Advertisement

- United States

- /

- Machinery

- /

- NYSE:ITW

Illinois Tool Works Inc. Just Released Its Yearly Earnings: Here's What Analysts Think

As you might know, Illinois Tool Works Inc. (NYSE:ITW) recently reported its full-year numbers. Illinois Tool Works reported in line with analyst predictions, delivering revenues of US$14b and statutory earnings per share of US$7.74, suggesting the business is executing well and in line with its plan. This is an important time for investors, as they can track a company's performance in its report, look at what top analysts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what analysts are expecting for next year.

Check out our latest analysis for Illinois Tool Works

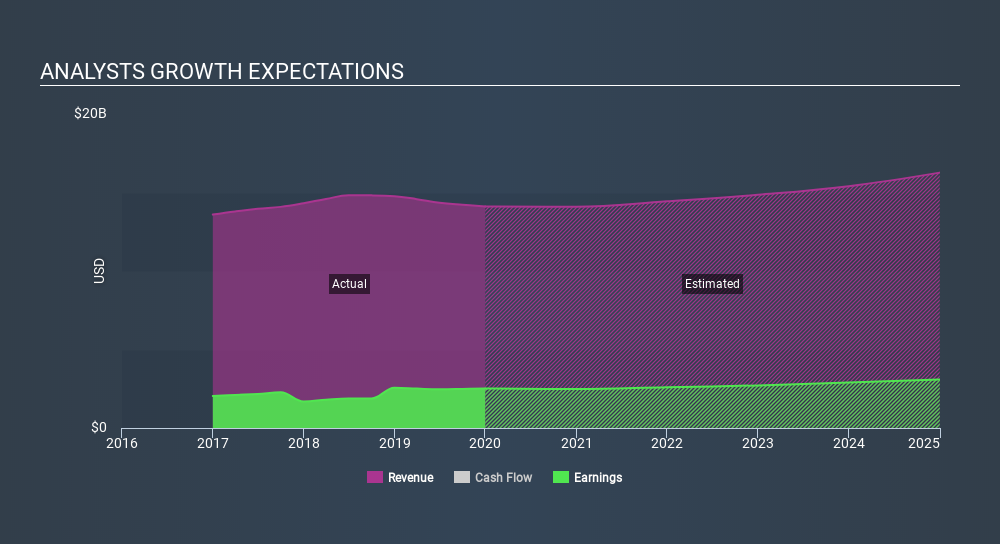

Following last week's earnings report, Illinois Tool Works's 15 analysts are forecasting 2020 revenues to be US$14.1b, approximately in line with the last 12 months. Statutory per share are forecast to be US$7.88, approximately in line with the last 12 months. In the lead-up to this report, analysts had been modelling revenues of US$14.2b and earnings per share (EPS) of US$7.99 in 2020. So it's pretty clear that, although analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

It will come as no surprise then, to learn that the consensus price target is largely unchanged at US$168. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Illinois Tool Works analyst has a price target of US$208 per share, while the most pessimistic values it at US$121. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Illinois Tool Works shareholders.

It can be useful to take a broader overview by seeing how analyst forecasts compare, both to the Illinois Tool Works's past performance and to peers in the same market. These estimates imply that sales are expected to slow, with a forecast revenue decline of 0.1% a significant reduction from annual growth of 1.2% over the last five years. Compare this with our data, which suggests that other companies in the same market are, in aggregate, expected to see their revenue grow 1.6% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - analysts also expect Illinois Tool Works to grow slower than the wider market.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with analysts reconfirming that earnings per share are expected to continue performing in line with their prior expectations. Fortunately, analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that Illinois Tool Works's revenues are expected to perform worse than the wider market. The consensus price target held steady at US$168, with the latest estimates not enough to have an impact on analysts' estimated valuations.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have estimates - from multiple Illinois Tool Works analysts - going out to 2024, and you can see them free on our platform here.

You can also see whether Illinois Tool Works is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:ITW

Illinois Tool Works

Provides industrial products and equipment in North America, Europe, the Middle East, Africa, the Asia Pacific, and South America.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.562.2% undervalued

33 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.6% overvalued

39 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.9% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

TI

TimLee on Master Tec Group Berhad ·

Master Tec’s TNB Extension Reinforces Its Utility-Scale Growth Story

Fair Value:RM 1.6841.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on Judo Capital Holdings ·

A Fast-Growing SME Lender Trading Like a Problem Bank

Fair Value:AU$0.954.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on Weebit Nano ·

A Semiconductor Bet Moving From Science Project to Commercial Story

Fair Value:AU$8.7514.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.4% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.5% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative