Last Update 27 Jul 26

Fair value Increased 2.50%APH: AI Data Center Buildout And CommScope Deal Will Drive Upside

Amphenol's analyst fair value estimate has been nudged higher from about $184.78 to $189.39. This reflects a series of recent price target increases across the Street as analysts factor in Q2 earnings previews, confidence in networking infrastructure and storage components, ongoing focus on AI related demand, and sector recovery expectations.

Analyst Commentary

Recent research on Amphenol points to a cluster of higher price targets around the Q2 earnings preview period, with analysts weighing the company’s exposure to networking infrastructure, storage components, and AI related demand against pockets of risk in execution and positioning.

Bullish Takeaways

- Bullish analysts see Amphenol well positioned into Q2 results, with expectations that Street forecasts could reset higher after the print, which supports a higher fair value framework.

- Several price target increases are tied to constructive views on networking infrastructure and storage components, suggesting confidence in Amphenol’s role across data and connectivity spending.

- Some research points to increased confidence around AI related content, which is being incorporated into updated estimates and valuation work.

- Recent target moves in the electronic components and industrial technology groups indicate that, within these sectors, Amphenol is viewed as one of the better positioned companies on growth and execution.

Bearish Takeaways

- JPMorgan removed Amphenol from its Equity Focus List, which signals a more balanced stance even while keeping an Overweight rating and can temper how aggressively some investors might underwrite upside.

- BofA commentary highlights investor focus on the durability of AI related growth, the trade off between copper and optical solutions, and potential share risks, all of which could limit how much investors are willing to pay for the stock.

- Despite higher price targets, some research keeps more neutral ratings in place, indicating that, at current levels, valuation already reflects a meaningful portion of the Street’s growth and execution expectations.

- References to the sector being in the early stages of recovery make clear that macro and industry normalization are still works in progress, which could introduce variability in near term results and sentiment around Amphenol.

What’s in the News for Amphenol

- Amphenol agreed to acquire CommScope's Connectivity and Cable Solutions business for US$10.5b, expanding fiber optic capabilities and positioning the company as a broader connectivity supplier across AI data centers, networking, and storage. (Source: Amphenol Strengthens AI Data Center Leadership with CommScope Acquisition and Robust Growth)

- The company reported record first quarter 2026 sales with a US$9.4b order backlog and wider operating margins tied to demand across IT datacom, defense, aerospace, automotive, and industrial markets. (Source: Amphenol Strengthens AI Data Center Leadership with CommScope Acquisition and Robust Growth)

- Amphenol issued guidance for second quarter 2026 sales of US$8.1b to US$8.2b, which the company indicates would be 43% to 45% above the prior year quarter, with expected diluted EPS (GAAP) of US$1.13 to US$1.15. (Source: Corporate guidance)

- From 1 January 2026 to 29 April 2026, Amphenol repurchased 1,574,534 shares for US$222.23m, completing a broader buyback of 15,927,704 shares for US$1,351.11m under its April 24, 2024 authorization. (Source: Buyback tranche update)

- Amphenol joined a multi company group including 3M, AMD, Arista Networks, Cisco, Meta, TE Connectivity, and others to develop open specifications for expanded beam optical connectors aimed at AI data center deployments. (Source: Strategic alliances)

Valuation Changes for Amphenol

- Fair Value: The analyst fair value estimate for Amphenol has risen slightly from $184.78 to $189.39, reflecting a modest upward adjustment in the model.

- Discount Rate: The discount rate has edged lower from 8.97% to 8.95%, indicating a small change in the risk assumptions applied to future cash flows.

- Revenue Growth: Forecast revenue growth has risen slightly from 19.04% to 19.42%, pointing to a marginally higher growth outlook being used in the valuation inputs.

- Net Profit Margin: The projected profit margin has eased from 20.66% to 20.46%, suggesting a slightly more conservative view on future profitability for Amphenol.

- Future P/E: The future P/E assumption has increased from 33.32x to 34.13x, indicating a small uplift in the multiple used to value Amphenol’s earnings stream.

Key Takeaways

- Robust demand for high-speed interconnect solutions and diversified end markets strengthens revenue durability and reduces risk from economic cycles.

- Strategic acquisitions, innovation, and a premium product mix are enhancing margins, pricing power, and positioning versus competitors for secular growth.

- Heavy reliance on volatile tech markets, high capex, acquisition risks, and competitive pricing pressures threaten sustainable growth, margin stability, and free cash flow.

Catalysts

About Amphenol- Designs, manufactures, and markets electrical, electronic, and fiber optic connectors in the United States, China, and internationally.

- Accelerating global deployment of AI-driven data centers and adoption of next-generation IT architecture is driving strong, sustained demand for Amphenol's high-speed, high-value interconnect solutions, as evidenced by exceptional growth in IT datacom revenue and continued multi-quarter customer engagement; this is expected to support further top-line growth and maintain higher incremental margins.

- Increased electronic content and complexity across automotive, industrial, defense, and communications markets (including EVs, factory automation, and defense modernization) is expanding Amphenol's total addressable market, enabling diversified, resilient revenue streams and reducing cyclicality risk, which should underpin durability in both sales and earnings.

- Ongoing strategic acquisitions (e.g., ANDREW, CIT, Narda-MITEQ) are broadening product offerings in attractive, high-growth segments (AI, RF/microwave, aerospace/defense), creating further operating leverage and margin expansion opportunities through integration, as reflected in recent record operating margins and sequential improvement in profitability.

- Enhanced focus on high-technology, differentiated product mix-driven by customer demand for mission-critical, high-performance components-has strengthened pricing power and operating efficiency, resulting in structurally higher conversion and operating margins, with management now targeting 30% incremental margin conversion versus the historical 25%.

- Sustained investment in capacity and innovation (elevated CapEx to support datacom/AI growth, R&D for advanced connectors), paired with global supply chain agility and geographic diversification, positions Amphenol to out-execute competitors in capturing future secular growth, supporting robust free cash flow and long-term earnings per share growth.

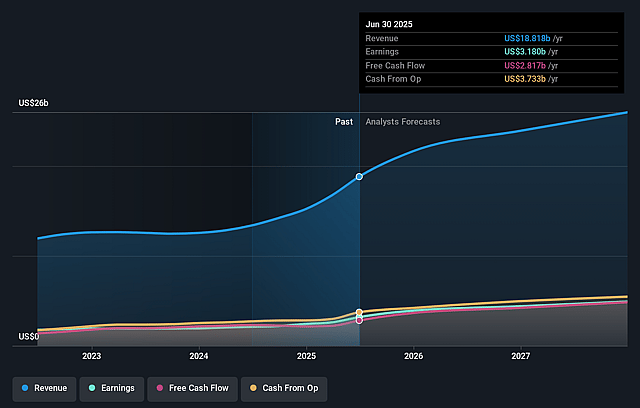

Amphenol Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Amphenol's revenue will grow by 19.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 17.2% today to 20.5% in 3 years time.

- Analysts expect earnings to reach $9.0 billion (and earnings per share of $7.04) by about July 2029, up from $4.5 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $10.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 34.1x on those 2029 earnings, down from 42.1x today. This future PE is greater than the current PE for the US Electronic industry at 29.6x.

- Analysts expect the number of shares outstanding to grow by 0.76% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.95%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's unprecedented growth and robust results in the IT datacom and AI infrastructure markets may not be sustainable as sector demand can be volatile and "lumpy"-management specifically acknowledged recent outperformance involved "pulling forward" demand from future quarters, which could lead to short-term revenue declines or stagnation if customer investment moderates.

- Ongoing elevated capital expenditures, especially in support of the booming AI and datacenter demand, could pressure future free cash flow and operating margins if the anticipated growth doesn't persist or if project returns underperform expectations.

- The aggregate contribution to revenue growth from acquisitions is significant, and the text notes "the dilutive impact of acquisitions," as well as the risk that future deals may be less synergistic or harder to integrate, potentially reducing overall net margin improvement.

- Although management highlighted a diversified customer and market base, the results reveal growing exposure to cyclical and fast-evolving technology end markets (notably AI/data center infrastructure), which increases risk of customer concentration and unpredictable revenue/earnings swings as technology cycles or customer budgets shift.

- Intense focus on expanding sales in high-performance, high-margin segments creates challenges to sustain pricing power amid long-term industry trends toward commoditization and system integration, meaning downward pricing pressure or shifts in product mix could erode long-term revenue growth and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $189.39 for Amphenol based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $215.0, and the most bearish reporting a price target of just $165.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $44.1 billion, earnings will come to $9.0 billion, and it would be trading on a PE ratio of 34.1x, assuming you use a discount rate of 8.9%.

- Given the current share price of $152.67, the analyst price target of $189.39 is 19.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Amphenol?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.