Key Takeaways

- Strategic expansion of the Las Vegas Grand Prix and dynamic pricing strategies may initially fall short but aim to boost revenue.

- Enhanced U.S. marketing and premium F1 TV subscriptions aim to increase media revenue and audience engagement, supporting earnings growth.

- Financial underperformance at the Las Vegas Grand Prix and high dependency on sponsorships pose risks to revenue, compounded by regulatory scrutiny and potential operational cost increases.

Catalysts

About Formula One Group- Engages in the motorsports business in the United States and the United Kingdom.

- Formula One Group is focusing on expanding its Las Vegas Grand Prix to improve top and bottom-line performance by leveraging data analytics for ticket pricing and product strategies, which may lead to better revenue outcomes, especially initially falling short of projections.

- Enhancements in hospitality and new marketing strategies, especially in the U.S. market, could potentially raise the average revenue per race despite previous underperformance in some offerings.

- Growing global fan base and launching new premium F1 TV subscriptions are aimed at driving up media rights revenue and maximizing audience engagement, likely contributing to earnings growth over time.

- The integration and collaboration with regional and global sponsors, including new high-value partnerships, could boost sponsorship revenue, which was up 10% in 2024, continuing to build this revenue stream.

- Strategies to improve operational efficiencies in freight logistics and capitalize on the regionalization of the race calendar may provide a positive impact on net margins by reducing the cost of operations.

