Last Update 09 Jul 26

Fair value Decreased 13%KMR: Lower Production And Higher Discount Rate Will Support Future Cash Flows

The analyst price target for Kenmare Resources has been revised in light of updated assumptions on fair value, discount rate, revenue growth, profit margin and future P/E. The new target is now set at £3.93 compared with the prior £4.50, as analysts factor in a different balance of growth and risk in their models.

What’s in the News for Kenmare Resources

- Kenmare Resources reported first quarter 2026 operating results, with excavated ore of 8,005,000 tonnes compared with 9,338,000 tonnes a year earlier. Source: Company operating results announcement.

- Heavy mineral concentrate production for the quarter was 217,200 tonnes, with 205,300 tonnes processed, compared with 312,300 tonnes produced and 303,900 tonnes processed in the prior year period. Source: Company operating results announcement.

- Ilmenite production for the first quarter was 125,900 tonnes, compared with 204,500 tonnes a year earlier. Source: Company operating results announcement.

- Primary zircon production was 8,900 tonnes and rutile production was 1,000 tonnes for the quarter, compared with 14,000 tonnes and 2,500 tonnes respectively in the same quarter a year ago. Source: Company operating results announcement.

- Concentrates output was 45,200 tonnes for the quarter, compared with 9,100 tonnes in the prior year period. Source: Company operating results announcement.

Valuation Changes for Kenmare Resources

- Fair value was revised down from £4.50 to £3.93, a reduction of about 13% in the modelled estimate.

- The discount rate increased slightly from 11.40% to roughly 11.95%, reflecting a higher required return in the valuation work.

- Revenue growth was lifted modestly from about 8.35% to roughly 9.44%, indicating a higher assumed dollar revenue growth rate in the forecast period.

- The net profit margin was adjusted from around 11.72% to roughly 11.19%, a small reduction in the projected profitability level.

- The future P/E multiple moved from 15.26x to about 13.66x, implying a lower valuation multiple applied to Kenmare Resources in the updated analysis.

Key Takeaways

- Expanded mining capacity and flexible operations are set to boost production, reduce costs, and support higher revenues and resilient margins.

- Elevated demand and critical mineral status position Kenmare to gain market share and pricing power, strengthening long-term growth and shareholder returns.

- Rising costs, market oversupply, political risks, high debt, and revenue concentration expose Kenmare to margin pressure, cash flow volatility, and uncertainty in shareholder returns.

Catalysts

About Kenmare Resources- Engages in the production and sale of mineral sand products in China, rest of Asia, Europe, the United States, and internationally.

- The upcoming completion and commissioning of expanded mining capacity at Nataka, supported by new high-capacity dredges and processing equipment, is expected to significantly grow Kenmare's production volumes and lower unit costs, which should drive higher revenues and improved net margins from 2025 onward.

- Execution of the selective mining operation (SMO) projects-low-capex, flexible mining solutions-adds incremental capacity and operational flexibility, enabling Kenmare to respond to demand spikes or market opportunities more efficiently, supporting both revenue and margin resilience.

- Growing global demand for titanium feedstocks and zircon, driven by ongoing urbanization, infrastructure buildout in emerging markets, and increased use of these minerals in renewable energy technologies, underpins robust long-term sales volume and pricing potential.

- Accelerating resource security concerns and the critical minerals designation for Kenmare's products in the EU, UK, and US are likely to increase customer preference for reliable suppliers outside China, potentially allowing Kenmare to capture market share and command price premiums, benefiting top-line growth.

- As the company transitions past its peak capex and the majority of operational/development project risk is behind it, Kenmare's strong balance sheet and established dividend/buyback policy position it for higher future distributions and enhanced total shareholder return when free cash flow rises.

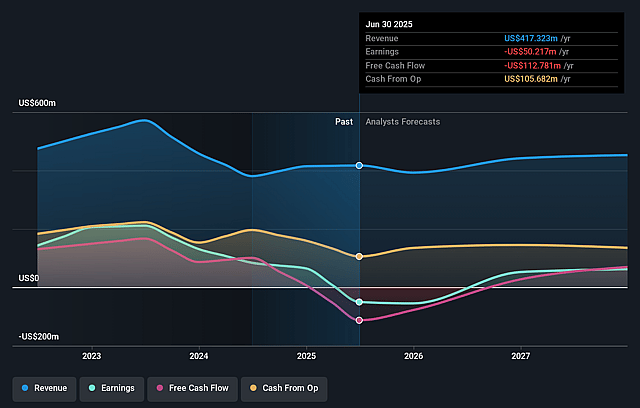

Kenmare Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Kenmare Resources's revenue will grow by 9.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from -98.9% today to 11.2% in 3 years time.

- Analysts expect earnings to reach $48.2 million (and earnings per share of $0.53) by about July 2029, up from -$325.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.7x on those 2029 earnings, up from -0.7x today. This future PE is lower than the current PE for the GB Metals and Mining industry at 15.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.95%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The protracted and uncertain negotiations over the renewal of the implementation agreement with the Mozambican government, particularly regarding a rising royalty rate (potentially up to nearly 5% of revenue), could significantly increase the company's future cost base and reduce net margins if terms become less favorable.

- Elevated supply of ilmenite and concentrates from artisanal and low-cost producers in Africa, especially in Mozambique, is contributing to structural oversupply in global markets; this ongoing dynamic is delaying price recovery and has already resulted in a $100 million impairment at Kenmare, posing a risk to future revenue growth and profitability.

- Operations in Mozambique face heightened political risk, security concerns, and have recently experienced disruptions (e.g., due to social unrest around elections), contributing to rising operating and compliance costs and potential for volatility or interruptions in cash flows.

- The company's large, capital-intensive projects-while almost complete-have caused a spike in net debt (from $25m to $85m) and increased dependency on future earnings improvements and successful ramp-up; if product pricing remains soft for an extended period or the ramp-up faces delays, servicing debt and maintaining dividends may become more challenging, impacting free cash flow and total shareholder return.

- Kenmare's reliance on a concentrated customer base, with strong but potentially limited long-term contracts, creates revenue concentration risk should a key customer reduce orders or renegotiate, especially in a soft market environment, which could directly impact top-line revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £3.93 for Kenmare Resources based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £5.65, and the most bearish reporting a price target of just £2.21.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $430.6 million, earnings will come to $48.2 million, and it would be trading on a PE ratio of 13.7x, assuming you use a discount rate of 12.0%.

- Given the current share price of £2.0, the analyst price target of £3.93 is 49.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Kenmare Resources?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.