Last Update 16 Jun 26

Fair value Increased 28%NEM: Record Cash Generation And Buybacks Will Support Future Share Price

The analyst price target for Newmont has been revised higher from $110.65 to $141.46, with analysts citing updated models that factor in recent Q1 results, new coverage initiations, and mixed adjustments to cost and diesel price assumptions.

Analyst Commentary

Recent research on Newmont highlights a mix of optimistic and cautious views, with analysts updating models after Q1 results, revising cost assumptions, and fine tuning valuation targets for the stock.

Bullish Takeaways

- Bullish analysts point to stronger than expected Q1 results as a support for their investment cases, using these numbers to justify higher price targets or to maintain positive ratings on Newmont.

- Some bullish analysts are initiating or reiterating positive stances on Newmont with price targets that sit comfortably above recent trading levels, indicating they see room for valuation upside based on current assumptions.

- Positive commentary around the second half cadence and outlook suggests confidence that Newmont can execute on its operating plans, which feeds into higher earnings and cash flow expectations in their models.

- Where price targets are adjusted only modestly, bullish analysts appear comfortable with the overall thesis, viewing recent tweaks as fine tuning rather than a change in direction for Newmont stock.

Bearish Takeaways

- Bearish analysts are focusing on higher expected costs, including diesel prices, which feed directly into lower margin and cash flow assumptions and can cap how high they are willing to set price targets for Newmont.

- Several research updates involve reductions in price targets, even when Q1 results are described as stronger than expected, which signals concern that cost inflation or execution risks may offset some of the positive earnings surprise.

- Downgrades highlight a more cautious stance on the risk and reward profile, with concerns that higher operating and energy costs could limit Newmont’s ability to meet more optimistic projections embedded in bullish models.

- Target cuts from large firms, including global banks, indicate that some analysts see less headroom for valuation expansion at current levels, especially if cost pressures persist or planned second half improvements prove harder to deliver.

What’s in the News for Newmont

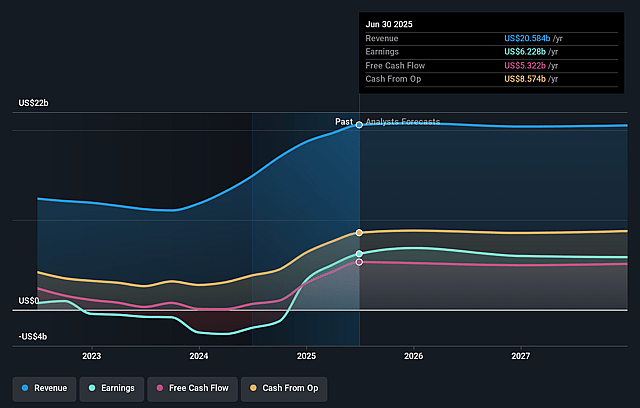

- Newmont reported record Q1 2026 results with adjusted EPS of $2.90, revenue of $7.31b, about 1.3 million attributable gold ounces, and free cash flow of $3.1b, while maintaining full year production guidance and reporting gold by product AISC of $1,029 per ounce (source: Newmont Reports Record Q1 Earnings and Expands $6 Billion Share Buyback Program).

- The company completed a prior $6b share repurchase authorization and the board approved an additional $6b buyback program alongside a $0.26 per share quarterly dividend, highlighting an ongoing capital return approach (sources: Newmont Reports Record Q1 Earnings and Expands $6 Billion Share Buyback Program; Buyback Transaction Announcements; Buyback Tranche Update).

- Newmont generated record Q1 free cash flow of $3.1b while reporting that softer gold prices and macro headwinds weighed on the stock price, with shares pulling back sharply around the earnings release (source: Newmont Reports Record Q1 Free Cash Flow Amid Falling Gold Prices and Expands $6 Billion Buyback).

- Newmont acquired about 13.32% of LunR, or 16,099,564 common shares, via a dividend in kind from Lundin Gold as part of its long term investment approach, and plans to review its position over time (source: Newmont Corporation Acquires 13.32% Stake in LunR via Dividend In Kind from Lundin Gold).

- The board appointed Brian Tabolt as Chief Financial Officer effective July 1, 2026, following his prior roles as Chief Accounting Officer, Group Head Finance, and interim CFO at Newmont (source: Executive Changes: CFO).

