Last Update 23 Jun 26

Fair value Decreased 11%EH: Commercialization Progress And Buyback Will Support Long-Term Low Altitude Upside

EHang Holdings' updated analyst price target has moved lower, reflecting a reduced fair value from about $19 to about $17 as analysts factor in recent price target cuts to $13 and $11.10, softer near term profit margin assumptions, and delays around eVTOL commercialization and revenue recognition.

Analyst Commentary

Recent research on EHang Holdings shows a mix of optimism about long term commercialization potential and caution around execution risks, reflected in lower price targets and rating changes.

Bullish Takeaways

- Bullish analysts maintain a positive stance on EHang Holdings even after trimming price targets, indicating they still see upside potential relative to current trading levels.

- Management attribution of weaker Q1 deliveries to seasonal factors and slower local government procurement points to issues that analysts view as timing related rather than purely demand related.

- Current profit pressure from higher operating expenses is seen by bullish analysts as tied to building out eVTOL capabilities and delivery capacity, which they view as important for long term growth.

- Lowered but still supportive price targets suggest that, in bullish models, delays affect timing of cash flows and revenue recognition more than the existence of the underlying commercialization opportunity.

Bearish Takeaways

- Bearish analysts have shifted to more cautious ratings and reduced price targets, reflecting increased concern about the pace of eVTOL commercialization and associated revenue growth for EHang Holdings.

- Delayed government approval for eVTOL commercialization in Hefei and Guangzhou, with no clear timeline, introduces uncertainty around when larger scale deployments and related revenues can be recognized.

- Downward revisions to 2025 revenue assumptions and reduced shipment and revenue forecasts for 2026 to 2028 highlight execution risk around both deliveries and accounting treatment under U.S. GAAP.

- Pushed out breakeven expectations to the 2029 to 2030 period, compared with earlier expectations of the 2026 to 2027 period, signals that some analysts now anticipate a longer period of investment and operating losses before EHang Holdings reaches sustained profitability.

What’s in the News for EHang Holdings

- EHang Holdings reported Q1 2026 revenue of US$3.7 million versus analyst expectations of US$53.9 million, with eVTOL aircraft sales falling more than 90% and only four EH216 units sold, while losses narrowed mainly due to cost management. (Source: Q1 2026 earnings coverage)

- The company highlighted ongoing progress toward commercializing what it describes as the world’s first pilotless human carrying eVTOL, with regulatory approvals advancing, routine trial operations underway, and an expanding international footprint that includes new operating licenses in Thailand. (Source: Q1 2026 earnings coverage)

- EHang reported that non human carrying businesses accounted for about 40% of Q1 2026 revenue, including 22 aerial media shows and operations using 1,000 GD 4.0 formation drones, indicating a broader mix of revenue sources alongside eVTOL aircraft sales. (Source: Q1 2026 earnings coverage)

- Management issued full year 2026 revenue guidance that indicates a significant acceleration later in the year, tied to increased commercialization efforts and higher R&D spending on autonomous aircraft technology, and separately reaffirmed full year 2026 revenue guidance of RMB 600 million. (Sources: Q1 2026 earnings coverage, Corporate Guidance)

- EHang’s board authorized a new share repurchase program of up to US$30 million in American Depositary Shares or ordinary shares, funded from existing cash and valid for 12 months, after which the stock rose more than 9% in premarket trading on the announcement. (Sources: Buyback announcements, Share buyback news)

Valuation Changes for EHang Holdings

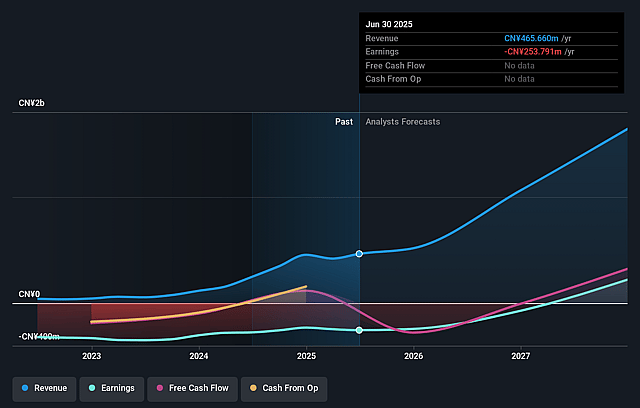

- Fair Value was reduced from about $18.00 to about $16.90, reflecting a lower implied valuation level for EHang Holdings.

- The Discount Rate increased slightly from about 8.36% to about 8.99%, indicating a higher required return assumption in updated models.

