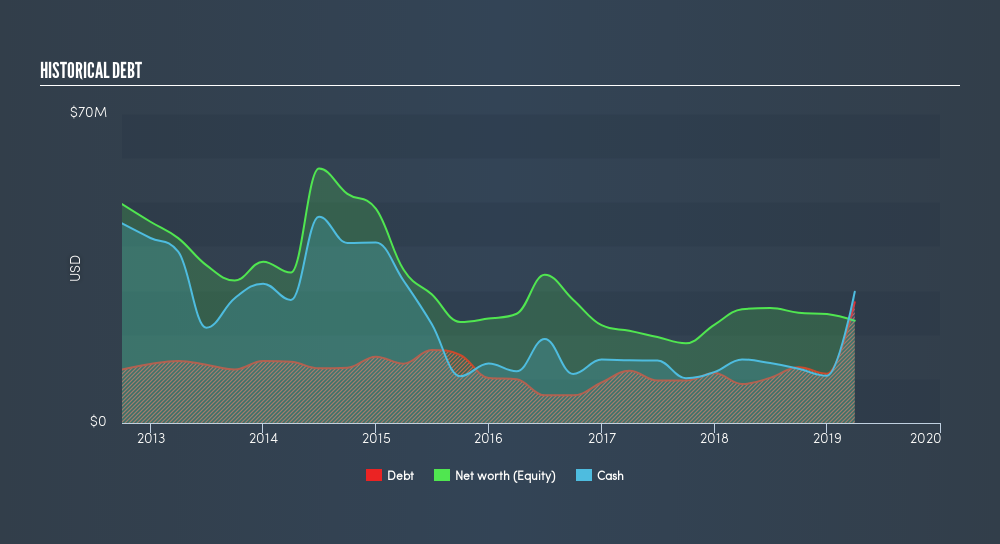

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Capstone Turbine had US$27.3m of debt, an increase on US$8.85m, over one year. But it also has US$29.7m in cash to offset that, meaning it has US$2.39m net cash.

How Strong Is Capstone Turbine's Balance Sheet?

The latest balance sheet data shows that Capstone Turbine had liabilities of US$28.1m due within a year, and liabilities of US$28.7m falling due after that. Offsetting this, it had US$29.7m in cash and US$16.2m in receivables that were due within 12 months. So its liabilities total US$10.9m more than the combination of its cash and short-term receivables.

Capstone Turbine has a market capitalization of US$50.8m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. Despite its noteworthy liabilities, Capstone Turbine boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Capstone Turbine's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Capstone Turbine saw its revenue hold pretty steady. While that hardly impresses, its not too bad either.

So How Risky Is Capstone Turbine?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Capstone Turbine lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$21m and booked a US$17m accounting loss. But at least it has US$30m on the balance sheet to spend on growth, near-term. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. For riskier companies like Capstone Turbine I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OTCPK:CGEH

Capstone Energy+

Provides customized microgrid solutions, on-site resilient energy-as-a-service (EaaS) solutions, and on-site energy technology systems.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4352.0% undervalued

76 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

25 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.7% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on DIGITAL HEARTS HOLDINGS ·

Strategic pivot in maximizing corporate value

Fair Value:JP¥928.1618.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Sanyo Trading ·

Delivering steady performance

Fair Value:JP¥1.59k2.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BI

birdflustocks on Arcturus Therapeutics Holdings ·

Arcturus Therapeutics: Strategic opportunities beyond CSL

Fair Value:US$3076.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.1% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6118.3% undervalued

1195 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

25 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative