Last Update 15 Apr 26

Fair value Decreased 50%UPST: Bank Charter Effort Will Likely Fail To Offset Mounting Funding Risks

Analysts have reset the fair value estimate for Upstart Holdings to $20.00 from $40.17, reflecting lower price targets across several firms while still noting possible earnings upside and reduced funding risk tied to the company's bank charter efforts and new product launches.

Analyst Commentary

Recent Street research around Upstart reflects a split view, with some firms flagging upside tied to the bank charter effort and new products, while others are trimming price targets and staying cautious on execution and funding.

On the more constructive side, one major firm upgraded Upstart to Buy and highlighted the bank charter application as a direct response to concerns about reliance on private credit and external funding sources. The firm argued that the current share price does not appear to reflect potential upside from becoming a bank or the reduced liquidity risk if funding sources diversify.

Other analysts have moved ratings to Neutral from more bearish stances, sometimes alongside higher price targets. This suggests that valuation may now better reflect identified risks. These more balanced views point to potential upside if the company achieves its long term outlook, while stopping short of a clear bullish call.

At the same time, multiple firms have reset their price targets lower on Upstart, sometimes as part of broader cuts across consumer finance stocks. These moves often reference a more uncertain macro backdrop and compressed market multiples, which feed directly into more conservative assumptions on growth, profitability, and what investors might be willing to pay for that profile.

Separately, Upstart's launch of its "Cash Line" earned wage access product has drawn mixed reactions. While analysts see it as competitive with offerings from names such as Dave, Chime, and Brigit, at least one firm is keeping a Neutral rating after the launch. This signals that execution on new products still needs to be proven out in terms of customer adoption, unit economics, and risk management.

Bearish Takeaways

- Bearish analysts have cut price targets on Upstart, with some firms citing a more uncertain macro outlook and lower market multiples. This points to concern about how the stock is valued relative to peers and to its own risk profile.

- Recent target reductions suggest worries that execution on growth plans may not fully match earlier expectations, especially as the company pursues a bank charter and expands into new products that carry their own underwriting and regulatory risks.

- Neutral ratings maintained after new product launches indicate that, for some bearish analysts, potential growth optionality is not yet enough to offset concerns around funding stability, credit performance, and the durability of demand for Upstart powered loans.

- Ongoing target cuts from firms including JPMorgan highlight that a portion of the Street remains cautious on the balance between upside scenarios and downside risks tied to earnings volatility, capital needs, and the pace at which Upstart can scale profitably.

What's in the News

- Stone Ridge Asset Management fund holding Affirm and Upstart loans is seeing high redemptions, according to a report that highlights investor outflows tied to funds exposed to these lending platforms (Wall Street Journal).

- Pomerantz LLP announced a class action lawsuit filed in the Southern District of New York alleging misstatements related to Upstart's Model 22 AI underwriting, revenue guidance for 2025, and the model's response to macroeconomic signals, covering investors who bought shares between May 14, 2025 and November 4, 2025.

- Upstart plans to apply to the OCC, FDIC, and Federal Reserve to form Upstart Bank, N.A. and become a bank holding company. The company aims to place its lending activities under a single federal prudential framework and gain access to deposit funding alongside continued use of bank, credit union, and institutional capital sources.

- Upstart announced the Cash Line revolving credit product, offering approved consumers an ongoing line with a stated minimum of $200 and potential access up to $5,000. The product provides instant access without extra expedited fees and includes a $10 monthly membership for smaller lines, plus a stated APR range of 5% to 36% for higher balances.

- Upstart detailed leadership changes, with co founder and CTO Paul Gu set to become CEO on May 1, 2026. Co founder Dave Girouard will move to Executive Chairman and special advisor, and Andrea Blankmeyer will join as CFO while current CFO Sanjay Datta becomes President and Chief Capital Officer.

Valuation Changes

- Fair Value: reset from $40.17 to $20.00, a reduction of roughly 50% in the fair value estimate.

- Discount Rate: moved from 8.32% to 9.21%, indicating a higher required return on equity risk.

- Revenue Growth: adjusted from 23.45% to 26.21%, reflecting a slightly higher assumed top line growth rate.

- Net Profit Margin: revised from 15.20% to 16.31%, pointing to a modestly higher expected profitability level.

- Future P/E: shifted from 22.59x to 7.90x, representing a sharp compression in the multiple applied to projected earnings.

Key Takeaways

- Increasing data privacy regulations and AI oversight threaten Upstart's model accuracy, differentiation, and may drive up compliance costs and operational risks.

