Last Update 02 May 26

Fair value Increased 10%WULF: Power Portfolio Monetization And HPC Transition Will Shape Future Returns

The analyst fair value estimate for TeraWulf has increased to $22.00 from $20.00, reflecting updated assumptions on growth, profitability, and discount rates as analysts respond to a series of recent price target increases across the Street.

Analyst Commentary

Recent research on TeraWulf has centered on how quickly the company can execute its shift away from Bitcoin mining and toward high performance computing, and how that shift should be reflected in valuation. Several firms have adjusted price targets in response to updated spending plans, joint venture accounting, and evolving expectations for power lease economics.

While many recent target moves have been positive, there are also more cautious voices pointing to execution and valuation risks as TeraWulf works through its transition and capital plans.

Bearish Takeaways

- Bearish analysts who trimmed their price target to $23 from $24 flagged higher spending and changes related to equity-method accounting for the Abernathy joint venture, which they see as a headwind to near term EBITDA and a reason to revisit assumptions in valuation models.

- Those same bearish analysts highlighted TeraWulf potentially exiting mining by year end, which introduces transition risk if the shift to HPC and power leasing does not scale as expected or if new contracts are slower to materialize.

- The share pullback from the February 25 52 week high is viewed by some bearish analysts as a sign that investors are reassessing risk around lease values and 2026 lease signings, suggesting the market could be applying a more conservative stance on long term growth.

- Concerns that investors might be over discounting current lease value or taking an overly cautious view of future lease agreements underscore the sensitivity of TeraWulf’s valuation to assumptions around power pricing, contract timing, and utilization of its 2.2 GW portfolio.

For you as an investor, these bearish points are a reminder to stress test your own assumptions on spending, joint venture economics, and the timing of the mining exit when comparing TeraWulf’s trading level with updated fair value estimates.

What's in the News

- TeraWulf completed a public offering of 54,510,000 common shares at US$19.00 per share. Underwriters fully exercised their option for an additional 7,110,000 shares. The company plans to use the proceeds for its Hawesville, Kentucky data center campus, repayment of a bridge credit facility, future site acquisitions, and general corporate purposes (Key Developments).

- The company filed and then completed follow-on equity offerings totaling about US$1.7b in common stock. This included a US$800m filed amount and a US$900.6m completed offering of 47,400,000 shares at US$19 with a US$0.475 discount per share (Key Developments).

- TeraWulf is looking for acquisitions alongside its capital raise plans, signaling interest in adding new sites or capabilities funded in part by recent equity proceeds (Key Developments).

- Directors, officers, and other holders agreed to lock-up arrangements on 435,381,960 common shares, certain warrants, and restricted stock units through a 31-day period from April 14, 2026 to May 15, 2026, limiting sales and transfers during that window (Key Developments).

- The company issued earnings guidance for first quarter 2026, indicating expected revenue in a range of US$30m to US$35m for the period ended March 31, 2026 (Key Developments).

Valuation Changes

- Fair Value was raised modestly to $22.00 from $20.00, reflecting adjusted assumptions in the model.

- The Discount Rate was reduced slightly from 10.83% to 9.81%, which increases the present value of projected cash flows in the updated analysis.

- Revenue Growth was adjusted slightly higher from 83.46% to 85.18%, indicating a small uplift in top line expectations.

- The Net Profit Margin moved marginally from 11.36% to 11.45%, signaling only a minor change in expected profitability on future revenue.

- The Future P/E inched up from 119.62x to 123.42x, suggesting a somewhat richer multiple embedded in the new fair value estimate.

Key Takeaways

- Heavy investment in capacity and reliance on a few key clients exposes TeraWulf to pronounced operational, regulatory, and technological disruptions.

- Rising financing needs and tightening regulation pose risks to profitability, while rapid tech shifts could undermine its fundamental business model.

- Expansion into AI hosting, secured partnerships with major tech firms, and focus on sustainable infrastructure position TeraWulf for diversified growth and improved financial stability.

Catalysts

About TeraWulf- Operates as a digital asset technology company in the United States.

- The company's aggressive capacity expansion and complex hyperscale build-out, including 400 megawatts at Cayuga and over 200 megawatts for Fluidstack, expose TeraWulf to significant long-term operational and capital risk. If demand for AI and HPC infrastructure falters due to regulatory changes or shifts in technology, excess capacity could go underutilized, leading to lower than projected revenue and potential impairment charges.