Valuation Changes for Newmont Stock

- Fair Value: Updated analyst fair value estimate increased from $110.65 to $141.46, a change of about 27.8%.

- Discount Rate: The discount rate assumption moved from 8.21% to 8.67%, a modest rise that implies a slightly higher required return.

- Revenue Growth: The forecast revenue growth rate shifted from 7.91% to 8.41%, indicating a slightly higher expected top line expansion in analyst models for Newmont.

- Net Profit Margin: The projected net profit margin increased from 36.95% to 41.86%, reflecting higher assumed profitability in future periods.

- Future P/E: The future P/E multiple moved from 13.92x to 13.35x, a small reduction that points to a slightly lower valuation multiple being applied to Newmont’s earnings outlook.

Key Takeaways

- Elevated gold demand and successful integration of acquired assets are set to drive stable long-term growth and strong cash flow performance.

- Focus on operational efficiency and ESG initiatives boosts margins, protects against regulatory risks, and enhances access to capital and valuation.

- Operational risks, declining asset quality, rising costs, reliance on divestments, and leadership transitions threaten Newmont's future revenue stability, earnings reliability, and cash flow.

Catalysts

About Newmont- Engages in the production and exploration of gold properties.

- Persistent global inflation and monetary debasement are likely to reinforce investor and central bank demand for gold, which will support higher sustained gold prices and directly increase Newmont's future revenues and earnings.

- Newmont's focus on operational stability, cost discipline, and productivity enhancements (e.g., at Lihir, Boddington, and across its core assets) is expected to drive lower operating costs and improved EBITDA margins, positioning the company for margin expansion and stronger net income over time.

- The realization of synergies and increased production scale following the Newcrest Mining acquisition, together with ongoing asset optimization and the ramp-up of expansion projects (such as Ahafo North and Tanami), should support long-term revenue growth and cash flow stability.

- Rising geopolitical tensions and wealth accumulation in emerging markets are likely to ensure resilient long-term demand for gold as a store of value, which should provide a strong macro tailwind for sustained revenue growth and upward revision in analyst outlooks.

- Newmont's continued investment in ESG initiatives, such as decarbonization, water management, and tailings remediation, enhances its reputation and access to capital with institutional investors, protects margins against potential regulatory costs, and supports premium valuation multiples over the long run.

Newmont Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Newmont's revenue will grow by 8.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 33.9% today to 41.9% in 3 years time.

- Analysts expect earnings to reach $13.3 billion (and earnings per share of $13.4) by about June 2029, up from $8.5 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $19.7 billion in earnings, and the most bearish expecting $9.7 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.4x on those 2029 earnings, up from 13.3x today. This future PE is lower than the current PE for the US Metals and Mining industry at 19.9x.

- Analysts expect the number of shares outstanding to decline by 2.81% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.67%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The fall of ground incidents at the Red Chris operation highlight potential operational safety and geotechnical risks, which could prompt costlier safety measures, production delays, regulatory scrutiny, and negatively affect future revenues and margins if similar disruptions occur or require ongoing investment.

- Several major assets, including Cadia, Peñasquito, and Lihir, are entering periods of lower-grade ore processing and planned production declines, suggesting future output and revenue may fall short of current strong results, especially if optimization initiatives do not fully offset mine sequencing headwinds.

- Planned increases in sustaining and development capital expenditures-especially for asset integrity, tailings remediation, and delayed shutdowns-will raise company-wide costs in the second half of the year and beyond, potentially compressing net margins and reducing free cash flow if commodity prices soften or cost-saving targets are not achieved.

- The heavy reliance on asset sales (e.g., Greatland Gold, Discovery Silver) and noncore divestments to fund capital returns implies that future shareholder distributions may be unsustainable once the current divestment pipeline is exhausted, placing long-term pressure on free cash flow and earnings if organic cash generation declines.

- Transition risks related to leadership changes (e.g., unexpected CFO departure, ongoing executive reshuffling) and complex integration of new assets could lead to strategic missteps, loss of institutional knowledge, and execution risk, threatening the stability of operations and negatively impacting earnings reliability over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $141.46 for Newmont based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $175.0, and the most bearish reporting a price target of just $72.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $31.8 billion, earnings will come to $13.3 billion, and it would be trading on a PE ratio of 13.4x, assuming you use a discount rate of 8.7%.

- Given the current share price of $105.8, the analyst price target of $141.46 is 25.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Newmont?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.