- Intensifying competition and reliance on limited partners expose Upstart to margin pressure, market share loss, and greater revenue volatility.

- AI-driven model enhancements, diversified lending products, stronger partner funding, and digital-first automation are boosting revenue growth, improving efficiency, and reducing financial risk.

Catalysts

About Upstart Holdings- Operates a cloud-based artificial intelligence (AI) lending platform in the United States.

- Dependence on ongoing access to alternative borrower data for AI model accuracy exposes Upstart to the risk that increasing consumer privacy awareness and tightening data privacy regulations will restrict access to these data sources, reducing model efficacy and potentially lowering approval rates and future transaction volumes, negatively impacting long-term revenue growth.

- Intensifying regulatory scrutiny of artificial intelligence and machine learning in credit decisioning could result in materially higher compliance expenses, model retraining requirements, and the erosion of Upstart's proprietary differentiation, compressing net margins and increasing operational risk over the next several years.

- Competitive threats from both legacy financial institutions and aggressive newer entrants, including large technology firms integrating similar AI-driven lending solutions, are likely to escalate, causing pricing pressure and potential loss of market share, resulting in declining take rates and eventual margin contraction.

- The prolonged elevated interest rate environment, coupled with the risk of further rates volatility, may lead to higher consumer credit losses and increased funding costs for Upstart's loan buyers, which could drive lenders away from the platform, decrease origination volumes, and depress both revenue and earnings growth.

- Ongoing reliance on a limited set of banking partners amplifies customer concentration risk, leaving Upstart vulnerable to abrupt funding withdrawals or the loss of key distribution relationships, resulting in unpredictable revenue volatility and diminished future earnings stability.

Upstart Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Upstart Holdings compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Upstart Holdings's revenue will grow by 26.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 5.0% today to 16.3% in 3 years time.

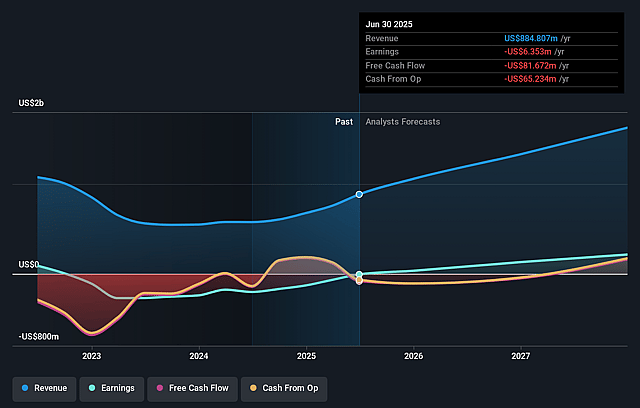

- The bearish analysts expect earnings to reach $352.6 million (and earnings per share of $2.58) by about April 2029, up from $53.6 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $549.1 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 7.9x on those 2029 earnings, down from 52.3x today. This future PE is lower than the current PE for the US Consumer Finance industry at 9.0x.

- The bearish analysts expect the number of shares outstanding to grow by 3.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.21%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Rapid improvements in AI model performance, exemplified by the launch of Model 22 and advances in automation and servicing, are directly increasing approval and conversion rates, as well as driving down loan losses, which may sustain stronger revenue growth and support net margins over the long term.

- Expansion into new lending verticals such as Home, Auto, and small dollar loans is accelerating, diversifying revenue streams, and growing Upstart's total addressable market, which could lead to higher aggregate revenues and improved long-run operating leverage.

- Strengthening funding partnerships, including significant bank and credit union relationships, as well as increasing access to third-party funding and the ABS market, may enhance Upstart's ability to scale loan originations without undue balance sheet risk, supporting more predictable earnings.

- Improvements in customer acquisition efficiency, increasing cross-sell opportunities, and a rising percentage of repeat borrowers are progressively lowering customer acquisition costs and may improve long-term contribution margins and profitability.

- The persistent trend toward digital and mobile-first borrowing, combined with Upstart's advancements in automation and instant loan processing across new product lines, positions the company to capture market share from slower-moving incumbents, potentially resulting in sustained revenue growth and enhanced margins over several years.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Upstart Holdings is $20.0, which represents up to two standard deviations below the consensus price target of $43.67. This valuation is based on what can be assumed as the expectations of Upstart Holdings's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $80.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $2.2 billion, earnings will come to $352.6 million, and it would be trading on a PE ratio of 7.9x, assuming you use a discount rate of 9.2%.

- Given the current share price of $29.53, the analyst price target of $20.0 is 47.7% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Upstart Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.