Last Update 03 Jun 26

Fair value Decreased 31%SHAK: Reset Guidance And New CFO Will Test Rich Forward P/E Multiple

Analysts have reduced the Shake Shack fair value estimate to $66 from $95, citing a series of lowered price targets across the Street following Q2 guidance cuts, tempered same-store sales expectations, and updated 2026 EBITDA guidance, even as some still see attainable targets and ongoing value in the stock.

Analyst Commentary

Street research on Shake Shack has turned more cautious after the Q2 guidance update, with several bearish analysts cutting price targets and reassessing the risk profile tied to execution and growth.

One firm reduced its price target to US$70 from US$85 and highlighted that, while the guidance reduction was disappointing, the revised targets are viewed as more aligned with current trends. The same research pointed to the arrival of a new CFO as a potential support for tighter financial oversight, while still seeing value in the stock at current levels.

Another bearish analyst brought their price target down to US$82 from US$100 but maintained a positive rating, signaling that, even with a lower valuation framework, they still see room for the stock if execution improves over time.

Jefferies cut its price target to US$66 from US$76 and kept a Hold rating after management lowered Q2 same-store sales and restaurant level margin guidance, along with revising 2026 EBITDA guidance to a range of US$225m to US$235m from US$230m to US$245m. Jefferies also flagged ongoing macro headwinds and more tempered expectations around the World Cup impact, which, in their view, weigh on the near term outlook.

Earlier in the year, several other bearish analysts also lowered price targets by double digit dollar amounts. At the same time, JPMorgan and other major firms had previously raised targets or initiations at higher levels. The shift from those earlier, more optimistic targets to current, lower levels underlines how sentiment has cooled as guidance has been reset.

Bearish Takeaways

- Bearish analysts have cut price targets across the board, compressing valuation expectations as guidance for same-store sales, margins, and 2026 EBITDA has been reset.

- The reduction of 2026 EBITDA guidance to US$225m to US$235m from US$230m to US$245m highlights execution risk around reaching prior profitability ambitions.

- Commentary around macro headwinds and more cautious World Cup expectations points to external pressures that could limit near term growth and margin expansion.

- Earlier upward target moves from firms such as JPMorgan now sit alongside a series of recent cuts, signaling a more balanced but less enthusiastic view of the stock's risk and reward profile.

What’s in the News

- Q1 2026 results: revenue of US$366.74m, up 14.3% year over year with 4.6% same Shack sales growth and 17 new locations opened, but the company reported break-even EPS of US$0.00 versus Wall Street expectations of US$0.11 and a US$2.6m operating loss, with adjusted EBITDA margin at 10.1% versus 12.7% a year earlier (source: Q1 2026 earnings coverage).

- Guidance reset and stock reaction: management reaffirmed full year 2026 revenue guidance but lowered earnings guidance and trimmed some profitability forecasts, alongside more cautious same store sales and new opening expectations, and the stock price fell about 28% to 30% on May 7, 2026 following the update (sources: Q1 2026 earnings coverage, guidance update reports).

- Legal scrutiny: multiple law firms, including Pomerantz LLP, Schall Law Firm, and Kessler Topaz Meltzer & Check, LLP, launched investigations into potential securities law violations after the Q1 2026 operating loss and net loss disclosures and the more than 28% single-day share price decline (source: law firm investigation announcements).

- Insider and founder buying: founder Danny Meyer purchased about US$2m of stock after the post-earnings drop, alongside additional insider share purchases in May, which some investors view as a signal of internal confidence in the company despite profitability pressures and technology overhaul costs (source: insider activity reports).

- Leadership and growth initiatives: the company appointed Michelle Hook as CFO effective May 11, 2026, outlined Project Catalyst to upgrade technology and launch a loyalty program, and continued geographic expansion with its first Western Canada Shack in Calgary, which includes local menu items and partnerships (sources: company executive announcement, Project Catalyst release, Calgary opening announcements).

Valuation Changes

- Fair Value: cut from $95.00 to $66.00, a large reset that brings the modeled upside closer to recent Street targets.

- Discount Rate: risen slightly from 8.79% to 9.22%, reflecting a higher required return for the stock.

- Revenue Growth: trimmed from 14.08% to 12.92%, pointing to more conservative assumptions for future dollar revenue expansion.

- Net Profit Margin: reduced from 4.31% to 4.04%, signaling a modestly lower expected share of dollar revenue flowing through to earnings.

- Future P/E: brought down from 52.88x to 39.62x, implying a lower valuation multiple applied to projected earnings.

