Last Update 20 Mar 26

Fair value Decreased 0.031%WULF: Power Assets And 2.2 GW Portfolio Will Support Future AI Hosting

Analyst price targets for TeraWulf have shifted within a relatively tight range, with some firms trimming expectations by about $1 while others lifted targets by $3 to $7, as analysts incorporate higher spending, accounting changes around the Abernathy joint venture, and growing confidence in the company’s transition from Bitcoin mining to AI focused high performance computing.

Analyst Commentary

Bullish analysts are largely framing the recent pullback as a reset rather than a change in the core thesis, pointing to the AI focused high performance computing shift and the company’s power assets as key pillars of their views.

Across recent notes, target prices have clustered in the low to mid US$20s, with some research moving higher as analysts factor in the transition away from Bitcoin mining and the potential to monetize the 2.2 GW portfolio over time.

Several firms also acknowledge near term earnings noise from higher spending and equity method accounting for the Abernathy joint venture, but still emphasize execution on the new model as the key driver for their valuation work.

Bullish Takeaways

- Multiple bullish analysts have lifted price targets into the US$23 to US$27 range, tying their views to growing confidence in the company’s ability to scale AI focused high performance computing and eventually fully utilize its 2.2 GW power portfolio.

- One bullish group characterizes the recent 22% to 23% share pullback from the late February high as an appealing entry point, arguing that the market may be overly conservative on future lease signings and the value of existing leases.

- Positive commentary highlights the transition away from Bitcoin mining, with some analysts describing 2025 as transformational and suggesting that the shift to high performance computing is increasingly shaping the story for equity holders.

- Despite adjustments to EBITDA estimates to reflect higher spending and changes around the Abernathy joint venture, bullish analysts continue to anchor on execution in AI infrastructure as a central driver of their longer term valuation frameworks.

What's in the News

- U.S. crypto legislation known as the Clarity Act has stalled after banks declined to support a White House backed compromise on stablecoin rewards, keeping regulatory outcomes for cryptocurrency related firms, including TeraWulf, uncertain (Reuters).

- The White House is set to meet with banks and crypto firms to discuss the stalled crypto bill and potential paths forward on regulation, a process that includes companies operating in the broader digital asset space such as TeraWulf (Reuters).

- U.S. regulators have signaled plans to lay out crypto rules, which could influence how companies with digital asset exposure, including TeraWulf, operate and report activity in this sector (WSJ).

- TeraWulf has reported completion of a share repurchase program covering 24,468,750 shares, representing 6.38% of its shares, for a total of US$151.36m under the buyback announced on October 23, 2024. The company reported no additional shares repurchased from October 1, 2025 to December 31, 2025.

Valuation Changes

- Fair Value: $33.99 has moved slightly to $33.99, effectively unchanged within rounding.

- Discount Rate: The discount rate has eased slightly from 10.79% to 10.74%, indicating a modest adjustment in the required return assumption.

- Revenue Growth: Assumed revenue growth has risen slightly from 108.63% to 109.46%, with expectations for very high expansion remaining in place.

- Net Profit Margin: Assumed profit margin has fallen significantly from 22.62% to 11.36%, reflecting a more cautious view on future profitability levels.

- Future P/E: The future P/E multiple has increased significantly from 69.35x to 136.26x, indicating a higher valuation multiple applied to expected earnings.

Key Takeaways

- Transformative partnerships and long-term lease agreements uniquely position TeraWulf for rapid growth, strong recurring revenues, and enhanced pricing power in AI infrastructure.

- Zero-carbon infrastructure advantages and strategic acquisitions set the stage for sustained above-market growth, margin expansion, and long-term institutional adoption.

- Aggressive expansion into AI and green data centers heightens capital and operational risks amid customer concentration, volatile legacy mining, rising costs, and rapid technology shifts.

Catalysts

About TeraWulf- Operates as a digital asset technology company in the United States.

- Analyst consensus recognizes the strength of the AI hyperscale hosting agreements, but may understate just how transformative the $3.7 billion Fluidstack contract-with Google's $1.8 billion backstop and equity stake-will be in repositioning TeraWulf as a premier AI infrastructure provider, driving recurring, ultra-high-margin revenue and meaningfully reducing the company's cost of capital for future expansions.

