Last Update 24 Mar 26

Fair value Decreased 0.28%BILI: AI Spending Will Support Engagement While Execution Risk And Pricing Persist

Analysts have slightly reduced Bilibili's fair value estimate while maintaining a relatively high future P/E assumption. This reflects a modestly lower blended price target after BofA's $1 cut and JPMorgan's upgrade to $35, based on increased AI investment and anticipated support for user engagement and advertising revenue.

Analyst Commentary

Recent Street research around Bilibili highlights a mixed tone, with optimism on AI investment sitting alongside more cautious valuation resets. JPMorgan has moved to a more constructive stance with a US$35 price target, citing AI driven user engagement and advertising opportunities, while other voices have trimmed fair value estimates.

In practical terms, price targets are clustering in a relatively tight range, with one large firm trimming its target by US$1 and JPMorgan lifting its target from US$27 to US$35. For investors, that combination signals enthusiasm for the long term potential of AI initiatives, but also serves as a reminder that execution risk and earnings visibility still matter to how the stock is being priced.

JPMorgan characterizes Bilibili as a "solid profit compounder" and points to AI as a key support for user metrics and ad revenue. At the same time, the reference to the shares being 26% below a recent peak underlines that the market has already reassessed expectations, which can cut both ways for anyone considering new exposure.

Bearish Takeaways

- Bearish analysts cutting price targets, including the US$1 reduction from one major firm, highlight concern that prior expectations for earnings power and AI monetization may have been too optimistic.

- The presence of multiple research updates in a short window, including target changes and rating shifts, points to uncertainty around execution on AI investment and how quickly it can translate into consistent growth in user and advertising revenue.

- The reference to shares being 26% below a recent peak suggests that some investors have already reacted to valuation and growth worries, which bearish analysts may view as a signal that confidence in the current P/E assumptions is fragile.

- Even with a US$35 price target from JPMorgan, the earlier, lower US$27 target and the separate US$1 cut elsewhere serve as a reminder that not all analysts are aligned on Bilibili's ability to deliver on its AI ambitions without further volatility in forecasts and valuation multiples.

What's in the News

- Bilibili has scheduled a board meeting for Mar 5, 2026 to consider and approve unaudited financial results for the fourth quarter and full year ended Dec 31, 2025 (company event filing).

- The same Mar 5, 2026 board meeting will also review unaudited financial results language that appears in a second disclosure, reinforcing the focus on Q4 and full year 2025 performance (company event filing).

Valuation Changes

- Fair Value: trimmed slightly from $23.12 to $23.05, a modest adjustment to the intrinsic value estimate.

- Discount Rate: nudged up from 9.39% to 9.41%, indicating a marginally higher required return in the model.

- Revenue Growth: CN¥ revenue growth assumption adjusted from 7.26% to 7.39%, reflecting a small change in top line expectations.

- Net Profit Margin: CN¥ net profit margin moved from 6.85% to 6.90%, a very minor refinement to profitability assumptions.

- Future P/E: future P/E multiple lowered from 34.16x to 33.73x, suggesting a slightly more conservative earnings multiple being used.

Key Takeaways

- Declining youth demographics and increased competition threaten user growth, engagement, and the ability to monetize core audiences.

- Regulatory pressures and high operational costs undermine sustained profitability, while shifting consumer preferences limit future revenue streams.

- Robust user engagement, AI-driven monetization, diversified revenue streams, and operational efficiencies position Bilibili for sustained profitability and resilience against market and regulatory challenges.

Catalysts

About Bilibili- Provides online entertainment services for the young generations in the People’s Republic of China.

- Bilibili's future user and revenue growth is likely to be constrained by China's shrinking youth demographic, resulting in a smaller core audience and diminishing long-term engagement, which will erode the company's ability to grow its top line and monetize at historical rates.

- Heightened regulatory scrutiny and evolving content controls threaten the sustainability of user-generated and subculture content, significantly increasing compliance costs and introducing unpredictability for both monetization and innovation, with a direct negative impact on net margins and earnings.

- Intense competition from global and domestic platforms-especially short-video apps and AI-driven interactive media-poses a continual threat to Bilibili's market share, risking stagnating user metrics and diluting ad revenue growth as consumer preferences shift.

- Despite recent improvements in gross and operating margins, Bilibili's high ongoing costs for content acquisition, server infrastructure, and user acquisition are unlikely to decline meaningfully, putting sustained profitability and operating leverage at risk as revenue growth decelerates.

- Market saturation and user fatigue in the online video and interactive media sector are expected to curb both engagement and time spent per user, putting incremental pressure on advertiser demand and reducing long-term revenue streams, ultimately constraining future earnings growth.

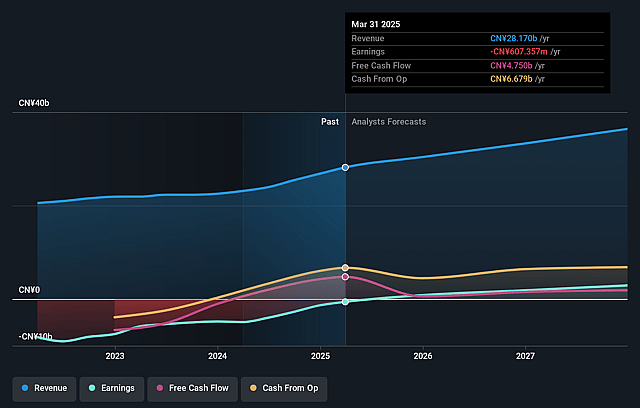

Bilibili Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Bilibili compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Bilibili's revenue will grow by 7.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 3.9% today to 6.9% in 3 years time.

- The bearish analysts expect earnings to reach CN¥2.6 billion (and earnings per share of CN¥7.18) by about March 2029, up from CN¥1.2 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as CN¥5.4 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 33.8x on those 2029 earnings, down from 58.0x today. This future PE is greater than the current PE for the US Interactive Media and Services industry at 14.7x.

- The bearish analysts expect the number of shares outstanding to grow by 0.22% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.41%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- User growth and engagement remain robust, with daily active users reaching 109 million (up 7% year-over-year) and monthly active users rising to 363 million (up 8%), alongside increased time spent on the platform, all of which underpin Bilibili's potential to sustain and expand its revenue base.

- Bilibili's successful deployment of AI for advertising optimization and content recommendations has led to revenue growth in advertising and higher gross margin, suggesting the company can benefit further from digital transformation trends and enhance overall profitability.

- The rise in proprietary and high-quality user-generated content, coupled with a sticky Gen Z+ community and strong retention rates (12-month retention around 80%), supports continued improvements in monetization, potentially driving higher average revenue per user and earnings growth.

- Diversification of business lines-including substantial advances in gaming, e-commerce, and high-margin value-added services-provides multiple pathways for revenue expansion and increases resilience against market or regulatory shifts, which can help support stable or rising net margins over time.

- Operational efficiency improvements, disciplined cost control, and a clear pathway to higher operating margins (with a midterm OP margin target of 15–20%) point to a sustained trajectory toward greater net profit and improved returns to shareholders, which could positively impact the company's share price in the long run.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Bilibili is $23.05, which represents up to two standard deviations below the consensus price target of $30.85. This valuation is based on what can be assumed as the expectations of Bilibili's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $41.35, and the most bearish reporting a price target of just $21.03.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be CN¥37.6 billion, earnings will come to CN¥2.6 billion, and it would be trading on a PE ratio of 33.8x, assuming you use a discount rate of 9.4%.

- Given the current share price of $24.26, the analyst price target of $23.05 is 5.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Bilibili?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.