Last Update 19 Dec 25

Fair value Increased 4.15%ROKU: Platform Monetization And Profitability Efforts Will Support Measured Upside Into 2026

Analysts have nudged their fair value estimate for Roku higher, from approximately $111 to $115. They cite slightly stronger revenue growth expectations into 2026 and increasing confidence that platform investments will support premium future multiples despite some compression in projected profit margins.

Analyst Commentary

Recent Street research on Roku reflects a generally constructive stance, with multiple firms raising price targets alongside improving confidence in the company’s execution into 2026.

Bullish Takeaways

- Bullish analysts highlight that Q3 results were solid, with revenue and Q4 guidance at or slightly ahead of expectations, reinforcing confidence in Roku’s ability to deliver against its growth plan.

- Platform investments in advertising and new services are increasingly viewed as key drivers of incremental monetization, supporting the case for sustained top line expansion and a higher fair value range.

- Improving platform fundamentals and a clearer path to positive and growing EBITDA are seen as validating management’s strategic spend, helping justify premium valuation multiples versus historical levels.

- Some major firms, including JPMorgan, argue that the Q4 outlook keeps the 2026 bull case intact, underpinning upward revisions to price targets and a tilt toward more constructive ratings.

Bearish Takeaways

- Bearish analysts remain cautious on the pace of profit margin expansion, noting that continued investment in the platform could limit near term leverage and cap upside to earnings based valuation frameworks.

- Neutral views and In Line ratings emphasize that while fundamentals are improving, the recent share price strength may already discount a sizable portion of the medium term growth story.

- Some observers point out that Q3 upside was more modest than in prior quarters, suggesting that execution needs to remain tight for Roku to fully deliver against elevated 2026 expectations.

What's in the News

- Paramount appoints Roku ad sales leader Jay Askinasi as its new chief revenue officer, signaling industry recognition of Roku's advertising leadership talent and potentially creating a key partnership conduit between the companies (ADWEEK).

- Roku and DoubleVerify mark major milestones in their multiyear collaboration to combat CTV ad fraud, blocking billions of fraudulent ad requests imitating Roku device traffic and showcasing the impact of Roku's Advertising Watermark technology.

- Roku and FreeWheel significantly expand their partnership, making FreeWheel's Streaming Hub a central activation platform for Roku Advertising and giving buyers and publishers more direct, transparent access to Roku's premium CTV inventory.

- Roku launches Philips Roku TV sets featuring Philips Ambilight technology in the U.S., extending its TV OS footprint with an immersive lighting experience, 4K HDR support, and deeper integration into the Roku ecosystem.

- Roku completes a $50 million share repurchase, buying back 567,582 shares, or 0.39 percent of shares outstanding, under the buyback program announced in July 2025.

Valuation Changes

- Fair Value Estimate has risen slightly, increasing from approximately $111 to about $115.50 per share, reflecting modestly stronger growth assumptions.

- Discount Rate has edged down marginally from about 9.07 percent to roughly 9.06 percent, implying a slightly lower required return on Roku’s equity.

- Revenue Growth has risen slightly, with the medium term outlook moving from roughly 11.8 percent to about 12.0 percent, supporting a higher intrinsic valuation.

- Net Profit Margin has fallen moderately, declining from around 5.9 percent to about 5.1 percent as higher platform investment is incorporated into the model.

- Future P/E multiple has increased meaningfully, moving from about 58.7x to roughly 69.8x and signaling a higher expected premium for Roku’s long term earnings potential.

Key Takeaways

- Migration from linear TV to streaming and digital ads is driving user growth, platform engagement, and higher-margin advertising revenue.

- Investments in content, self-service ads, and operational efficiency are improving margins, financial health, and supporting long-term revenue and earnings expansion.

- Competition, ad market dependency, content fragmentation, data regulation, and risky international expansion all threaten Roku's ability to grow revenue, margins, and platform engagement.

Catalysts

About Roku- Operates a TV streaming platform in the United States and internationally.

- The accelerating shift away from traditional linear TV toward streaming continues to expand Roku's total addressable market, supporting long-term growth in active users and increasing demand for its connected TV platform, which is expected to drive sustained double-digit platform revenue growth.

- The global migration of advertising budgets from linear TV to digital and connected TV, combined with Roku's successful rollout of new ad products (such as Roku Ads Manager) and deeper third-party DSP integrations, increases its share of high-margin digital advertising, which is showing up as both revenue growth and higher platform margins.