- While consensus appreciates TeraWulf's new megawatt capacity and ongoing expansion, it may significantly underestimate how the Cayuga site's 80-year lease, together with contractor expertise and regional dominance, positions TeraWulf to accelerate its build-out pace and capture share as datacenter and crypto infrastructure demand soars, setting the stage for step-function revenue and EBITDA growth over the coming decade.

- The Google partnership serves not only as a major financial vote of confidence but also as a catalyst for attracting additional blue-chip tenants and strategic partnerships, potentially creating a virtuous cycle of demand, pricing power, and further margin expansion, all of which will enhance both top-line growth and bottom-line profitability.

- With the mainstreaming of AI, digital assets, and sustainability mandates, TeraWulf stands to benefit uniquely from surging institutional adoption of Bitcoin and the growing necessity for zero-carbon infrastructure-drivers which could sharply increase mining profitability, customer stickiness, and long-term fleet utilization.

- As consolidation accelerates in the mining and digital infrastructure sectors, TeraWulf's strengthened balance sheet, proven execution, and hard-to-replicate zero-carbon sites should enable accretive acquisitions and outsized market share gains, ultimately translating into above-market revenue growth and structurally higher operating margins.

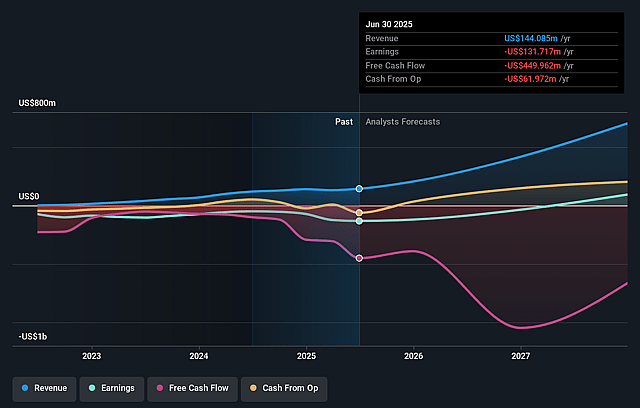

TeraWulf Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on TeraWulf compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming TeraWulf's revenue will grow by 109.5% annually over the next 3 years.

- The bullish analysts are not forecasting that TeraWulf will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate TeraWulf's profit margin will increase from -392.6% to the average US Software industry of 11.4% in 3 years.

- If TeraWulf's profit margin were to converge on the industry average, you could expect earnings to reach $175.8 million (and earnings per share of $0.34) by about March 2029, up from -$661.4 million today.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 136.4x on those 2029 earnings, up from -10.1x today. This future PE is greater than the current PE for the US Software industry at 29.0x.

- The bullish analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.74%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- TeraWulf's accelerated expansion into hyperscale AI hosting and HPC infrastructure will substantially increase capital expenditure and operational complexity, posing risks to future net margins and free cash flow, particularly if AI compute demand or contracted tenant revenues fail to materialize as forecast.

- Heavy reliance on major tenants such as Fluidstack, with Google's equity-linked backstop, introduces customer concentration risk and potential operational dependence, making overall revenue and earnings vulnerable to shifts in client strategy or performance failure tied to strict service-level agreements.

- While the company touts low-carbon power and green data centers as a structural advantage, tightening global decarbonization standards and competition for zero-carbon energy may drive up input costs and erode profitability, especially as more capital is committed to large-scale, long-duration energy contracts.

- TeraWulf's legacy bitcoin mining operations remain highly sensitive to bitcoin price volatility, hash rate escalation, and network difficulty, all of which could drive cyclical downturns in mining revenue and compress net margins, especially if resources are diverted to new ventures without commensurate returns.

- Rapid industry-wide innovation cycles in hardware for both bitcoin mining and advanced AI computing could force continuous, expensive upgrades and risk technological obsolescence, which may negatively impact long-term earnings and necessitate ongoing high capital investment just to maintain competitive relevance.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for TeraWulf is $33.99, which represents up to two standard deviations above the consensus price target of $25.33. This valuation is based on what can be assumed as the expectations of TeraWulf's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $37.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $1.5 billion, earnings will come to $175.8 million, and it would be trading on a PE ratio of 136.4x, assuming you use a discount rate of 10.7%.

- Given the current share price of $15.74, the analyst price target of $33.99 is 53.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on TeraWulf?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.