Advertisement

- Germany

- /

- Commercial Services

- /

- DB:GBF

Is Bilfinger SE (FRA:GBF) Growing Too Fast?

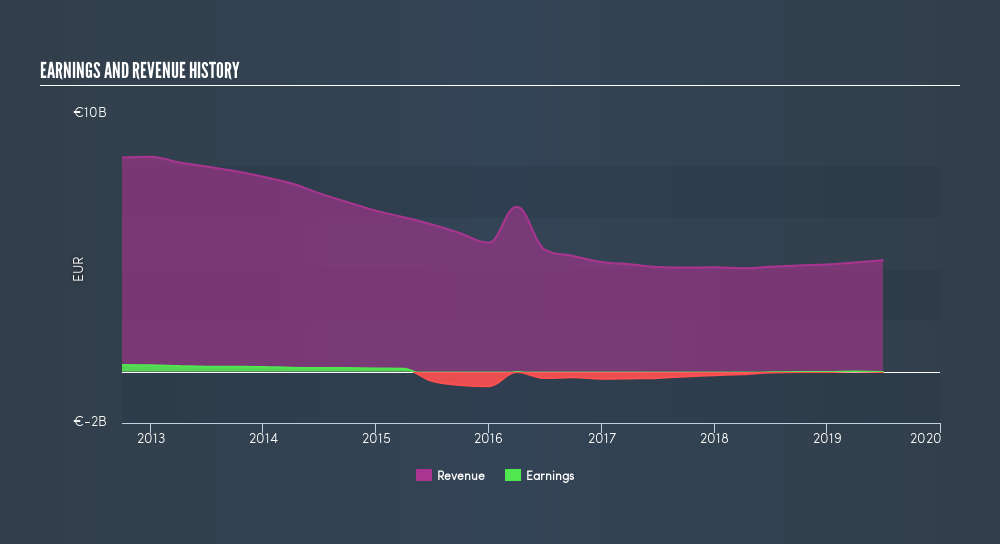

Trailing twelve-month data shows us that Bilfinger SE's (FRA:GBF) earnings loss has accumulated to -€23.1m. Although some investors expected this, their belief in the path to profitability for Bilfinger may be wavering. The single most important question to ask when you’re investing in a loss-making company is – will it need to raise cash again, and if so, when? This is because new equity from additional capital raising can thin out the value of current shareholders’ stake in the company. Given that Bilfinger is spending more money than it earns, it will need to fund its expenses via external sources of capital. Looking at Bilfinger’s latest financial data, I will estimate when the company may run out of cash and need to raise more money.

View our latest analysis for Bilfinger

What is cash burn?

With a negative free cash flow of -€83.4m, Bilfinger is chipping away at its €837m cash reserves in order to run its business. The biggest threat facing Bilfinger investors is the company going out of business when it runs out of money and cannot raise any more capital. Bilfinger operates in the diversified support services industry, which delivered positive earnings in the past year. This means, on average, its industry peers are profitable. Bilfinger runs the risk of running down its cash supply too fast, or falling behind its profitable peers by investing too little.

When will Bilfinger need to raise more cash?

We can measure Bilfinger's ongoing cash expenditure requirements by looking at free cash flow, which I define as cash flow from operations minus fixed capital investment, is a measure of how much cash a company generates/loses each year.

In the past year, free cash outflows (excluding one-offs) rose by 39%, which is high. However, given the current levels of cash holdings, it seems that Bilfinger will not need further capital soon. The company may be able to continue investing at the same rate without having to issue equity or borrow within the next three years. Although this is a relatively simplistic calculation, and Bilfinger could reduce its costs or borrow money instead of raising new equity capital, the outcome of this analysis still helps us understand how sustainable the Bilfinger operation is, and when things may have to change.

Next Steps:

Although Bilfinger’s cash burn is growing at a double-digit rate, investors can breathe easy knowing it probably won’t be raising money any time soon. This should be good news for current shareholders as there is less of a chance that their current shares will be diluted, and it also indicates the company doesn’t have an immediate cash problem on its hand. Now that we’ve accounted for cash burn growth, you should also look at expected revenue growth in order to gauge when the company may become breakeven. I admit this is a fairly basic analysis for GBF's financial health. Other important fundamentals need to be considered as well. I recommend you continue to research Bilfinger to get a more holistic view of the company by looking at:- Future Outlook: What are well-informed industry analysts predicting for GBF’s future growth? Take a look at our free research report of analyst consensus for GBF’s outlook.

- Valuation: What is GBF worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether GBF is currently mispriced by the market.

- Other High-Performing Stocks: If you believe you should cushion your portfolio with something less risky, scroll through our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 30 June 2019. This may not be consistent with full year annual report figures. Operating expenses include only SG&A and one-year R&D.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About DB:GBF

Bilfinger

Provides industrial services to customers in the process industry primarily in Europe, North America, and the Middle East.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

159 followersusers have followed this narrative

0 commentsusers have commented on this narrative

27 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

JR

JRY on Bloom Energy ·

The Bloom Story is early days

Fair Value:US$386.143.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CH

ChuckN on NextEra Energy ·

Investor Thesis: Why the NextEra Energy / Dominion Energy Merger Could Be a Major AI Power Infrastructure Event

Fair Value:US$93.719.7% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.1% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

283 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

143 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

167 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0