Last Update 21 Apr 26

Fair value Decreased 2.14%PDN: Outperform Upgrade And EIS Approval Will Support Future Upside

Analysts have trimmed their fair value estimate for Paladin Energy from about A$17.49 to A$17.11, citing updated cost assumptions at Langer Heinrich, as well as expectations for stronger revenue growth, higher profit margins, and a lower future P/E multiple.

Analyst Commentary

Recent Street research reflects a more constructive tone on Paladin Energy, with bullish analysts pointing to valuation support and updated cost assumptions at Langer Heinrich as key drivers behind their views.

Bullish Takeaways

- Paladin Energy has been upgraded to an Outperform rating, which signals increased confidence in the shares at current levels.

- The updated A$13.50 price target is framed as attractive versus the recent share pullback, suggesting potential upside if execution stays on track.

- Bullish analysts acknowledge higher cost forecasts at Langer Heinrich, yet still see value in the equity, indicating that revised assumptions are already reflected in their models.

- The combination of a rating upgrade and a defined price target gives investors a clearer sense of how bullish analysts are valuing Paladin Energy based on their current revenue and margin expectations.

What's in the News

- Paladin Energy received Ministerial approval for its Environmental Impact Statement under The Environmental Assessment Act in Saskatchewan for the Patterson Lake South Project in the Athabasca Basin, Canada, clearing a key regulatory step toward future permitting for construction and operation (Key Developments).

- The Saskatchewan Minister of Environment formally approved the Environmental Impact Statement for the shallow, high grade Patterson Lake South Project following technical acceptance in June 2025 (Key Developments).

- The approval followed an extensive public review period from July to September 2025, which was part of the regulatory process leading up to this Environmental Assessment decision (Key Developments).

Valuation Changes

- Fair Value: Trimmed slightly from A$17.49 to A$17.11, reflecting updated assumptions in the model.

- Discount Rate: Held steady at 6.85%, indicating no change in the required return used in the valuation work.

- Revenue Growth: Assumed long term dollar revenue growth has risen modestly from 61.42% to 63.00%.

- Net Profit Margin: Forecast dollar net profit margin has edged up from 21.48% to 22.62%.

- Future P/E: Forward price-to-earnings multiple has been reduced from 38.22x to 35.19x, signalling a lower valuation multiple applied to future earnings.

Key Takeaways

- Operational improvements and expansion opportunities at core assets may boost revenue growth and profitability beyond what current forecasts and consensus expect.

- Strong market demand, strategic partnerships, and long-term premium contracts position the company to achieve improved earnings visibility and sustained margin expansion.

- Heavy dependence on uranium, operational concentration, regulatory hurdles, rising capital needs, and uncertain market dynamics could elevate earnings volatility and financial risk.

Catalysts

About Paladin Energy- Engages in the development, exploration, evaluation, and operation of uranium mines in Australia, Canada, and Namibia.

- Analysts broadly agree that the successful ramp-up of Langer Heinrich is driving Paladin's production growth, but what is likely understated is the company's capacity to move beyond nameplate levels post-2027, with a cycle of continuous operational gains positioning Paladin as the next leading swing producer and meaningfully boosting revenue over current forecasts.

- While consensus highlights the PLS project's robust economics and progress on development, a far more bullish scenario sees Paladin leveraging strategic partnerships and early utility customer demand to fast-track both contracting and financing, bringing forward PLS cash flows and sharply increasing the company's medium-term earnings growth profile.

- Surging global utility interest in securing non-Russian, western uranium supply is leading to unusually strong forward contracting conditions, which uniquely positions Paladin to lock in long-term, premium pricing contracts-this will significantly raise contracted revenue visibility and support margin expansion for years to come.

- The severe and persistent global uranium supply deficit, alongside growing commitment to nuclear from major economies, could lead to a step change in uranium prices well above current consensus, enabling Paladin to generate supernormal profitability given its low-cost operations and rising production base.

- Paladin's large, underexplored resource base at both Langer Heinrich and the PLS region offers exceptional optionality-ongoing and future drilling programs are set to unlock material reserve and resource upgrades, paving the way for further production expansions that are not yet reflected in current valuations or earnings expectations.

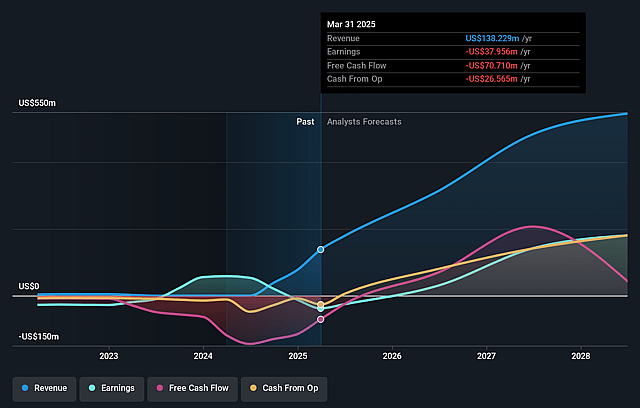

Paladin Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Paladin Energy compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Paladin Energy's revenue will grow by 63.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -16.4% today to 22.6% in 3 years time.

- The bullish analysts expect earnings to reach $233.9 million (and earnings per share of $0.53) by about April 2029, up from -$39.2 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $178.0 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 35.2x on those 2029 earnings, up from -111.8x today. This future PE is greater than the current PE for the AU Oil and Gas industry at 17.1x.

- The bullish analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.85%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Paladin's reliance on uranium demand tied to new nuclear build could be threatened by the accelerating global shift toward renewables and alternative grid storage technologies, potentially slowing long-term revenue growth if nuclear fails to maintain its share in the electricity mix.

- Heavy concentration of operations at Langer Heinrich exposes Paladin to risk of operational or geopolitical disruptions in Namibia, where any major interruption could materially impact production, shrinking near-term and long-run revenues and causing significant earnings volatility.

- The path to first production at the Patterson Lake South (PLS) project is long and subject to regulatory complexity in Canada, so any delays or unfavorable shifts in permitting or stakeholder agreements could defer or undermine projected revenue and earnings contributions from this major growth asset.

- Escalating upfront capital costs at PLS-combined with management's openness to debt, equity, or strategic partnerships-raise the specter of further shareholder dilution or elevated financial risk if spot uranium prices underperform, directly pressuring net margins and earnings per share.

- The industry faces persistent risk of uranium oversupply from major producers (Kazakhstan, Canada, Niger) re-entering or ramping up production, which could suppress uranium prices, squeeze Paladin's operating margins, and weigh on top-line revenues over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Paladin Energy is A$17.11, which represents up to two standard deviations above the consensus price target of A$12.54. This valuation is based on what can be assumed as the expectations of Paladin Energy's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$17.11, and the most bearish reporting a price target of just A$6.92.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $1.0 billion, earnings will come to $233.9 million, and it would be trading on a PE ratio of 35.2x, assuming you use a discount rate of 6.9%.

- Given the current share price of A$13.61, the analyst price target of A$17.11 is 20.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Paladin Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.