Last Update 11 Jan 26

BZUN: Future Returns Will Depend On Balancing Demand Shifts And Earnings Durability

Analysts have raised their price target on Baozun, citing updated expectations for revenue growth, profit margins and future P/E multiples that they believe better align the stock with current sector peers, though they have not provided a specific US$ value for the new target in the sources referenced here.

Analyst Commentary

Bearish analysts looking at Baozun are not drawing direct conclusions from the Kanzhun target change itself, but they are using similar valuation questions to frame their concerns. When they look at e commerce and internet service peers that have had price targets adjusted, they often point to risks around how quickly demand trends can shift and how that might affect what investors are willing to pay on a P/E basis.

These more cautious views generally center on whether current expectations for growth, profitability and valuation multiples leave enough room for execution hiccups or slower end market demand. For you as an investor, that translates into a closer focus on how much optimism is already reflected in Baozun’s share price and how sensitive that could be to any disappointment in future updates.

Bearish Takeaways

- Bearish analysts worry that expectations for revenue growth and margins could be ahead of what recent demand trends in the broader internet and e commerce space might support, which could leave Baozun’s P/E multiple exposed if sentiment cools.

- They highlight the risk that if underlying customer demand for online services moderates, even slightly, investors could reassess how much they are willing to pay for future earnings, putting pressure on price targets for companies like Baozun.

- Some cautious views focus on execution risk, where any delay in improving profitability or scaling new initiatives could prompt investors to apply a lower valuation multiple to the shares.

- There is also concern that sector wide re ratings, such as price target changes across similar internet and platform names, may signal a tighter range of acceptable valuation for Baozun if growth or margin delivery does not clearly support current expectations.

What's in the News

- Baozun has scheduled a board meeting for November 25, 2025, to approve the unaudited financial results and announcement for the third quarter ended September 30, 2025 (Key Developments).

Valuation Changes

- Fair Value: The fair value estimate is unchanged at 2.70, so there is no shift in the core valuation anchor used in this framework.

- Discount Rate: The discount rate remains at 13.76%, indicating no adjustment to the risk assumption applied to Baozun’s future cash flows.

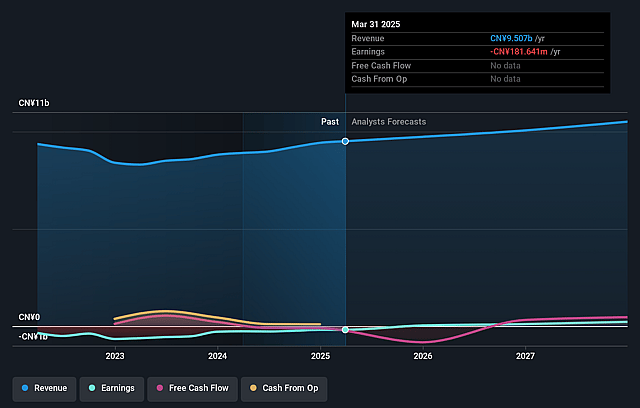

- Revenue Growth: Revenue growth expectations have risen from 3.20% to about 4.27%, a moderate upward move that signals slightly higher assumed top line expansion.

- Profit Margin: The profit margin input has fallen from about 3.32% to about 2.75%, which reflects a more cautious stance on how much profit Baozun might retain from its revenue.

- Future P/E: The future P/E multiple has risen from about 4.39x to about 5.10x, implying that the model now assumes a somewhat higher valuation applied to Baozun’s earnings outlook.

Key Takeaways

- Baozun faces structural demand decline, increased compliance costs, and intensifying competition that threaten long-term revenue growth and profitability.

- Ongoing operating losses and challenges with acquired brands put sustained profit recovery and margin expansion at risk.

- Sustained revenue growth, operational efficiencies, omnichannel leadership, expanding brand portfolio, and investments in proprietary technology position Baozun for long-term profitability and scalable earnings.

Catalysts

About Baozun- Through its subsidiaries, engages in the provision of end-to-end e-commerce solutions in the People's Republic of China.

