Key Takeaways

- Strategic investments and expansion in global markets and omni-channel development are expected to drive revenue growth and enhance consumer engagement.

- Emphasis on IP-centric and higher-value products is likely to improve profit margins and strengthen partnerships with major licensors.

- The reliance on directly operated stores in overseas markets and geopolitical risks could significantly pressure operational costs and profit margins.

Catalysts

About MINISO Group Holding- An investment holding company, engages in the retail and wholesale of lifestyle products and pop toy products in China, rest of Asia, the Americas, Europe, Indonesia, and internationally.

- The acquisition of a 29.4% stake in Yonghui and plans to optimize its operations could result in improved revenue and net margins due to synergies in supply chain integration and operational efficiencies.

- MINISO's commitment to expanding its store network, adding 900 to 1,100 new stores globally each year, is expected to drive revenue growth through increased market presence.

- The focus on IP-centric products, which are anticipated to contribute over 50% of sales by 2028, is likely to boost gross profit margins due to higher-value product offerings and exclusive collaborations with major IP licensors.

- The expansion and optimization efforts in overseas markets, particularly in high-growth areas like the U.S. and Europe, present opportunities for significant revenue and earnings growth driven by improved store operations and increased consumer stickiness.

- Strategic investment in omni-channel and O2O (online-to-offline) business development is expected to enhance consumer engagement and sales efficiency, contributing positively to same-store sales growth and overall earnings.

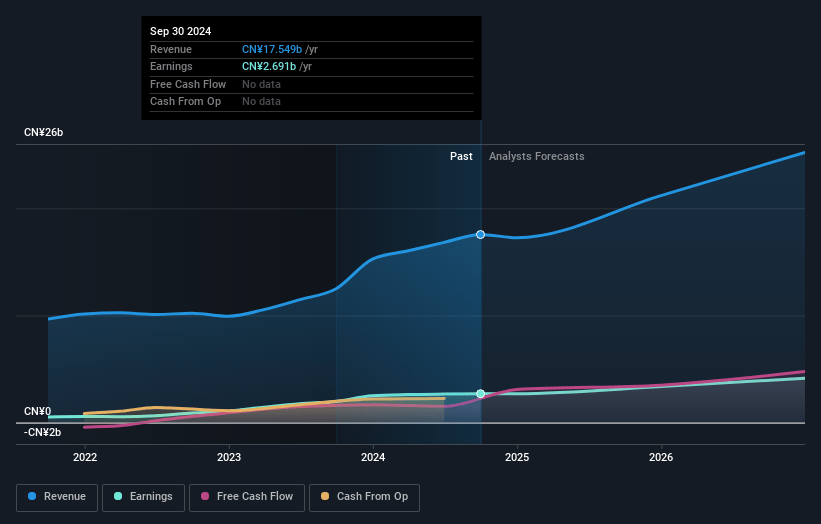

MINISO Group Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming MINISO Group Holding's revenue will grow by 17.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.3% today to 16.7% in 3 years time.

- Analysts expect earnings to reach CN¥4.7 billion (and earnings per share of CN¥15.09) by about January 2028, up from CN¥2.7 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.2x on those 2028 earnings, down from 19.3x today. This future PE is lower than the current PE for the US Multiline Retail industry at 19.3x.

- Analysts expect the number of shares outstanding to grow by 0.69% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.72%, as per the Simply Wall St company report.

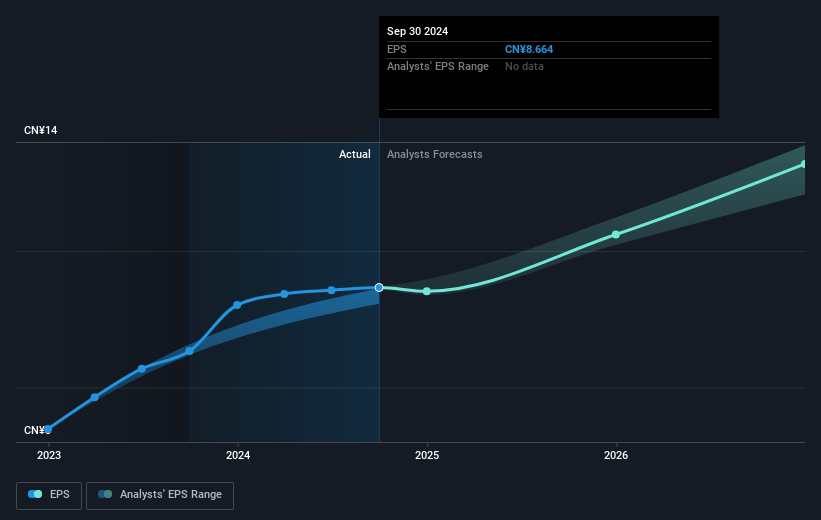

MINISO Group Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's reliance on directly operated stores in overseas markets could lead to higher operational expenses, such as rent, labor, and logistics costs, impacting net margins.

- Same-store sales performance, especially in lower-tier cities in China, showed a mid-single-digit decline, indicating potential revenue growth challenges.

- The geopolitical risks and potential U.S. tariff increases pose a threat to supply chain costs and could affect the company's pricing power and profit margins.

- The acquisition of Yonghui, while expanding brand reach, introduces integration risks and potential financial liabilities, impacting cash flows and earnings.

- Intense competition in the IP-centric consumer goods market may pressure MINISO's market positioning, affecting revenue growth and margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $25.42 for MINISO Group Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $32.39, and the most bearish reporting a price target of just $14.71.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥28.4 billion, earnings will come to CN¥4.7 billion, and it would be trading on a PE ratio of 15.2x, assuming you use a discount rate of 7.7%.

- Given the current share price of $23.26, the analyst's price target of $25.42 is 8.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

SU

SuEric

Community Contributor

Top Pick for Multi-bagger

Strong Q1 2024 Performance In Q1 2024, $MNSO revenue surged 26% year-on-year to $515.7 million, with adjusted EBITDA margin expanding by 200 basis points to 25.9%. This growth was fueled by a robust strategy of opening new stores globally.

View narrativeUS$44.06

FV

55.8% undervalued intrinsic discount20.00%

Revenue growth p.a.

9users have liked this narrative

0users have commented on this narrative

22users have followed this narrative

about 2 months ago author updated this narrative