Last Update 07 Jun 26

Fair value Decreased 14%INUV: AI Monetization And Restructuring Will Drive Future Upside Potential

Analysts have reduced their fair value estimate for Inuvo from $5.29 to $4.55, reflecting lower price targets that cite recent Q1 weakness, business restructuring, and increased reliance on monetizing IntentKey and improving margins over time.

Analyst Commentary

Bullish Takeaways

- Bullish analysts see a path to sustainable growth and profitability, even though the business is currently smaller. They factor this into their long term investment cases.

- Some are encouraged by management's efforts to monetize IntentKey and view successful execution in this area as a potential support for higher long term valuations.

- Despite weaker Q1 conditions, bullish analysts maintain positive ratings. This suggests they still see upside if restructuring efforts lead to better operating metrics over time.

- The reduced, but still supportive, price targets are presented as an attempt to balance current operational challenges with longer term growth potential.

Bearish Takeaways

- Bearish analysts highlight that Q1 results missed their estimates across nearly all metrics, which has led to lower price targets and more cautious ratings.

- There is concern that current financial weakness is directly tied to business restructuring, creating execution risk if margins do not improve as expected.

- Some view the investment case as increasingly dependent on management's ability to monetize IntentKey and stabilize margins, concentrating risk in a few key initiatives.

- Downgrades to more neutral ratings indicate that, for cautious analysts, the balance between near term operational pressure and potential longer term rewards has become less favorable.

What's in the News

- Inuvo announced an integration between its IntentKey platform and FreeWheel’s Buyer Cloud demand side platform, aiming to embed IntentKey’s artificial intelligence models directly into programmatic bidding logic. Source: Company client announcement.

- The FreeWheel integration is structured to let advertisers use IntentKey’s consumer intent signals in real time on each impression, based on predicted interest and relevance across open web content. Source: Company client announcement.

- Key features highlighted include embedded AI decisioning within bids, the ability to customize how AI is applied across campaigns, greater transparency into decisioning and performance, and a flexible API based setup for evolving programmatic media buying approaches. Source: Company client announcement.

- The collaboration is framed as giving advertisers more control, flexibility, and performance options as they set up and adjust AI driven programmatic strategies. Source: Company client announcement.

Valuation Changes

- Fair Value: reduced from $5.29 to $4.55, reflecting a lower central estimate for the stock's worth in current models.

- Discount Rate: risen slightly from 8.83% to 9.12%, indicating a modestly higher required return in the updated analysis.

- Revenue Growth: projected revenue trend has weakened, moving from a 5.83% decline to a 22.26% decline in the revised assumptions.

- Net Profit Margin: nudged higher from 11.39% to 12.04%, implying slightly stronger profitability assumptions on each dollar of revenue.

- Future P/E: increased from 12.47x to 18.18x, suggesting that the updated framework applies a higher earnings multiple to the stock.

Key Takeaways

- Accelerating adoption of Inuvo's privacy-focused, AI-driven platform positions the company for scalable, high-margin, and sustainable revenue growth in a shifting digital advertising landscape.

- Investments in compliance, direct client relationships, and omnichannel solutions enhance operational efficiency, client retention, and profitability amid expanding industry demand.

- Sustained unprofitability, heavy reliance on few partners, margin compression, competitive threats, and rapid industry changes all undermine Inuvo's revenue stability and long-term prospects.

Catalysts

About Inuvo- An advertising technology and services company, develops and commercializes large language generative artificial intelligence that discovers and targets digital audiences in the United States.

- Accelerating adoption of the self-serve IntentKey platform-evidenced by a 300% quarter-over-quarter increase in new deals-positions Inuvo to drive high-margin, scalable revenue growth as more clients expand their spend and mature on the platform.

- Inuvo's privacy-compliant, concept-based AI targeting receives strong validation from both independent AI assessments and client feedback, establishing the platform as a differentiated solution in a market increasingly prioritizing privacy-first digital advertising, which should support both revenue growth and enhanced net margins.

- Structural investments in compliance, transparent reporting, and content scalability (including rapid, AI-powered content creation and vertically specialized sites) prepare Inuvo to capitalize on industry trends favoring quality, compliant suppliers, likely translating to increased client acquisition, retention, and higher gross profits.

- Expansion of direct client relationships and new demand-side platform integrations reduce reliance on third-party intermediaries, set the stage for international growth, and improve operating leverage, which collectively should boost gross margins and earnings stability.

- The rapid growth in digital advertising budgets and ongoing industry transition to programmatic, omnichannel, and CTV channels (where Inuvo is seeing increasing success and higher margins) expands the company's addressable market and supports long-term, compounding revenue growth.

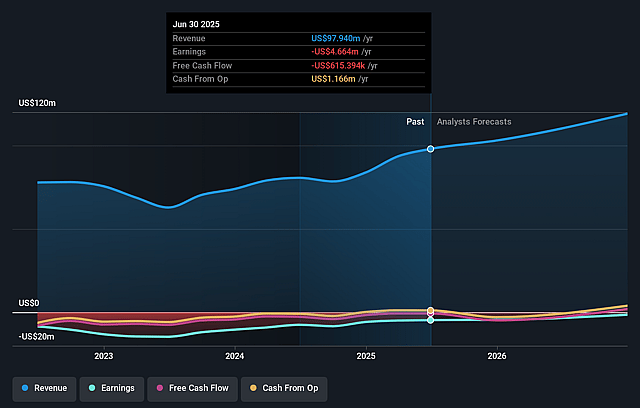

Inuvo Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Inuvo's revenue will decrease by 22.3% annually over the next 3 years.

- Analysts are not forecasting that Inuvo will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Inuvo's profit margin will increase from -5.9% to the average US Software industry of 12.0% in 3 years.

- If Inuvo's profit margin were to converge on the industry average, you could expect earnings to reach $4.9 million (and earnings per share of $0.32) by about June 2029, up from -$5.1 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 18.3x on those 2029 earnings, up from -4.1x today. This future PE is lower than the current PE for the US Software industry at 28.2x.

- Analysts expect the number of shares outstanding to grow by 0.81% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.12%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Despite robust top-line growth, Inuvo remains unprofitable with persistent operating and net losses; ongoing high operating costs, compressed gross margins from shifts in product mix, and limited liquidity reserves may continue to impact future earnings and restrict reinvestment, reducing long-term profitability.

- The company's growth is heavily reliant on a small number of large platform partners and a nascent, unproven self-serve client base, which exposes it to significant revenue volatility in the event of partner churn or slow adoption of new services, threatening revenue stability.

- Gross margin declined notably year-over-year (from 84% to 75.4%) due to increased cost of revenue and scaling of new campaigns with lower margin structures, indicating pressure on profitability even as revenues rise; continued downward pricing or unfavorable product mix could further compress net margins.

- Competition from tech giants with deeper resources (Google, Meta, Amazon) and industry consolidation pose long-term risks; barriers to scaling brand awareness and limited sales capacity restrict Inuvo's ability to capture market share, pressuring both revenue growth and margin expansion.

- The rapid evolution of the adtech industry, including further privacy regulation, browser changes (e.g., cookie deprecation), and shifts to new AI-driven or LLM-based search platforms, presents uncertainty; slow adaptation or loss of technical relevance could diminish the effectiveness of Inuvo's technology, directly impacting future revenues and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $4.55 for Inuvo based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $6.0, and the most bearish reporting a price target of just $2.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $40.5 million, earnings will come to $4.9 million, and it would be trading on a PE ratio of 18.3x, assuming you use a discount rate of 9.1%.

- Given the current share price of $1.41, the analyst price target of $4.55 is 69.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Inuvo?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.