Advertisement

- India

- /

- Consumer Finance

- /

- NSEI:CHOLAFIN

Cholamandalam Investment and Finance Company Limited (NSE:CHOLAFIN): Can Growth Justify Its September Share Price?

Cholamandalam Investment and Finance Company Limited (NSE:CHOLAFIN) closed yesterday at ₹276.45, which left some investors asking whether the high earnings potential can still be justified at this price. Below I will be talking through a basic metric which will help answer this question.

Check out our latest analysis for Cholamandalam Investment and Finance

Where's the growth?

Investors in Cholamandalam Investment and Finance have been patiently waiting for the uptick in earnings. If you believe the analysts covering the stock then the following year will be very interesting. The consensus forecast from 16 analysts is certainly positive with earnings forecasted to rise significantly from today's level of ₹15.752 to ₹25.041 over the next three years. On average, this leads to a growth rate of 15% each year, which signals a market-beating outlook in the upcoming years.

Is CHOLAFIN available at a good price after accounting for its growth?

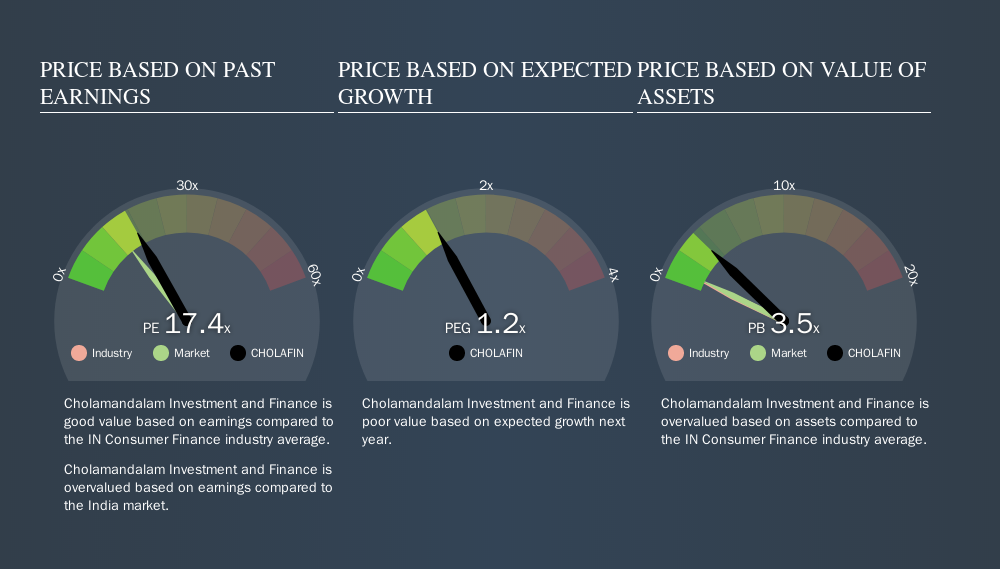

Cholamandalam Investment and Finance is available at price-to-earnings ratio of 17.44x, showing us it is overvalued based on current earnings compared to the Consumer Finance industry average of 16.9x , and overvalued compared to the IN market average ratio of 13.71x .

We understand CHOLAFIN seems to be overvalued based on its current earnings, compared to its industry peers. However, to be able to properly assess the value of a high-growth stock such as Cholamandalam Investment and Finance, we must incorporate its earnings growth in our valuation. The PEG ratio is a great calculation to take account of growth in the stock's valuation. A PE ratio of 17.44x and expected year-on-year earnings growth of 15% give Cholamandalam Investment and Finance an acceptable PEG ratio of 1.19x. Based on this growth, Cholamandalam Investment and Finance's stock can be considered slightly overvalued , based on fundamental analysis.

What this means for you:

CHOLAFIN's current overvaluation could signal a potential selling opportunity to reduce your exposure to the stock, or it you're a potential investor, now may not be the right time to buy. However, basing your investment decision off one metric alone is certainly not sufficient. There are many things I have not taken into account in this article and the PEG ratio is very one-dimensional. If you have not done so already, I highly recommend you to complete your research by taking a look at the following:

- Financial Health: Are CHOLAFIN’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

- Past Track Record: Has CHOLAFIN been consistently performing well irrespective of the ups and downs in the market? Go into more detail in the past performance analysis and take a look at the free visual representations of CHOLAFIN's historicals for more clarity.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:CHOLAFIN

Cholamandalam Investment and Finance

Operates as a non-banking finance company in India.

High growth potential second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor