Last Update 21 Apr 26

Fair value Decreased 2.33%BILI: AI Engagement And Margin Execution Will Support Higher Future Fair Value

The updated analyst price target for Bilibili now points to a slightly lower fair value of about $37.90 per share versus $38.81 previously, as analysts factor in higher expected revenue growth and profit margins, along with a lower future P/E assumption and a modestly higher discount rate following recent upgrades that cite AI investment and user engagement trends.

Analyst Commentary

Recent Street research has tilted more positive on Bilibili, with several bullish analysts shifting their views to more constructive stances and updating price targets. While there is some variation in individual assumptions, the common thread is growing confidence in management's execution on AI, user engagement, and monetization initiatives, along with a willingness among some firms to move off the sidelines and issue more favorable ratings.

One key reference point is the upgrade to Overweight from Neutral at JPMorgan, which came with a price target of $35, revised from $27. That move followed a share price pullback of about 26% from a recent January peak, with JPMorgan explicitly characterizing the setup as an opportunity to "bottom fish" at lower levels. In that context, the latest blended fair value estimate of about $37.90 a share sits modestly above JPMorgan's $35 target, but broadly in the same range of expectations for what the stock could be worth under current assumptions.

JPMorgan's research flagged Bilibili's increased AI investment as a central part of the equity story, arguing that AI has already become a major driver of user engagement and advertising revenue. In that view, greater AI spending is not just a cost item, but a key lever that could support the premium valuation inputs analysts are using, particularly where models assume healthier revenue trends and firmer profit margins over time.

Beyond JPMorgan, other bullish analysts have also upgraded Bilibili following share price weakness, framing the reset in the stock as a chance for investors to reassess the risk reward profile. Multiple upgrades clustered in a short time window suggest a more constructive tone around the name, even as some targets, such as the $1 cut cited by BofA, show that expectations are being fine tuned rather than moving in only one direction.

Taken together, this mix of higher rating stances, AI focused research arguments, and recalibrated price targets helps explain why the updated consensus fair value estimate is only slightly below the prior figure, despite changes to assumptions on discount rates and future P/E. The Street appears to be weighing a more conservative valuation framework against still constructive views on Bilibili's ability to execute on user growth and monetization.

Bullish Takeaways

- JPMorgan's upgrade to Overweight, paired with a higher price target of $35 from $27, signals that at least one major global firm now sees the risk reward skew as more favorable after the stock's roughly 26% pullback from its recent January peak.

- JPMorgan's view that Bilibili is a "solid profit compounder" reflects confidence that the company can translate user engagement and advertising momentum into sustained margin improvement, which supports the use of higher earnings power in valuation models.

- Bullish analysts highlight Bilibili's push into AI as a core positive driver, arguing that AI is already a major contributor to user engagement and ad revenue, which in turn can support revenue growth trajectories that underpin current price targets and fair value estimates.

- The cluster of upgrades following share price weakness suggests that some bullish analysts see the recent correction as an entry point rather than a red flag, reinforcing the idea that execution on AI and user engagement could justify current valuation assumptions over time.

What's in the News

- Bilibili plans to hold its annual general meeting on June 17, 2026, where shareholders will vote on adopting new Articles of Association that would replace the current version in order to meet Rule 8A.44 requirements for weighted voting rights issuers and include housekeeping updates (Key Developments).

- The proposed New Articles of Association are intended to give effect to Rule 8A.27 of the Listing Rules by embedding those requirements directly into the company’s governing documents (Key Developments).

- The board has scheduled a meeting for March 5, 2026, to consider and approve Bilibili’s unaudited financial results for the fourth quarter and full year ended December 31, 2025 (Key Developments).

Valuation Changes

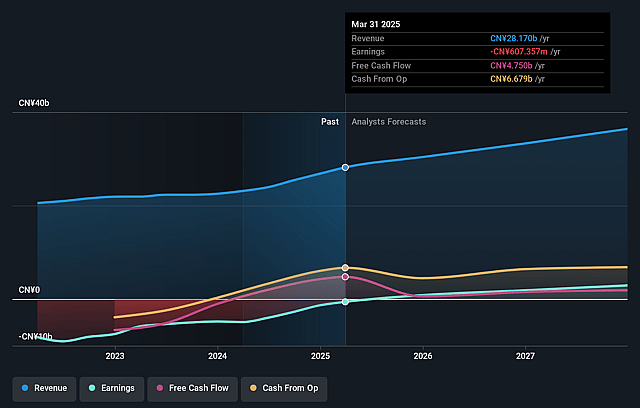

- Fair Value: Updated fair value moves slightly lower to $37.90 from $38.81 per share, indicating only a modest adjustment in the overall valuation output.

- Discount Rate: The discount rate is set at 9.50%, compared with 9.27% previously. This is a small upward move that makes future cash flows less valuable in the model.

- Revenue Growth: The CN¥ revenue growth assumption is now 13.59% versus 10.99% before, representing a moderate step up in expected top line expansion.

- Net Profit Margin: The CN¥ net profit margin assumption rises to 12.26% from 11.26%, indicating slightly stronger projected profitability.

- Future P/E: The future P/E multiple is reduced to 25.62x from 32.13x, a meaningful reset that places less weight on higher earnings multiples in the updated model.

Key Takeaways

- AI-driven ad upgrades, strong engagement, and ecosystem scaling position Bilibili for outperformance in monetization, user loyalty, and cross-platform revenue growth.

- Durable marquee games, unmatched Gen Z+ appeal, and advanced proprietary AI enable sustained ARPU expansion and significant structural profit gains.

- Rising content costs, regulatory risks, demographic challenges, and global uncertainties threaten Bilibili's ability to sustain growth, profitability, and international expansion.

Catalysts

About Bilibili- Provides online entertainment services for the young generations in the People’s Republic of China.

- Analyst consensus expects ongoing strength in advertising, but the scale of Bilibili's AI-driven ad infrastructure upgrades and record high engagement metrics could drive compounding, above-industry advertising and e-commerce growth, resulting in operating leverage and significant outperformance in both revenue and gross profit.

- Consensus recognizes new game launches as a driver, but the durability of marquee titles like San Mou-with proven potential as multi-year monetization engines, cross-market rollouts, and continuous in-game monetization tools-sets the stage for Bilibili's games revenue to structurally re-rate higher, with far greater impact on net income than analysts expect.

- Bilibili's unmatched hold on Gen Z+ mindshare and its dominance in longer-form, interactive video puts it at the center of a broad generational migration towards participatory, high-engagement platforms, enabling above-peer user monetization for years to come and leading to sustained ARPU expansion.

- The underappreciated scaling of Bilibili's integrated digital and offline ecosystem-including massive ACG events, growing international influence, and cultural brand leadership-provides a unique flywheel for user loyalty and category-leading cross-platform revenues.

- Bilibili's proprietary AI tools, trained on a uniquely rich set of organic user feedback signals, are poised to lower content costs while sharply amplifying content quality and creator productivity, directly supporting structural margin expansion and improving long-term profit growth.

Bilibili Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Bilibili compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Bilibili's revenue will grow by 13.6% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 3.9% today to 12.3% in 3 years time.

- The bullish analysts expect earnings to reach CN¥5.5 billion (and earnings per share of CN¥12.02) by about April 2029, up from CN¥1.2 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CN¥2.6 billion.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 25.7x on those 2029 earnings, down from 59.4x today. This future PE is greater than the current PE for the US Interactive Media and Services industry at 16.0x.

- The bullish analysts expect the number of shares outstanding to decline by 0.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.5%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Growing content acquisition and production costs, particularly with rising competition for premium IP and an increasing creator income base of 2 million, could compress gross margins and threaten long-term profitability, making it more difficult for Bilibili to sustainably expand earnings.

- Recent net income and margin improvements rely heavily on scalable hit content and robust advertising and games momentum, but fierce competition from well-capitalized rivals and the shifting adoption of decentralized and AI-driven media could undermine market share and slow revenue growth versus user base expansion.

- China's ongoing regulatory scrutiny and unpredictable policy environment for online communities and digital content may constrain user engagement and limit the launch or monetization of new features, posing material downside risk to both revenues and net income.

- The company's growth remains highly tethered to a youth-oriented Gen Z+ demographic, yet China's demographic headwinds-including a shrinking youth cohort and aging population-threaten to structurally slow Bilibili's long-term user growth and dampen future revenue streams.

- Efforts to expand globally and diversify market exposure, such as rolling out games internationally and attracting foreign attendees to events, face substantial risk from intensifying geopolitical tensions and the decoupling of China and the West, which could restrict international revenue potential and limit access to global partnerships or capital.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Bilibili is $37.9, which represents up to two standard deviations above the consensus price target of $31.15. This valuation is based on what can be assumed as the expectations of Bilibili's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $37.94, and the most bearish reporting a price target of just $21.23.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be CN¥44.5 billion, earnings will come to CN¥5.5 billion, and it would be trading on a PE ratio of 25.7x, assuming you use a discount rate of 9.5%.

- Given the current share price of $24.97, the analyst price target of $37.9 is 34.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Bilibili?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.