Here's How We Evaluate Hong Leong Financial Group Berhad's (KLSE:HLFG) Dividend

Is Hong Leong Financial Group Berhad (KLSE:HLFG) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. Yet sometimes, investors buy a popular dividend stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

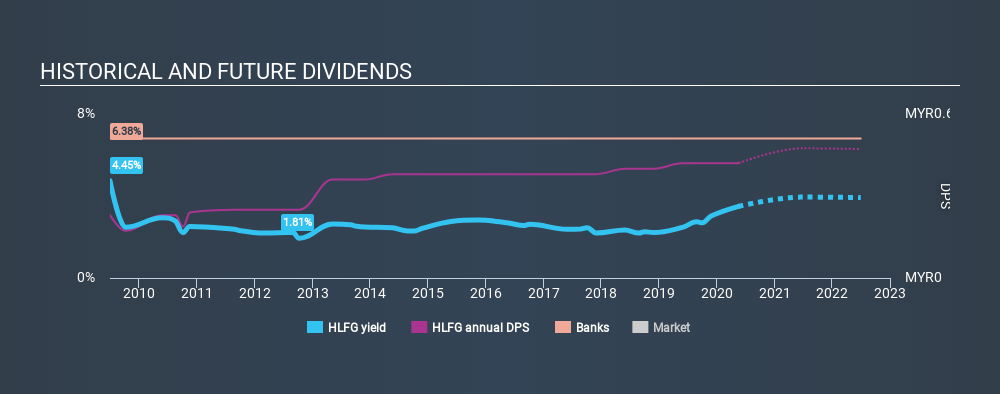

A high yield and a long history of paying dividends is an appealing combination for Hong Leong Financial Group Berhad. We'd guess that plenty of investors have purchased it for the income. The company also returned around 1.1% of its market capitalisation to shareholders in the form of stock buybacks over the past year. There are a few simple ways to reduce the risks of buying Hong Leong Financial Group Berhad for its dividend, and we'll go through these below.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. Looking at the data, we can see that 25% of Hong Leong Financial Group Berhad's profits were paid out as dividends in the last 12 months. Given the low payout ratio, it is hard to envision the dividend coming under threat, barring a catastrophe.

We update our data on Hong Leong Financial Group Berhad every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. Hong Leong Financial Group Berhad has been paying dividends for a long time, but for the purpose of this analysis, we only examine the past 10 years of payments. Its dividend payments have declined on at least one occasion over the past ten years. During the past ten-year period, the first annual payment was RM0.23 in 2010, compared to RM0.42 last year. This works out to be a compound annual growth rate (CAGR) of approximately 6.2% a year over that time. The dividends haven't grown at precisely 6.2% every year, but this is a useful way to average out the historical rate of growth.

A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. While there may be fluctuations in the past , Hong Leong Financial Group Berhad's earnings per share have basically not grown from where they were five years ago. Flat earnings per share are acceptable for a time, but over the long term, the purchasing power of the company's dividends could be eroded by inflation. So, we know earnings growth has been thin on the ground. However, at least the payout ratio is conservative, and there is plenty of potential to increase this over time.

Conclusion

To summarise, shareholders should always check that Hong Leong Financial Group Berhad's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. Firstly, we like that Hong Leong Financial Group Berhad has a low and conservative payout ratio. Second, earnings have been essentially flat, and its history of dividend payments is chequered - having cut its dividend at least once in the past. Hong Leong Financial Group Berhad might not be a bad business, but it doesn't show all of the characteristics we look for in a dividend stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 2 warning signs for Hong Leong Financial Group Berhad that investors should take into consideration.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About KLSE:HLFG

Hong Leong Financial Group Berhad

An investment holding company, provides investment banking, stockbroking, and fund management business of financial services to consumer, corporate, and institutional customers.

Undervalued with excellent balance sheet and pays a dividend.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)