- TeraWulf remains heavily reliant on a concentrated tenant base for its new digital infrastructure offerings, with deals that are complex and bespoke. Should key customers like Fluidstack or Google materially change their strategic priorities or face business headwinds, TeraWulf could suffer abrupt contract terminations or non-renewals, which would create a sharp decline in future revenue and erode the anticipated increase in net operating margins.

- The company's surging capital expenditures, with large portions back-ended and an ongoing need to raise external financing even after the Google backstop, increase balance sheet leverage and interest expense risk. If macroeconomic or industry-wide credit conditions tighten, TeraWulf may be forced to accept unfavorable debt terms or dilutive equity raises, significantly compressing future net margins and limiting shareholder returns.

- Global regulatory scrutiny targeting the energy consumption and environmental impact of large-scale digital infrastructure, particularly in cryptocurrency and AI data center operations, is mounting. If new rules impose higher compliance costs or restrict TeraWulf's operations, long-run earnings power could be impaired as electricity, permitting, and sustainability requirements become more onerous.

- Rapid advances in computing and blockchain consensus mechanisms, including a potential shift away from energy-intensive proof-of-work to alternative models like proof-of-stake, threaten the very relevance of TeraWulf's core business model. Should these technologies gain widespread adoption, the demand for TeraWulf's services may collapse, rendering much of its fixed-cost, capital-intensive infrastructure obsolete and severely impacting future cash flows and overall valuation.

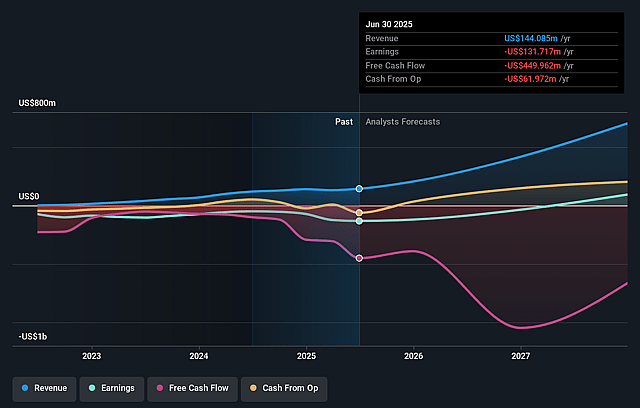

TeraWulf Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on TeraWulf compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming TeraWulf's revenue will grow by 85.2% annually over the next 3 years.

- The bearish analysts are not forecasting that TeraWulf will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate TeraWulf's profit margin will increase from -392.6% to the average US Software industry of 11.5% in 3 years.

- If TeraWulf's profit margin were to converge on the industry average, you could expect earnings to reach $122.5 million (and earnings per share of $0.24) by about May 2029, up from -$661.4 million today.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 123.5x on those 2029 earnings, up from -15.8x today. This future PE is greater than the current PE for the US Software industry at 30.3x.

- The bearish analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.81%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The execution of a 10-year, $3.7 billion+ hyperscale AI hosting agreement with Fluidstack, backstopped by Google, will diversify TeraWulf's revenue mix beyond bitcoin mining, potentially driving significant top-line growth and improving earnings stability even if BTC prices decline.

- Google's $1.8 billion credit backstop and equity participation significantly enhances TeraWulf's credit profile, enabling access to lower-cost capital, supporting scalable growth initiatives, and likely improving net margins by reducing financing costs.

- TeraWulf's ability to secure long-term, zero-carbon power sources at both Lake Mariner and the newly leased 400MW Cayuga site positions the company to benefit from the rising global demand for sustainable digital infrastructure, supporting competitive advantage and margin resilience.

- Growing enterprise and hyperscaler demand for AI infrastructure, validated by the urgency and scale of recent customer agreements, aligns TeraWulf with robust secular tailwinds in digitalization, which could drive strong, recurring revenue and support valuation multiples.

- The company's ongoing operational momentum, experienced team, and successful delivery on large projects for marquee clients like Core42, Fluidstack, and Google suggest continued execution strength, which may enhance TeraWulf's financial performance and drive improved net income in future years.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for TeraWulf is $22.0, which represents up to two standard deviations below the consensus price target of $27.6. This valuation is based on what can be assumed as the expectations of TeraWulf's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $41.5, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $1.1 billion, earnings will come to $122.5 million, and it would be trading on a PE ratio of 123.5x, assuming you use a discount rate of 9.8%.

- Given the current share price of $21.31, the analyst price target of $22.0 is 3.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on TeraWulf?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.