Last Update 23 Jun 26

Fair value Increased 3.87%ROKU: Fox Deal And Personalization Upgrades Will Support Future Advertising Upside

Roku's updated analyst fair value estimate has shifted from $146.04 to $151.68. This reflects analysts' adjustments to discount rate, revenue growth, profit margin, and future P/E assumptions in light of Fox's planned acquisition and the recent wave of price target resets around the $155 to $160 range.

Analyst Commentary

Analysts are rapidly recalibrating their views on Roku after Fox announced plans to acquire the company in a cash and stock deal valued at US$160 per share. The research flow clusters around two themes, with bullish analysts focused on what the deal and Roku's existing partnerships could mean for long term growth and monetization, and more cautious analysts concentrating on deal caps, integration risk, and the odds of a higher competing bid.

Bullish Takeaways

- Bullish analysts who recently raised fair value or price targets toward the US$155 to US$160 area frame Roku as worth at least US$155 on a standalone basis. They suggest the Fox offer is broadly aligned with prior growth and margin expectations rather than solely a merger-driven bump.

- Commentary around Trade Desk's programmatic relationships with both Fox and Roku highlights the potential for stronger ad demand flows if the combined company keeps Roku's platform relatively open. This could support Roku's long term revenue mix and justify the US$22b acquisition price plus the cited US$8b debt load.

- Some bullish analysts view the US$160 headline price as reasonable and potentially beatable. They imply that competitive interest or improved Fox trading levels could support valuations near or above current deal terms if execution on integration and ad monetization stays on track.

- Positive remarks about Roku's Q1 beat and raise and its monetization trajectory indicate that, in the eyes of these analysts, the Fox transaction is layering a takeover premium on top of an already improving execution story rather than rescuing a weak business model.

Bearish Takeaways

- Bearish analysts who moved to Neutral, Hold, or similar ratings argue that Roku's stock is now largely trading on deal mechanics rather than fundamentals. In their view this limits near term upside relative to the US$160 offer and reduces the relevance of traditional growth and margin analysis.

- Several downgrades emphasize that the agreed US$160 per share effectively caps returns unless a competing bid emerges. At least one research house flags management commentary and disclosures as pointing to a low probability of a rival offer, which tempers expectations for further re-rating.

- Concerns around Fox's integration of Roku focus on higher leverage and the risk that overlapping services such as Fox's Tubi and the Roku platform could cannibalize each other if not carefully managed. This could weigh on the combined company's ability to fully realize the US$22b purchase plus incremental US$8b in debt.

- Some cautious commentary on Fox's own target cuts and references to platform conflict and integration risk underline that while Roku brings scale and living room reach, execution missteps at the parent could affect how much long term value is ultimately attributed to Roku's business within the combined structure.

What's in the News for Roku

- Fox Corporation agreed to acquire Roku in a cash and stock deal valued at approximately US$22b, or US$160 per share, with closing targeted for the first half of 2027. Fox describes the combined company as the third largest U.S. TV streaming player by share of viewing. (Source: Fox acquisition announcement)

- Roku reported Q1 2026 results that topped Wall Street expectations, with revenue growth of 22%, net income of US$85.7m, adjusted EBITDA growth of 165%, and global reach above 100m streaming households. The company also raised its full year 2026 revenue guidance to about US$5.5b. (Source: Q1 2026 earnings reports)

- Before the Fox deal was announced, Roku was reported to be reviewing multiple options, including a full company sale, PIPE financing, and deeper partnerships, while its stock price moved sharply on speculation around potential buyers. (Source: strategic alternatives reporting)

- Roku and Smartly announced an advertising partnership that connects Smartly directly into Roku Ads Manager via API, allowing marketers to extend social media campaigns to connected TV using existing workflows and creative assets. (Source: partnership announcement)

- Roku launched a major Home Screen redesign to over 100m households, adding more personalized content recommendations, new genre based destinations, and features such as Quick Access and expanded “Top Picks for You.” The company positions these changes as supporting both viewer engagement and partner exposure. (Source: product announcement)

Valuation Changes for Roku

- Fair Value: The analyst fair value estimate for Roku has risen slightly from $146.04 to $151.68 per share, bringing it closer to the US$160 deal price.

- Discount Rate: The discount rate has edged down slightly from 8.72% to about 8.68%, implying a modestly lower required return in analysts' models.

- Revenue Growth: The revenue growth assumption has moved slightly higher from 13.37% to about 13.39%, indicating a small upward adjustment to Roku's expected top line trajectory in analyst forecasts.

- Net Profit Margin: The net profit margin estimate has risen marginally from 11.54% to about 11.56%, reflecting a minor tweak to Roku's modeled profitability.