- Baozun is heavily exposed to structurally declining discretionary consumer demand in China and wider Asia, a headwind driven by aging demographics and persistent macroeconomic stagnation, which could lead to lower order volumes and weaker revenue growth over the coming years.

- The rising complexity and cost of navigating tightening data security, cross-border e-commerce regulations, and escalating cybersecurity mandates will likely increase Baozun's compliance spending, weighing on net margins and reducing future profitability as international expansion becomes more expensive and uncertain.

- Intensifying competition from both major brands' in-house digital teams and low-cost third-party SaaS providers threatens to erode Baozun's value proposition, likely driving down client retention rates and service-based revenues in future periods.

- The continued growth of direct-to-consumer models among consumer brands combined with the expanding dominance of integrated retail giants such as Alibaba, JD.com, and Pinduoduo is expected to marginalize independent enablers like Baozun, shrinking its effective addressable market and constraining long-term top line growth.

- Persistent operating losses and the ongoing challenge of turning around recently acquired brands, particularly Gap China, increase the risk of future impairment charges and sustained group-level earnings drag, undermining prospects for sustainable profit recovery and margin expansion.

Baozun Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Baozun compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Baozun's revenue will grow by 2.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -1.9% today to 2.3% in 3 years time.

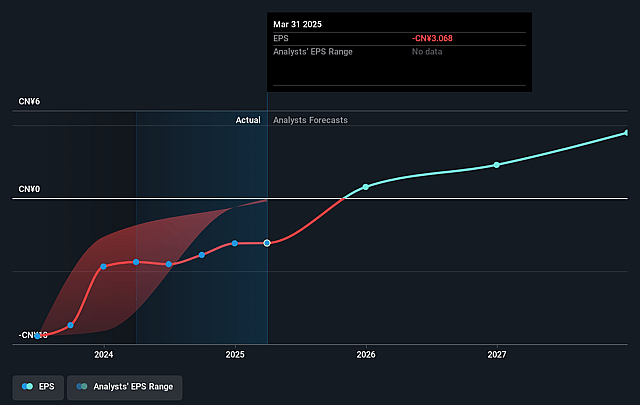

- The bearish analysts expect earnings to reach CN¥238.5 million (and earnings per share of CN¥8.12) by about September 2028, up from CN¥-185.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 7.0x on those 2028 earnings, up from -9.0x today. This future PE is lower than the current PE for the US Multiline Retail industry at 20.9x.

- Analysts expect the number of shares outstanding to decline by 2.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.27%, as per the Simply Wall St company report.

Baozun Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rapid and sustained revenue growth in key business segments, with BBM (brand management) posting 35% year-over-year revenue growth and recurring expansion in e-commerce services, could translate into strong top-line momentum for several years, challenging expectations of a share price decline.

- Increasing operational efficiency, evidenced by margin expansion in both e-commerce (gross margin up 110 basis points) and brand management (inventory days down over 20%), alongside targeted cost optimization, points to significant improvement in net margins and earnings quality over time.

- Baozun's leadership in omnichannel strategy and early adoption of new retail platforms such as Douyin, RedNote, and close partnerships with Tmall and JD provide ongoing tailwinds for market share gains, with higher-value service fees and new client acquisition likely to benefit future revenue and profitability.

- Successful expansion of the BBM brand portfolio, including additional brand acquisitions and the ability to onboard new brands efficiently using established systems from Gap and Hunter, creates the potential for high-margin, scalable recurring revenue streams and a diversified revenue base supporting long-term earnings growth.

- Continued investment in proprietary technology and AI-driven operational efficiency-such as leveraging 800-plus in-house engineers to drive automation, content creation, and supply chain optimization-will likely yield greater operating leverage and cost reductions, which should positively impact long-term operating margins and free cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Baozun is $3.02, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Baozun's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $6.0, and the most bearish reporting a price target of just $3.02.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be CN¥10.4 billion, earnings will come to CN¥238.5 million, and it would be trading on a PE ratio of 7.0x, assuming you use a discount rate of 13.3%.

- Given the current share price of $4.03, the bearish analyst price target of $3.02 is 33.5% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Baozun?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.