Last Update 02 Jul 26

Fair value Increased 3.34%COST: Membership Model And Q3 Execution Will Support Premium Multiple

Analysts have nudged the Costco Wholesale fair value estimate higher to $1,082.94 from $1,047.90, reflecting updated assumptions around slightly firmer profit margins, a modestly lower future P/E of about 50.7, and Street research that highlights the company's resilient membership model and balanced risk/reward at current levels.

Analyst Commentary

Recent Street research on Costco Wholesale presents a mix of confidence in the business model and caution around valuation, with price targets spread across a wide range and ratings spanning Buy, Hold, Neutral, and Sell. For readers, the key themes cluster around how much to pay for Costco's membership driven model, the sustainability of current execution, and what that implies for long term growth expectations embedded in the stock's P/E multiple.

Bullish Takeaways

- Bullish analysts highlight Costco's membership model and membership fee income as important supports for earnings quality and resilience, contributing to their willingness to underwrite higher fair value estimates.

- Some bullish analysts emphasize Costco's positioning as a primary stock up destination, helped by quality private label products, a curated general merchandise assortment, and ancillary offerings such as pharmacy, optical, and fuel that help sustain warehouse traffic.

- Positive commentary points to Costco's warehouse format as having one of the deeper moats in retail, with low prices, distribution efficiency on a relatively small SKU count, and recurring membership revenue all cited as reasons the business can justify premium valuation multiples.

- Several bullish analysts maintain or raise price targets into the US$1,000 plus range, citing what they view as balanced or attractive risk/reward at current levels, even while acknowledging that valuation is no longer discounted.

Bearish Takeaways

- Bearish analysts question whether Costco's current valuation, including references to enterprise value to expected EBITDA around 30x, is appropriate given signs of decelerating traffic and what they view as weaker or more costly member acquisition and retention efforts.

- Cautious commentary points out that membership growth is moderating and that new member additions, cited at over 800,000 in a recent period, sit below a referenced long term average of 1.1 million, which in their view tempers the long term growth narrative embedded in the stock.

- Some neutral to cautious voices frame Costco's risk/reward as balanced at present share levels, suggesting that while the company is seen as a long term market share gainer, much of that expectation may already be reflected in current price targets and the roughly 50.7 P/E assumption.

- There is also attention on short term execution items such as potential fuel related margin headwinds and traffic growth in the U.S. slowing to 1.8% from 2.4% in a recent quarter, which more cautious analysts view as reasons to be measured about upside from here.

What's in the News for Costco Wholesale

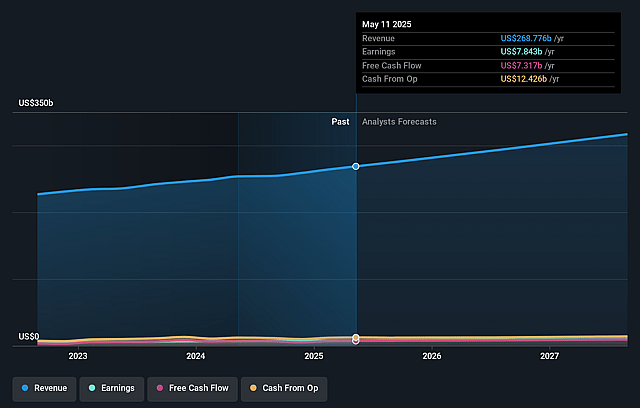

- Costco Wholesale reported fiscal Q3 2026 revenue of US$70.53b and adjusted EPS of US$4.93, with comparable sales up 9.8% globally and digital sales up 21.5%. Membership fee income rose 10.7% on a base of 82.9 million paid members, with renewal rates around 90% (Source: Q3 2026 earnings coverage).

- Despite record revenue and 15% earnings growth in recent quarters, Costco stock has pulled back from highs. Investors are weighing a premium forward P/E in the high 40s against concerns about inflation, consumer sentiment, tariff risks, and slowing membership growth (Sources: multiple Q3 2026 earnings stories).

- Costco is using artificial intelligence across its digital channels, with AI-tuned product pages helping drive a 3x increase in online traffic in fiscal Q3 2026 and the highest conversion rates on its digital platforms so far. Management points to AI as an important e commerce growth driver (Source: AI and digital strategy coverage).