Key Takeaways

- Shifting consumer preferences, regulatory pressure, and rising input costs threaten Shake Shack's growth prospects and margin stability.

- Labor market challenges and increased competition may limit innovation effectiveness and erode long-term market share.

- Aggressive expansion, operational improvements, digital investments, and disciplined financial management are positioning the brand for sustained growth in revenue, margins, and earnings.

Catalysts

About Shake Shack- Owns, operates, and licenses Shake Shack restaurants (Shacks) in the United States and internationally.

- Intensifying health consciousness and mounting anti-fast food sentiment threaten to fundamentally erode Shake Shack's long-term traffic and sales growth, particularly as increasing calories and portion sizes from menu innovation directly conflict with evolving consumer preferences, ultimately limiting revenue expansion.

- Accelerating regulatory scrutiny, including possible taxation on processed foods and animal proteins, will likely impose additional costs and constrain Shake Shack's ability to flexibly manage its menu, leading to compressed net margins and diminished earnings power over time.

- Persistent labor market tightness in urban and suburban areas, along with sustained wage inflation, is set to push payroll expense higher; this will pressure Shake Shack's operating margins as future hiring and retention demands outstrip available productivity gains.

- The company's ongoing reliance on new menu innovation is at risk of falling behind competitors, as more agile rivals and digitally native brands drive greater differentiation and frequency, resulting in decelerating same-store sales growth and long-term market share losses.

- Volatile input costs, particularly the continued rise in beef and other commodities due to climate change and supply chain instability, are projected to reduce gross margins, challenge cost controls, and constrain Shake Shack's ability to achieve its long-range adjusted EBITDA targets.

Shake Shack Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Shake Shack compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Shake Shack's revenue will grow by 12.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 2.8% today to 4.0% in 3 years time.

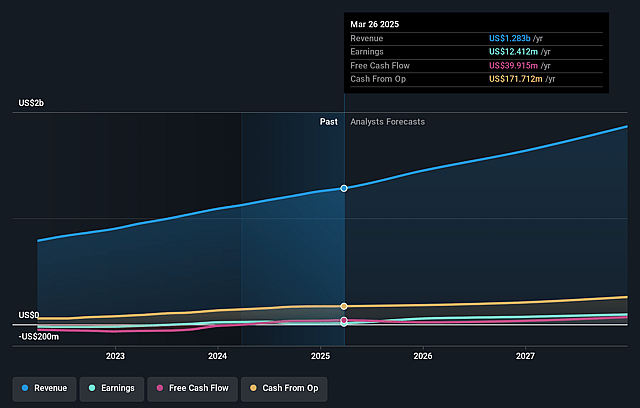

- The bearish analysts expect earnings to reach $86.8 million (and earnings per share of $2.0) by about June 2029, up from $41.2 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $108.9 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 40.3x on those 2029 earnings, down from 55.8x today. This future PE is greater than the current PE for the US Hospitality industry at 20.3x.

- The bearish analysts expect the number of shares outstanding to grow by 0.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.22%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Shake Shack has demonstrated 18 consecutive quarters of positive same-store sales growth, ongoing double-digit adjusted EBITDA growth, and expanding restaurant-level margins, indicating the potential for sustained increases in revenue, margins, and earnings over the long term.

- The company is executing its largest class of new openings in history, with 45 to 50 company-operated and 35 to 40 licensed locations expected in the coming year, which is likely to drive significant topline growth and support increased system-wide earnings.

- Investment in digital channels, supply chain optimizations, and operational efficiency programs-like new kitchen prototypes, labor guides, and standardized scorecards-are already yielding substantial improvements in both restaurant-level and company-wide net margins.

- Shake Shack is accelerating its brand and traffic growth by moving into scaled paid media advertising for the first time and leveraging an 18-month pipeline of culinary innovation, which is demonstrated to be mix

- and margin-accretive, thereby increasing both customer frequency and average check size.

- The company has maintained strong financial discipline, with positive operating cash flow, a strong cash position, and explicit long-term guidance to grow revenue and EBITDA at low double-digit rates annually, underpinned by favorable trends in urban foot traffic recovery, global expansion, and consumer demand for premium fast-casual dining-implying robust potential for future net income growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Shake Shack is $66.0, which represents up to two standard deviations below the consensus price target of $93.54. This valuation is based on what can be assumed as the expectations of Shake Shack's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $150.0, and the most bearish reporting a price target of just $66.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $2.1 billion, earnings will come to $86.8 million, and it would be trading on a PE ratio of 40.3x, assuming you use a discount rate of 9.2%.

- Given the current share price of $57.01, the analyst price target of $66.0 is 13.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Shake Shack?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.