- Increased penetration of smart TVs and streaming devices globally, along with investments in expanding Roku's operating system and international distribution, are fueling persistent user growth and engagement, laying the foundation for continued revenue expansion.

- Ongoing investments in proprietary content (e.g., The Roku Channel), self-service ad solutions, and performance marketing are boosting user engagement and attracting new cohorts of advertisers (especially SMBs), adding incremental high-margin advertising revenue and broadening usage, which are supporting margin and earnings growth.

- Enhanced operational discipline, margin expansion through operating leverage, and the company becoming operating income positive ahead of schedule signal improving financial health and suggest a potential for net margin and earnings acceleration as monetization initiatives scale.

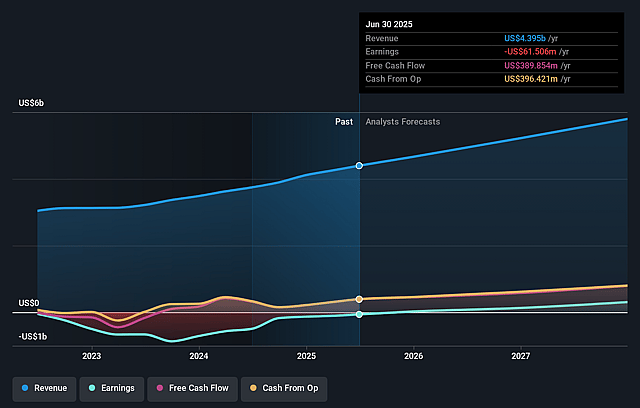

Roku Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Roku's revenue will grow by 11.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from -1.4% today to 6.1% in 3 years time.

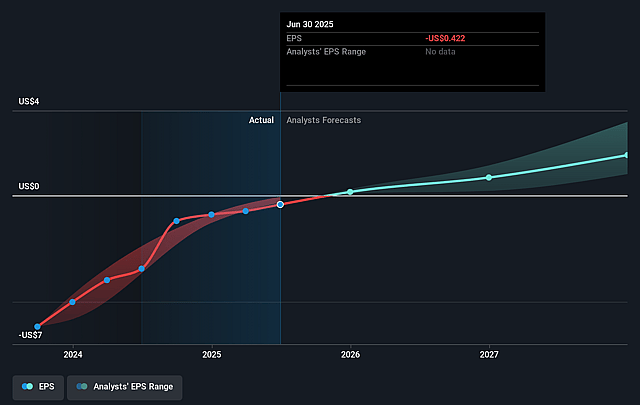

- Analysts expect earnings to reach $372.1 million (and earnings per share of $2.25) by about September 2028, up from $-61.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $513.6 million in earnings, and the most bearish expecting $149.3 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 53.9x on those 2028 earnings, up from -235.9x today. This future PE is greater than the current PE for the US Entertainment industry at 38.2x.

- Analysts expect the number of shares outstanding to grow by 1.47% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.05%, as per the Simply Wall St company report.

Roku Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intensifying competition in the smart TV OS and streaming device market from large ecosystem players (such as Amazon, Google, Apple, and now Walmart/Vizio) risks commoditizing Roku's hardware, which could limit household penetration growth, pressure device revenues, and erode Roku's ability to maintain current levels of active accounts-ultimately impacting both top-line revenue and long-term earnings capacity.

- Despite strong performance, Roku's heavy reliance on advertising revenue makes it vulnerable to macroeconomic slowdowns, cyclical ad market contractions, or shifting digital ad budgets toward competitors, resulting in potential revenue volatility and compressing operating or net margins during periods of weaker ad demand.

- The proliferation of direct-to-consumer apps and continued content fragmentation may see major media companies withholding top-tier content or creating more walled gardens, diminishing Roku's platform value proposition, reducing user engagement/time spent, and limiting subscription or ad revenue potential.

- Increasing global privacy regulations and consumer data protection laws may restrict Roku's ability to leverage its proprietary data for targeted advertising, potentially stalling growth in its high-margin ad business and impacting long-term profitability.

- International expansion and new market entry, including performance-focused ad products for SMBs, carry significant execution and scaling risks; initial investments may not generate proportionate returns, which could keep net margins compressed or delay improvements in long-term operating income and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $101.154 for Roku based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $130.0, and the most bearish reporting a price target of just $70.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $6.1 billion, earnings will come to $372.1 million, and it would be trading on a PE ratio of 53.9x, assuming you use a discount rate of 9.0%.

- Given the current share price of $98.47, the analyst price target of $101.15 is 2.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Roku?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.