- Revenue Growth was raised from about 45.77% to about 56.61%, pointing to a higher projected CN¥ revenue growth rate despite near term commercialization delays.

- The Net Profit Margin was lowered from about 33.97% to about 28.55%, suggesting expectations for slimmer CN¥ earnings relative to revenue in future periods.

- The Future P/E moved up from about 25.6x to about 27.5x, indicating a higher earnings multiple applied in the updated valuation framework.

Key Takeaways

- Expansion into urban air mobility and strong government partnerships enhance regulatory acceptance, infrastructure integration, and long-term revenue growth potential.

- Innovations in battery technology and a dual business model foster market differentiation, recurring revenue, and margin improvement through operational services and proven safety records.

- Heavy reliance on China, rising costs, and certification delays pose risks to growth and profitability as EHang prioritizes operational stability over aggressive expansion.

Catalysts

About EHang Holdings- Operates as an urban air mobility (UAM) technology platform company in the People’s Republic of China, East Asia, West Asia, North America, South America, West Africa, and Europe.

- The ongoing expansion of urban air mobility use cases-especially driven by government initiatives in smart cities, emergency response, and low-altitude economic ecosystems-positions EHang's autonomous aerial vehicles as foundational infrastructure, which is likely to sustain robust long-term demand and revenue growth as cities increasingly adopt eVTOL solutions.

- The company's deepening partnerships with municipal governments (such as Hefei's RMB 500 million support for the VT35 hub) and involvement in setting regulatory and safety standards enhances regulatory acceptance and ecosystem integration, supporting wider market entry, improved top-line growth, and improved long-term earnings visibility.

- Significant advancements in battery R&D-including solid-state battery integration and partnerships aimed at improving flight range, safety, and eco-friendliness-strengthen EHang's differentiation in green air mobility; this aligns with growing regulatory and societal demands for carbon reduction, which should drive both sales volumes and the ability to command higher margins due to performance leadership.

- Transitioning to a dual business model that combines eVTOL manufacturing with high-value operational services (maintenance, software, training, and operations management) is expected to unlock recurring revenue streams and meaningfully improve overall net margins and earnings resilience as the installed base scales.

- EHang's first-mover advantage in passenger-carrying pilotless eVTOL commercialization, validated by a proven safety record and accelerating order conversion, underpins sustained pricing power, competitive differentiation, and high customer switching costs, which should contribute to long-term margin expansion and earnings growth as volumes ramp.

EHang Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming EHang Holdings's revenue will grow by 56.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from -77.6% today to 28.6% in 3 years time.

- Analysts expect earnings to reach CN¥457.9 million (and earnings per share of CN¥4.41) by about June 2029, up from -CN¥323.9 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CN¥812.2 million in earnings, and the most bearish expecting CN¥282.7 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 27.8x on those 2029 earnings, up from -11.1x today. This future PE is lower than the current PE for the US Aerospace & Defense industry at 40.2x.

- Analysts expect the number of shares outstanding to grow by 4.32% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.99%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- EHang's lowered revenue guidance for 2025 and its strategy to moderate the pace of order deliveries in favor of focusing on operational readiness and safety signal that the company is prioritizing long-term stability over short-term sales growth; this transition may lead to slower revenue growth and increases the risk that scaling will be delayed, impacting near-future top-line revenues.

- International expansion remains in early stages, with 90% of current sales and backlog concentrated in China; limited overseas certification and very modest overseas deliveries so far raise concerns about the company's ability to diversify revenue and increase its addressable market, making future earnings vulnerable to domestic regulatory or economic headwinds.

- EHang's continued high operating expenses-largely due to accelerated R&D investment and workforce expansion-are outpacing gross profit growth, which could put persistent pressure on net margins and profitability, particularly if operational ramp-up or commercial adoption is slower than anticipated.

- Heightened competition from larger, global aerospace and eVTOL players with more resources could erode EHang's technological lead, dampen pricing power, and compress both revenues and margins if multinational rivals gain certifications or market traction faster, both domestically and internationally.

- Delays or stricter standards in achieving large-scale regulatory certifications for new aircraft models, batteries, and international operations could impede commercial deployments, slow revenue recognition, and limit market expansion-exposing EHang's long-term growth to regulatory and operational execution risks.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $16.9 for EHang Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.25, and the most bearish reporting a price target of just $9.72.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CN¥1.6 billion, earnings will come to CN¥457.9 million, and it would be trading on a PE ratio of 27.8x, assuming you use a discount rate of 9.0%.

- Given the current share price of $7.03, the analyst price target of $16.9 is 58.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on EHang Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.