Advertisement

- Poland

- /

- Specialty Stores

- /

- WSE:MDV

Here's Why We Think CCC's (WSE:CCC) Statutory Earnings Might Be Conservative

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. That said, the current statutory profit is not always a good guide to a company's underlying profitability. In this article, we'll look at how useful this year's statutory profit is, when analysing CCC (WSE:CCC).

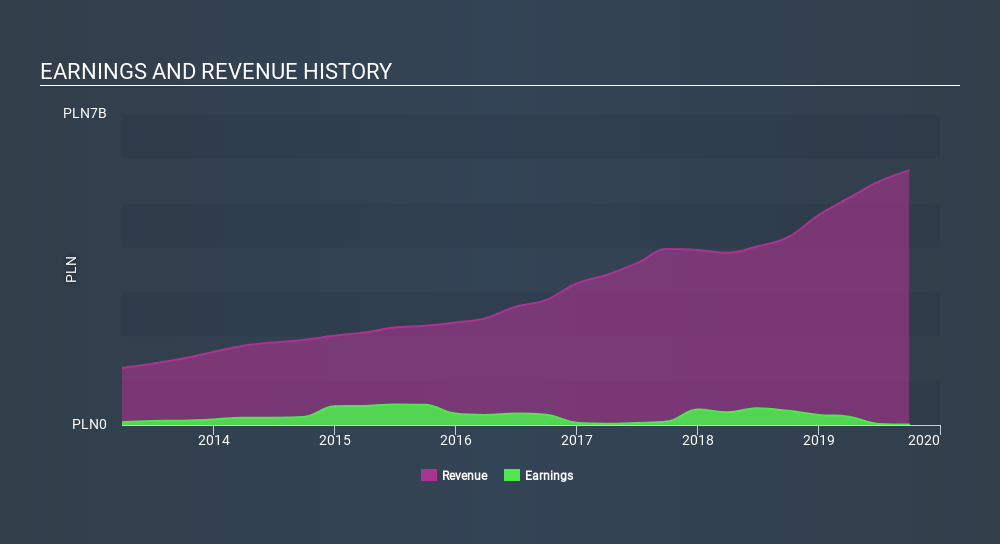

While CCC was able to generate revenue of zł5.73b in the last twelve months, we think its profit result of zł8.90m was more important. While it managed to grow its revenue over the last three years, its profit has moved in the other direction, as you can see in the chart below.

Check out our latest analysis for CCC

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. Today, we'll discuss CCC's free cashflow relative to its earnings, and consider what that tells us about the company. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

A Closer Look At CCC's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

CCC has an accrual ratio of -0.27 for the year to September 2019. That implies it has very good cash conversion, and that its earnings in the last year actually significantly understate its free cash flow. In fact, it had free cash flow of zł524m in the last year, which was a lot more than its statutory profit of zł8.90m. CCC's free cash flow improved over the last year, which is generally good to see.

Our Take On CCC's Profit Performance

Happily for shareholders, CCC produced plenty of free cash flow to back up its statutory profit numbers. Because of this, we think CCC's underlying earnings potential is as good as, or possibly even better, than the statutory profit makes it seem! On the other hand, its EPS actually shrunk in the last twelve months. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Ultimately, this article has formed an opinion based on historical data. However, it can also be great to think about what analysts are forecasting for the future. Luckily, you can check out what analysts are forecsting by clicking here.

Today we've zoomed in on a single data point to better understand the nature of CCC's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About WSE:MDV

Modivo

Engages in the retail sale of footwear and other products in Poland, Central and Eastern Europe, and Western Europe.

High growth potential and fair value.

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$470.5% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.251.3% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Discovery Silver ·

#1 Silver Play with Positive Cashflow Gold Miner (Top Notch Team)

Fair Value:CA$7087.7% undervalued

54 followersusers have followed this narrative

16 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Hangzhou Oxygen Plant Group ·

The company must capitalize on its R&D&I over the next 10 years; it is still too early to infer the outcome.

Fair Value:CN¥24.481.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Sinopec Shanghai Petrochemical ·

Capital expenditures remain required regardless of profitability

Fair Value:HK$0.32259.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.4% undervalued

122 followersusers have followed this narrative

2 commentsusers have commented on this narrative

34 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative