Last Update 09 Jun 26

KNOP: Recent Upgrades And Higher Future P/E Will Support Bullish Case

Analysts have raised their price target on KNOT Offshore Partners to $14.50, citing recent upgrades from Fearnley and B. Riley along with updated assumptions regarding the discount rate, revenue trends, profit margins, and future P/E multiples.

Analyst Commentary

Bullish Takeaways

- Bullish analysts highlight that the updated discount rate assumptions support a higher intrinsic value, which they see as aligning with the new US$14.50 price target.

- They point to revised revenue expectations as better matching the partnership's current contract profile, which they believe improves confidence in projected cash flows and earnings.

- Optimistic views also focus on profit margin assumptions that analysts consider more realistic, which they see as supporting the case for a higher justified P/E multiple.

- Bullish analysts argue that the combination of revised cash flow estimates and valuation multiples suggests the stock may be pricing in more conservative execution risks than their updated models.

Bearish Takeaways

- Bearish analysts caution that the revised valuation still relies on assumptions about stable revenue trends, which could be at risk if contract renewals or utilization levels differ from current expectations.

- They stress that profit margin forecasts leave limited room for operational missteps, so any cost overruns or downtime could pressure earnings relative to the implied P/E multiple.

- Some are wary that lower discount rate assumptions can make the valuation sensitive to changes in risk sentiment or funding conditions, which may not be fully reflected in the current price target.

- Bearish analysts also flag that the higher target price leaves less cushion if execution falls short of the modeled revenue and margin path, which could lead to future estimate revisions.

What's in the News

- KNOT Offshore Partners' Board of Directors declared a quarterly cash distribution of US$0.05 per common unit for the first quarter ended March 31, 2026, payable on May 14, 2026, to unitholders of record as of April 27, 2026. The Board indicated this change is part of an ongoing review of capital allocation. (Source: Key Developments)

- Knutsen NYK Offshore Tankers AS cancelled its unsolicited non binding proposal to acquire an additional 70.80% stake in KNOT Offshore Partners for approximately US$240 million, or US$10 per unit, after both sides concluded they could not reach an agreement, ending discussions around a potential take private transaction. (Source: Key Developments)

- The terminated offer would have required approvals from the Conflicts Committee, the KNOT Offshore Partners Board, the KNOT board of directors and a majority of common, Class B and preferred unitholders. The parties had engaged advisors including DNB Carnegie, Baker Botts L.L.P., Evercore Group L.L.C. and Richards, Layton & Finger, P.A. before discussions were ended on March 19, 2026. (Source: Key Developments)

Valuation Changes

- Fair Value: Kept steady at $14.50 per unit, with no change between the previous and updated assessment.

- Discount Rate: Trimmed slightly from 10.32% to 10.20%, indicating a small adjustment to the required return used in the valuation model.

- Revenue Growth: Assumed decline has moderated, moving from revenue falling 2.39% to a smaller 0.31% decline in the updated assumptions.

- Net Profit Margin: Reduced from 9.89% to 7.65%, reflecting a lower expected share of revenue converting into earnings.

- Future P/E: Raised from 19.20x to 22.87x, implying a higher valuation multiple applied to expected earnings in the updated model.

Key Takeaways

- Robust demand for offshore oil transport and limited alternative infrastructure ensure stable revenue and high vessel utilization for KNOT's modern shuttle tanker fleet.

- Long-term, fixed-rate contracts and a tightening shuttle tanker market support strong earnings visibility, margin improvement, and sustained distribution potential.

- Rising refinancing costs, leverage, and customer concentration heighten earnings volatility and limit flexibility, while industry decarbonization trends threaten long-term demand and cash flow growth.

Catalysts

About KNOT Offshore Partners- Acquires, owns, and operates shuttle tankers under long-term charters in the North Sea and Brazil.

- Anticipated growth in deepwater offshore oil production, particularly in Brazil (with numerous new FPSOs coming online), is expected to drive sustained demand for shuttle tanker services, supporting higher vessel utilization rates and increasing future contracted revenues for KNOT.

