Catalysts

About Insight Molecular Diagnostics

Insight Molecular Diagnostics develops and commercializes molecular diagnostic assays for transplant rejection monitoring, with a current focus on its GraftAssure franchise and related lab services.

What are the underlying business or industry changes driving this perspective?

- The company is heavily dependent on timely FDA authorization of GraftAssureDx. Any prolonged government funding disruptions or extended review cycles could delay kit commercialization and keep revenue concentrated in lower scale lab services, which would weigh on revenue growth and delay any improvement in earnings.

- Clinicians are accustomed to existing centralized lab tests for donor derived cell free DNA. If head to head studies and registry data are slower to convert early adopters into broad center wide use, kit volumes could ramp more slowly while commercial expenses rise, compressing net margins.

- The business model relies on transplant centers bringing testing in house. If hospitals struggle with staffing, capital budgets or internal validation priorities, some may prefer to continue send out testing, which would limit kit penetration and keep overall revenue below the level implied by the stated 3 million annual testing opportunities.

- The projected total addressable market assumes at least 2 tests per year per patient and eventual expansion across kidney, heart, lung and other organs. If payers hold to restrictive coverage policies or limit reimbursement for additional tests, actual test utilization could remain below these assumptions, capping revenue and constraining operating margin expansion.

- The plan to extend the GraftAssure franchise into oncology and broader cancer testing adds complexity and capital needs. If resources are stretched between transplant and oncology before the core transplant franchise reaches scale, fixed costs could grow faster than kit and lab revenue, delaying any path to positive adjusted EBITDA and net income.

Assumptions

This narrative explores a more pessimistic perspective on Insight Molecular Diagnostics compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming Insight Molecular Diagnostics's revenue will grow by 47.1% annually over the next 3 years.

- The bearish analysts are not forecasting that Insight Molecular Diagnostics will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Insight Molecular Diagnostics's profit margin will increase from -1380.7% to the average US Biotechs industry of 16.2% in 3 years.

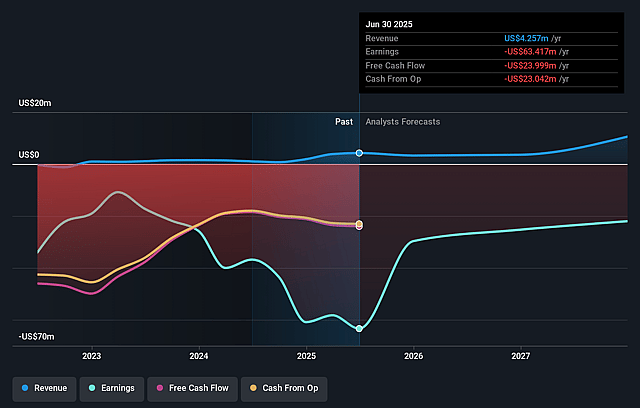

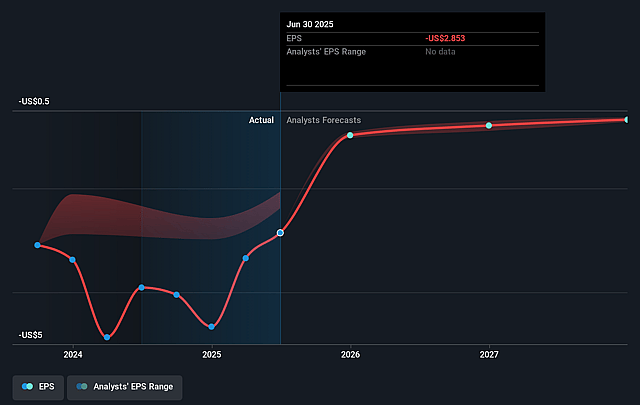

- If Insight Molecular Diagnostics's profit margin were to converge on the industry average, you could expect earnings to reach $2.3 million (and earnings per share of $0.08) by about January 2029, up from $-60.8 million today.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 62.2x on those 2029 earnings, up from -3.5x today. This future PE is greater than the current PE for the US Biotechs industry at 22.0x.

- The bearish analysts expect the number of shares outstanding to grow by 0.23% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.04%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Management is targeting FDA submission for GraftAssureDx by the end of 2025 and is preparing for a potential mid 2026 launch. The company reports that its assay performance in multi center pilots has exceeded expectations and that its Nashville CLIA lab is already processing reimbursed tests, which, if successful, could support kit revenue growth and improve earnings and net margins over time.

- The company highlights a kitted transplant testing TAM of more than US$1b, built on an estimated 1.5 million patients under management and 3 million testing opportunities per year. It points to growing transplant volumes and guideline adoption as tailwinds, which could underpin long term revenue growth and support operating margin expansion.

- Clinician feedback on the combination model score and higher positive predictive value for biopsies has been very positive according to management. Ongoing head to head and registry studies could help GraftAssure become embedded in clinical practice, which may lift test utilization and support higher gross profit and eventually improved net income.

- The company reports that it ended the quarter with US$20 million in cash and equivalents and no debt, is keeping cash burn near US$6 million per quarter, and has flexibility to scale back certain expenses. These factors could reduce financing risk and support the path toward better adjusted EBITDA and non GAAP net income over time.

- Management describes strong engagement from leading transplant centers, supportive relationships with partners such as Bio Rad, and a highly concentrated customer base of roughly 100 major transplant centers. If converted and retained over many years, these relationships could provide recurring revenue and help support more stable earnings and operating margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Insight Molecular Diagnostics is $4.0, which represents up to two standard deviations below the consensus price target of $7.0. This valuation is based on what can be assumed as the expectations of Insight Molecular Diagnostics's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $9.0, and the most bearish reporting a price target of just $4.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $14.0 million, earnings will come to $2.3 million, and it would be trading on a PE ratio of 62.2x, assuming you use a discount rate of 7.0%.

- Given the current share price of $7.5, the analyst price target of $4.0 is 87.5% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Insight Molecular Diagnostics?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.