Advertisement

Here's How P/E Ratios Can Help Us Understand Banco Santander, S.A. (BME:SAN)

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

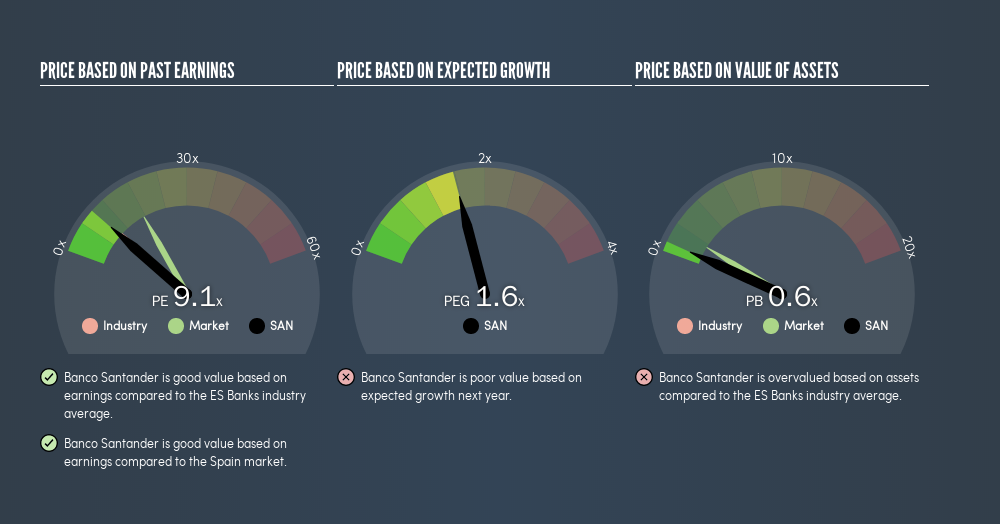

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). We'll apply a basic P/E ratio analysis to Banco Santander, S.A.'s (BME:SAN), to help you decide if the stock is worth further research. Banco Santander has a price to earnings ratio of 9.12, based on the last twelve months. That means that at current prices, buyers pay €9.12 for every €1 in trailing yearly profits.

See our latest analysis for Banco Santander

How Do I Calculate Banco Santander's Price To Earnings Ratio?

The formula for P/E is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Banco Santander:

P/E of 9.12 = €3.95 ÷ €0.43 (Based on the year to March 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each €1 of company earnings. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

How Growth Rates Impact P/E Ratios

P/E ratios primarily reflect market expectations around earnings growth rates. When earnings grow, the 'E' increases, over time. That means even if the current P/E is high, it will reduce over time if the share price stays flat. Then, a lower P/E should attract more buyers, pushing the share price up.

Banco Santander saw earnings per share improve by -7.0% last year. And its annual EPS growth rate over 5 years is 2.4%.

How Does Banco Santander's P/E Ratio Compare To Its Peers?

We can get an indication of market expectations by looking at the P/E ratio. As you can see below Banco Santander has a P/E ratio that is fairly close for the average for the banks industry, which is 9.7.

Its P/E ratio suggests that Banco Santander shareholders think that in the future it will perform about the same as other companies in its industry classification. If the company has better than average prospects, then the market might be underestimating it. Checking factors such as the tenure of the board and management could help you form your own view on if that will happen.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. In other words, it does not consider any debt or cash that the company may have on the balance sheet. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

So What Does Banco Santander's Balance Sheet Tell Us?

Net debt totals a substantial 112% of Banco Santander's market cap. This level of debt justifies a relatively low P/E, so remain cognizant of the debt, if you're comparing it to other stocks.

The Verdict On Banco Santander's P/E Ratio

Banco Santander trades on a P/E ratio of 9.1, which is below the ES market average of 17.5. The meaningful debt load is probably contributing to low expectations, even though it has improved earnings recently.

When the market is wrong about a stock, it gives savvy investors an opportunity. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

But note: Banco Santander may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About BME:SAN

Banco Santander

Provides various financial products and services to individuals, small and medium-sized enterprises, large corporations, and public entities worldwide.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor