Last Update 01 Jul 26

Fair value Increased 5.72%UBSG: Future Returns Will Rely On Capital Actions And Ethereum Compliance Progress

The analyst price target for UBS Group has been revised higher to CHF 45 from CHF 40, reflecting updated expectations around a fair value of CHF 40.57, a slightly adjusted discount rate of 9.02%, modestly lower revenue growth assumptions of 2.43%, a small increase in projected profit margin to 25.66%, and a higher future P/E of 13.40% as analysts factor in recent sector research and sentiment shifts.

Analyst Commentary

Recent research on UBS Group shows a mix of optimism and caution, with several banks revising price targets and ratings as they reassess valuation, execution risks, and growth expectations around the current set of forecasts.

Bullish Takeaways

- Bullish analysts have lifted UBS Group price targets toward the CHF 40 to CHF 45 range, which broadly aligns with the updated fair value estimate and supports the idea that the current valuation framework is still seen as reasonable.

- Repeated upward adjustments to price targets over recent months suggest that bullish analysts view the company as executing well enough on its current plan to justify higher target multiples on earnings.

- Some bullish analysts are comfortable maintaining positive recommendations even as price targets move higher. This indicates they see room for the UBS Group stock to reflect the updated P/E and margin assumptions in their models.

- Target changes clustered in similar ranges hint that bullish analysts broadly agree on the earnings power and balance of risks embedded in UBS Group forecasts, rather than viewing the current setup as stretched.

Bearish Takeaways

- Bearish analysts highlight that expectations around UBS Group are already elevated, which they believe increases the risk that any slip in execution or revenue delivery could lead to disappointment relative to current targets.

- The downgrade to an Underperform rating, despite a higher price target of CHF 38, signals concern that the current share price may already reflect much of the forecast profit margin and P/E assumptions.

- References to a period where conditions for the bank are described as exceptionally strong underscore worries that current profitability might be difficult to sustain if operating conditions become less favorable.

- Mixed moves in targets, including at least one reduction, show that not all analysts see a clear path for UBS Group to justify higher valuations, and some prefer to factor in a wider range of outcomes around growth and returns.

What’s in the News for UBS Group

- UBS Group and Ethereum research firm Nethermind completed two joint proofs of concept showing that the public Ethereum network can meet operational and compliance standards for regulated financial institutions. They plan to continue collaborating on risk management and digital asset projects within strict regulatory frameworks (source: recent UBS and Nethermind announcement).

- UBS Group’s chief investment office has been advising clients to build portfolios that can handle a range of economic and geopolitical scenarios, encouraging regular reviews and rebalancing rather than relying on a single macro forecast (source: UBS investment guidance).

- UBS Group AG obtained an exemption that allows current and future UBS related asset managers to keep relying on Prohibited Transaction Exemption 84-14 through May 5, 2035. This is subject to specific fiduciary, compliance, audit, and indemnification conditions designed to protect employee benefit plans (source: U.S. Department of Labor notice).

- UBS Group AG saw the termination of a prior Federal Reserve Board Cease and Desist Order dated July 21, 2023. The order was formally ended on May 12, 2026, removing that specific enforcement action from the current regulatory backdrop (source: Federal Reserve Board enforcement records).

- UBS Group AG reported the completion of a share repurchase tranche covering 20,400,000 shares, representing 0.66% of its share capital, for a total of US$850 million under the buyback program announced on February 4, 2026 (source: company buyback update).

Valuation Changes for UBS Group

- Fair Value: CHF 40.57 compared with the prior CHF 38.38, signaling a higher central estimate for UBS Group.

- Discount Rate: 9.02% versus 8.99% previously, a very small upward adjustment to the rate used to value future cash flows.

- Revenue Growth: projected revenue growth of 2.43% compared with 2.96% previously, indicating slightly more conservative top line expectations.

- Net Profit Margin: 25.66% compared with 25.42% previously, reflecting a modestly higher expected level of profitability.

- Future P/E: 13.40x versus 12.93x previously, pointing to a slightly higher valuation multiple applied to UBS Group earnings in analyst models.

Key Takeaways

- Integration of Credit Suisse and investment in digital infrastructure are enhancing efficiency, scalability, and profitability, boosting margins and long-term earnings potential.

- Global wealth management leadership and growing demand for high-margin solutions position UBS for recurring revenue growth and diversified income streams amid favorable market trends.

- Rising regulatory burdens, capital requirements, margin compression, and challenging integration risks threaten UBS's profit growth and may limit capital deployment for expansion or shareholder returns.

Catalysts

About UBS Group- Provides financial advice and solutions to private, institutional, and corporate clients worldwide.

- The ongoing integration of Credit Suisse is progressing ahead of schedule, driving meaningful cost savings, increased scale, and improved operating efficiency; as these synergies are realized through further platform migration and operational streamlining, UBS's net margins and return on equity are likely to improve, supporting higher earnings growth.

- UBS's global leadership in wealth management and strong asset flows-especially in Asia-Pacific, EMEA, and the Americas-positions it to benefit from rising global wealth and high-net-worth client growth, which should drive topline revenue expansion and highly recurring fee income as intergenerational wealth transfer accelerates.

- Significant investment in digital infrastructure, AI-powered client solutions, and operational automation (e.g., the rollout of in-house AI assistant and expanded Microsoft Copilot access) is expected to increase differentiation, expand UBS's scalable client base, and lower expense ratios over time, further boosting operating margins and profitability.

- Heightened client demand for mandates, higher-margin discretionary solutions, and alternative investments-including robust growth in UBS's Unified Global Alternatives unit-supports recurring revenues and asset management fees, leveraging long-term shifts toward sustainable and diversified investing.

- Globalization of capital markets and UBS's expansive cross-border franchise are driving market share gains in trading, FX, and advisory revenues, providing diversified revenue streams that are positioned to benefit as client conviction and capital deployment accelerate, especially as macroeconomic uncertainty subsides.

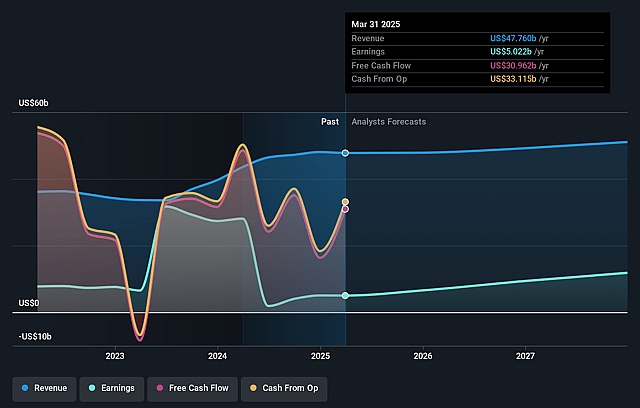

UBS Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming UBS Group's revenue will grow by 2.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 17.8% today to 25.7% in 3 years time.

- Analysts expect earnings to reach $14.1 billion (and earnings per share of $4.74) by about July 2029, up from $9.1 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $16.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.4x on those 2029 earnings, down from 16.5x today. This future PE is lower than the current PE for the GB Capital Markets industry at 15.5x.

- Analysts expect the number of shares outstanding to decline by 2.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.02%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The proposed changes to Switzerland's capital regime and early Basel III finalization would require UBS to hold $24–$42 billion in additional capital, significantly impacting return on tangible equity and potentially reducing the group's ability to deploy capital for growth, shareholder returns, or higher earnings.

- Rising global regulatory scrutiny and expected longer-term increases in compliance burdens (especially for cross-border banking, KYC, resolution planning, and ESG standards), are likely to drive structural increases in operational expenses and legal risk, eroding long-term net margins.

- Persistent margin compression in core businesses (particularly Asset Management, where clients continue rotating into lower-margin products, and Investment Banking as competition with passive investing and algorithmic trading intensifies) could limit UBS's ability to grow revenues and maintain current profit levels.

- Ongoing macroeconomic uncertainties in key markets (especially Switzerland and Europe), combined with prolonged low or negative interest rate environments, directly pressure net interest income and lending profitability-seen clearly in recent Swiss Personal & Corporate Banking performance, which may further constrain future earnings.

- The successful integration of Credit Suisse, though progressing, still carries multi-year execution risks-including restructuring costs, client attrition, IT decommissioning delays, and potential underperformance relative to targeted cost savings-which could weigh on net margins and overall group profitability longer than currently expected.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CHF40.57 for UBS Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF60.0, and the most bearish reporting a price target of just CHF33.99.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $55.1 billion, earnings will come to $14.1 billion, and it would be trading on a PE ratio of 13.4x, assuming you use a discount rate of 9.0%.

- Given the current share price of CHF40.06, the analyst price target of CHF40.57 is 1.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on UBS Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.