- Persistent infrastructure constraints and lack of scalable alternatives to marine transportation for moving offshore oil, especially in production-heavy regions, suggest long-term, reliable demand for KNOT's specialized shuttle tanker fleet, which underpins revenue stability and supports contract renewals at potentially higher day-rates.

- KNOT's strong pipeline of long-term, fixed-rate charter contracts-with $854 million in backlog and growing charter coverage-provides earnings visibility, reduces revenue volatility, and enhances the capacity to sustain and potentially increase distributions over time.

- Ongoing fleet modernization via drop-downs and accretive asset acquisitions from Knutsen NYK (the sponsor) allows KNOT to maintain a younger, more efficient fleet, potentially leading to higher net margins and improved operational efficiency as older vessels are swapped for newer ones on favorable terms.

- The slow pace of new shuttle tanker deliveries, combined with rising regulatory standards on emissions, points to a tightening market supply, which is likely to support elevated charter rates and fleet values-positively impacting KNOT's topline growth and net profitability over the long term.

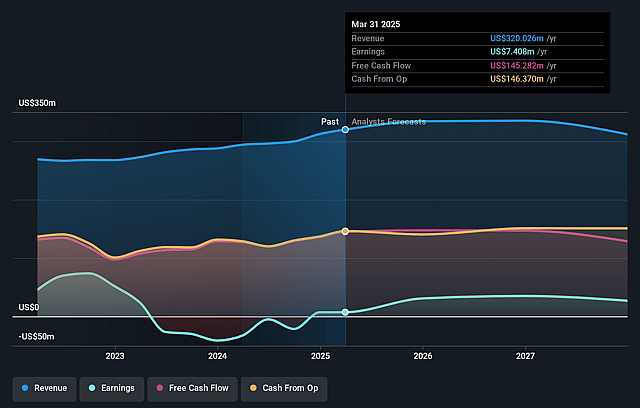

KNOT Offshore Partners Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming KNOT Offshore Partners's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from 3.1% today to 7.6% in 3 years time.

- Analysts expect earnings to reach $28.0 million (and earnings per share of $0.81) by about June 2029, up from $11.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $65.0 million in earnings, and the most bearish expecting $-10.0 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 23.2x on those 2029 earnings, down from 32.3x today. This future PE is greater than the current PE for the US Oil and Gas industry at 13.8x.

- Analysts expect the number of shares outstanding to decline by 1.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.2%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's significant upcoming debt maturities and balloon payments in 2025 and 2026 pose refinancing risk, particularly as existing low-rate interest rate hedges are rolling off and new swaps will likely be at higher market rates, potentially raising interest expense and eroding net margins and earnings.

- Persistent focus on fleet expansion via drop-downs rather than share buybacks may result in lower return on invested capital, especially if new vessel acquisitions generate a lower internal rate of return than the company's current equity valuation would justify, which could dilute earnings per share and limit capital returns to shareholders.

- Customer concentration risk remains elevated, as several vessels have long-term charters with a small pool of oil majors; if contracts are not renewed or options are not exercised, revenue backlog and fixed charter coverage would decrease, increasing earnings volatility and revenue risk.

- The current strategy increases leverage and future amortization commitments, which, alongside subdued distribution payouts, limits financial flexibility for reinvestment or weathering industry downturns, raising the risk of dividend cuts or missed growth opportunities if market conditions weaken.

- Long-term industry and secular shifts toward decarbonization, stricter emissions regulations, and global energy transition could gradually reduce demand for offshore oil transport and shuttle tankers, threatening vessel utilization, reducing day rates, and pressuring long-term revenue and cash flow growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $14.5 for KNOT Offshore Partners based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $366.2 million, earnings will come to $28.0 million, and it would be trading on a PE ratio of 23.2x, assuming you use a discount rate of 10.2%.

- Given the current share price of $10.75, the analyst price target of $14.5 is 25.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on KNOT Offshore Partners?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.