- Membership fee changes remain in focus. The 2024 premium membership increase from US$120 to US$130 contributed to a 10.7% rise in adjusted membership fees in Q3 2026, while renewal rates in the U.S. and Canada stay around 90% to 92% (Sources: membership fee and earnings stories).

- Operationally, Costco continues to adjust its model. This includes record gasoline volumes from 747 gas stations, selective price cuts on Kirkland Signature items, and ongoing warehouse expansion plans of roughly 26 to 30 new locations per year. At the same time, some reports flag slower warehouse traffic growth of 2.4% in a recent quarter as a key watch point for the stock’s premium valuation (Sources: gas sales, pricing, traffic, and expansion coverage).

Valuation Changes for Costco Wholesale

- Fair Value: The updated fair value estimate has risen slightly to $1,082.94 from $1,047.90, reflecting small adjustments to key inputs.

- Discount Rate: The discount rate assumption has moved up modestly to 7.11% from 7.01%, implying a slightly higher required return in the model.

- Revenue Growth: The revenue growth assumption has been trimmed slightly to 7.35% from 7.52%, indicating a more measured outlook within the modelled range.

- Net Profit Margin: The profit margin assumption has edged up to 3.20% from 3.19%, indicating a small change in expected profitability for Costco Wholesale within the model.

- Future P/E: The future P/E multiple has been reduced modestly to about 50.7x from 51.3x, indicating a slightly lower valuation multiple applied to Costco stock in the updated analysis.

Key Takeaways

- Expansion of warehouse locations and gas station hours aims to increase membership, store traffic, and revenue growth.

- E-commerce growth and international market investments could boost overall earnings and diversify sales.

- Rising costs from labor, tariffs, and supply chains, along with foreign exchange fluctuations, could pressure Costco's margins and market competitiveness.

Catalysts

About Costco Wholesale- Engages in the operation of membership warehouses in the United States, Puerto Rico, Canada, Mexico, Japan, the United Kingdom, Korea, Australia, Taiwan, China, Spain, France, Iceland, New Zealand, and Sweden.

- Costco plans to continue expanding its warehouse locations, with 28 new openings planned for fiscal year 2025. This expansion is likely to increase membership and sales volume, driving revenue growth.

- Costco's extension of gas station hours is designed to enhance member convenience, which could lead to higher gasoline sales and increased store traffic, positively impacting revenue.

- The updated employee agreement with higher wages may initially increase SG&A expenses, but Costco's focus on labor productivity and cost discipline could help maintain net margins over time.

- E-commerce and digital channels show significant growth, with e-commerce comp sales up 22.2% adjusted for FX, suggesting a strong potential to boost revenue and earnings from online sales.

- Continued investment in international markets with new warehouse openings and the introduction of Executive Memberships in additional countries could further diversify and increase international sales, enhancing overall earnings potential.

Costco Wholesale Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Costco Wholesale's revenue will grow by 7.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.0% today to 3.2% in 3 years time.

- Analysts expect earnings to reach $11.6 billion (and earnings per share of $26.3) by about July 2029, up from $8.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 50.8x on those 2029 earnings, up from 46.4x today. This future PE is greater than the current PE for the US Consumer Retailing industry at 18.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Foreign exchange fluctuations have negatively impacted Costco's international sales and profits, introducing uncertainty into net income and earnings.

- Increased labor costs due to the updated employee agreement could pressure margins, as Costco plans to improve wages significantly over the next few years.

- Tariff unpredictability and potential trade tensions, especially with a significant portion of sales being imports, could impact future costs and profit margins adversely.

- Supply chain cost increases, as Costco invests in maintaining higher inventory levels amidst global delays, could exert pressure on core operating margins.

- Rising competition from other retailers might impact market share and revenues, especially if they struggle to maintain price leadership amidst inflationary pressures.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $1082.94 for Costco Wholesale based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $1315.0, and the most bearish reporting a price target of just $740.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $363.2 billion, earnings will come to $11.6 billion, and it would be trading on a PE ratio of 50.8x, assuming you use a discount rate of 7.1%.

- Given the current share price of $924.67, the analyst price target of $1082.94 is 14.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Costco Wholesale?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.