- Future P/E: The future P/E multiple has increased from 33.25x to about 34.44x, signaling a slightly higher valuation multiple being used in updated analyst work on Roku.

Key Takeaways

- Migration from linear TV to streaming and digital ads is driving user growth, platform engagement, and higher-margin advertising revenue.

- Investments in content, self-service ads, and operational efficiency are improving margins, financial health, and supporting long-term revenue and earnings expansion.

- Competition, ad market dependency, content fragmentation, data regulation, and risky international expansion all threaten Roku's ability to grow revenue, margins, and platform engagement.

Catalysts

About Roku- Operates a TV streaming platform in the United States and internationally.

- The accelerating shift away from traditional linear TV toward streaming continues to expand Roku's total addressable market, supporting long-term growth in active users and increasing demand for its connected TV platform, which is expected to drive sustained double-digit platform revenue growth.

- The global migration of advertising budgets from linear TV to digital and connected TV, combined with Roku's successful rollout of new ad products (such as Roku Ads Manager) and deeper third-party DSP integrations, increases its share of high-margin digital advertising, which is showing up as both revenue growth and higher platform margins.

- Increased penetration of smart TVs and streaming devices globally, along with investments in expanding Roku's operating system and international distribution, are fueling persistent user growth and engagement, laying the foundation for continued revenue expansion.

- Ongoing investments in proprietary content (e.g., The Roku Channel), self-service ad solutions, and performance marketing are boosting user engagement and attracting new cohorts of advertisers (especially SMBs), adding incremental high-margin advertising revenue and broadening usage, which are supporting margin and earnings growth.

- Enhanced operational discipline, margin expansion through operating leverage, and the company becoming operating income positive ahead of schedule signal improving financial health and suggest a potential for net margin and earnings acceleration as monetization initiatives scale.

Roku Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

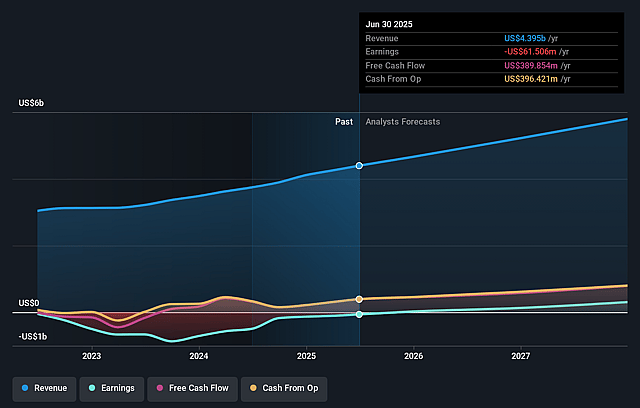

- Analysts are assuming Roku's revenue will grow by 13.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.1% today to 11.6% in 3 years time.

- Analysts expect earnings to reach $836.9 million (and earnings per share of $5.6) by about June 2029, up from $201.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.1 billion in earnings, and the most bearish expecting $575.0 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 34.5x on those 2029 earnings, down from 99.0x today. This future PE is greater than the current PE for the US Entertainment industry at 23.0x.

- Analysts expect the number of shares outstanding to grow by 0.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.68%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition in the smart TV OS and streaming device market from large ecosystem players (such as Amazon, Google, Apple, and now Walmart/Vizio) risks commoditizing Roku's hardware, which could limit household penetration growth, pressure device revenues, and erode Roku's ability to maintain current levels of active accounts-ultimately impacting both top-line revenue and long-term earnings capacity.

- Despite strong performance, Roku's heavy reliance on advertising revenue makes it vulnerable to macroeconomic slowdowns, cyclical ad market contractions, or shifting digital ad budgets toward competitors, resulting in potential revenue volatility and compressing operating or net margins during periods of weaker ad demand.

- The proliferation of direct-to-consumer apps and continued content fragmentation may see major media companies withholding top-tier content or creating more walled gardens, diminishing Roku's platform value proposition, reducing user engagement/time spent, and limiting subscription or ad revenue potential.

- Increasing global privacy regulations and consumer data protection laws may restrict Roku's ability to leverage its proprietary data for targeted advertising, potentially stalling growth in its high-margin ad business and impacting long-term profitability.

- International expansion and new market entry, including performance-focused ad products for SMBs, carry significant execution and scaling risks; initial investments may not generate proportionate returns, which could keep net margins compressed or delay improvements in long-term operating income and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $151.68 for Roku based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $170.0, and the most bearish reporting a price target of just $103.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $7.2 billion, earnings will come to $836.9 million, and it would be trading on a PE ratio of 34.5x, assuming you use a discount rate of 8.7%.

- Given the current share price of $135.06, the analyst price target of $151.68 is 11.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Roku?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.