Key Takeaways

- Shifting consumer preferences, regulatory pressure, and rising input costs threaten Shake Shack's growth prospects and margin stability.

- Labor market challenges and increased competition may limit innovation effectiveness and erode long-term market share.

- Aggressive expansion, operational improvements, digital investments, and disciplined financial management are positioning the brand for sustained growth in revenue, margins, and earnings.

Catalysts

About Shake Shack- Owns, operates, and licenses Shake Shack restaurants (Shacks) in the United States and internationally.

- Intensifying health consciousness and mounting anti-fast food sentiment threaten to fundamentally erode Shake Shack's long-term traffic and sales growth, particularly as increasing calories and portion sizes from menu innovation directly conflict with evolving consumer preferences, ultimately limiting revenue expansion.

- Accelerating regulatory scrutiny, including possible taxation on processed foods and animal proteins, will likely impose additional costs and constrain Shake Shack's ability to flexibly manage its menu, leading to compressed net margins and diminished earnings power over time.

- Persistent labor market tightness in urban and suburban areas, along with sustained wage inflation, is set to push payroll expense higher; this will pressure Shake Shack's operating margins as future hiring and retention demands outstrip available productivity gains.

- The company's ongoing reliance on new menu innovation is at risk of falling behind competitors, as more agile rivals and digitally native brands drive greater differentiation and frequency, resulting in decelerating same-store sales growth and long-term market share losses.

- Volatile input costs, particularly the continued rise in beef and other commodities due to climate change and supply chain instability, are projected to reduce gross margins, challenge cost controls, and constrain Shake Shack's ability to achieve its long-range adjusted EBITDA targets.

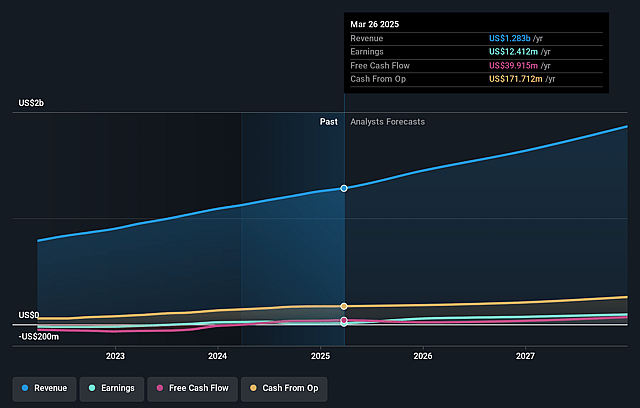

Shake Shack Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Shake Shack compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Shake Shack's revenue will grow by 14.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 1.5% today to 5.8% in 3 years time.

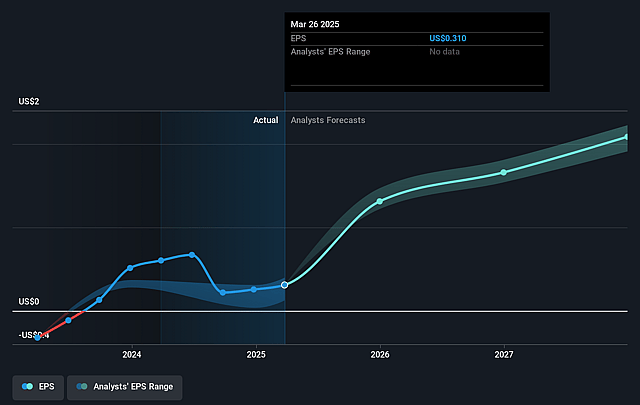

- The bearish analysts expect earnings to reach $115.3 million (and earnings per share of $2.21) by about August 2028, up from $19.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 52.9x on those 2028 earnings, down from 213.7x today. This future PE is greater than the current PE for the US Hospitality industry at 22.5x.

- Analysts expect the number of shares outstanding to grow by 0.66% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.87%, as per the Simply Wall St company report.

Shake Shack Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Shake Shack has demonstrated 18 consecutive quarters of positive same-store sales growth, ongoing double-digit adjusted EBITDA growth, and expanding restaurant-level margins, indicating the potential for sustained increases in revenue, margins, and earnings over the long term.

- The company is executing its largest class of new openings in history, with 45 to 50 company-operated and 35 to 40 licensed locations expected in the coming year, which is likely to drive significant topline growth and support increased system-wide earnings.

- Investment in digital channels, supply chain optimizations, and operational efficiency programs-like new kitchen prototypes, labor guides, and standardized scorecards-are already yielding substantial improvements in both restaurant-level and company-wide net margins.

- Shake Shack is accelerating its brand and traffic growth by moving into scaled paid media advertising for the first time and leveraging an 18-month pipeline of culinary innovation, which is demonstrated to be mix

- and margin-accretive, thereby increasing both customer frequency and average check size.

- The company has maintained strong financial discipline, with positive operating cash flow, a strong cash position, and explicit long-term guidance to grow revenue and EBITDA at low double-digit rates annually, underpinned by favorable trends in urban foot traffic recovery, global expansion, and consumer demand for premium fast-casual dining-implying robust potential for future net income growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Shake Shack is $110.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Shake Shack's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $162.0, and the most bearish reporting a price target of just $110.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $2.0 billion, earnings will come to $115.3 million, and it would be trading on a PE ratio of 52.9x, assuming you use a discount rate of 8.9%.

- Given the current share price of $105.6, the bearish analyst price target of $110.0 is 4.0% higher. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.