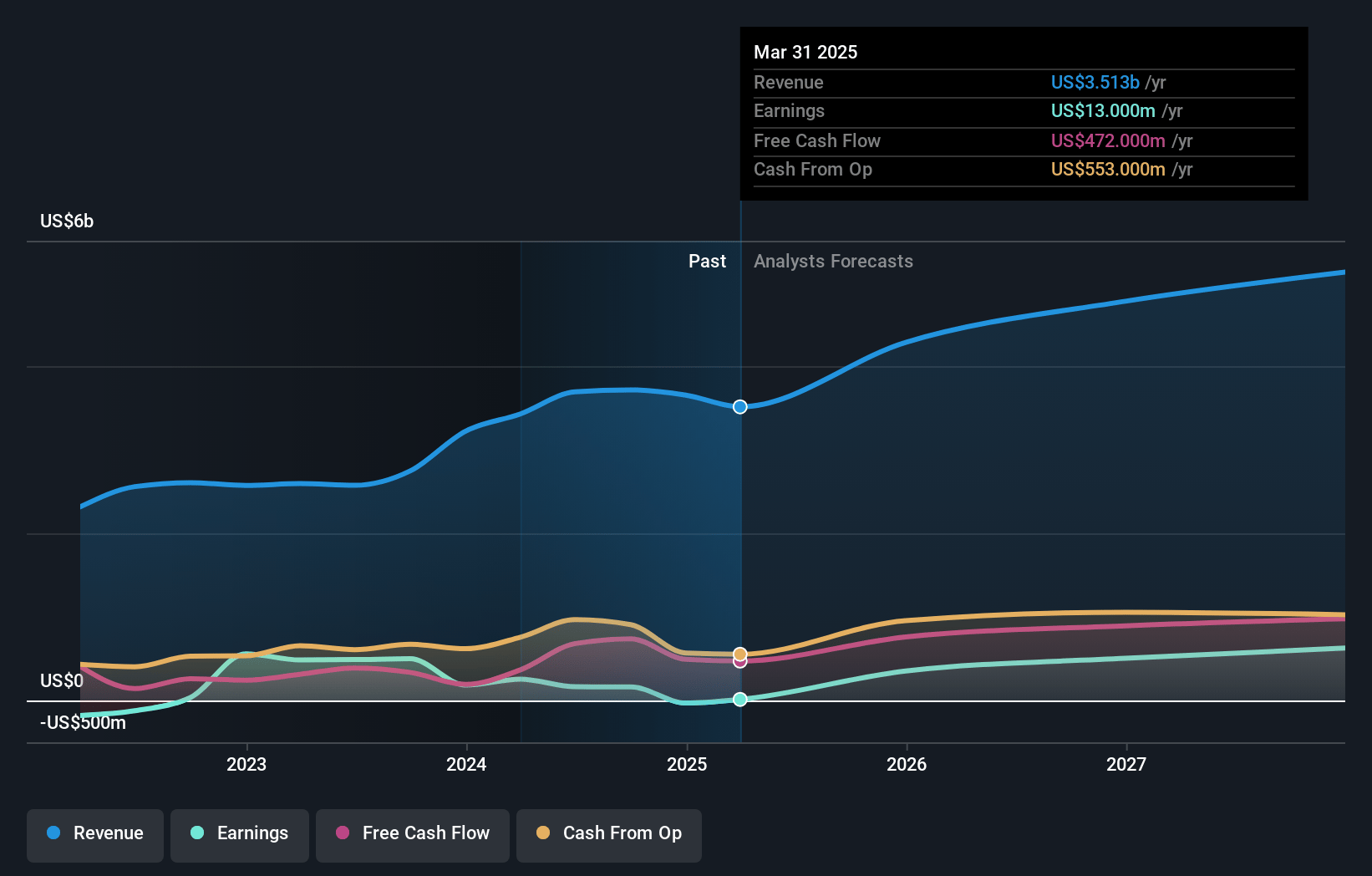

Formula One Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Formula One Group compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Formula One Group's revenue will grow by 5.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -0.8% today to 9.5% in 3 years time.

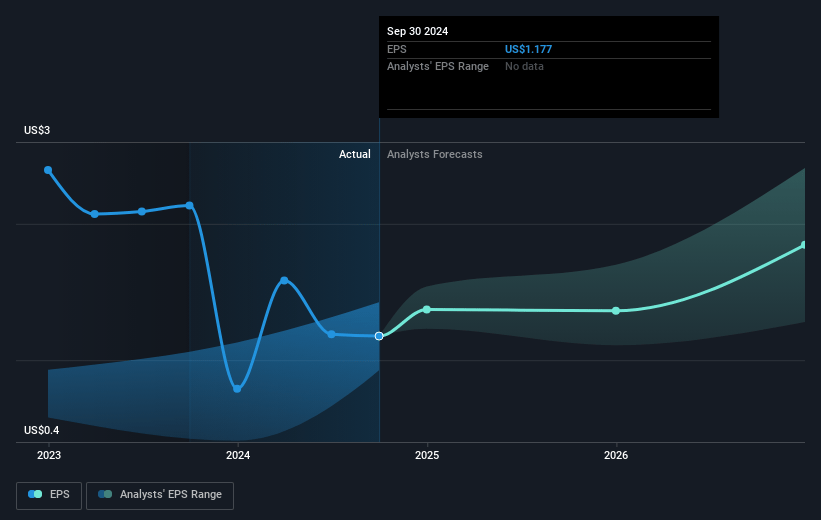

- The bearish analysts expect earnings to reach $408.6 million (and earnings per share of $2.12) by about April 2028, up from $-30.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 84.4x on those 2028 earnings, up from -719.4x today. This future PE is greater than the current PE for the US Entertainment industry at 21.8x.

- Analysts expect the number of shares outstanding to grow by 6.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.58%, as per the Simply Wall St company report.

Formula One Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The Las Vegas Grand Prix underperformed financially, particularly in terms of ticket sales and hospitality offerings, resulting in missed revenue and OIBDA expectations for 2024. This could impact future earnings if improvements are not realized.

- Formula One is facing regulatory scrutiny, with the Phase 2 regulatory process for the Dorna acquisition indicating potential complexity and delays, which could affect future financial operations and integration costs.

- There's a risk of fluctuating revenues due to changes in the race calendar and the high dependency on contracted revenues, which might limit growth opportunities in media rights and sponsorship revenue streams.

- The cost management issues highlighted by the need for structural reorganization in Las Vegas suggest a risk of increased operational costs, which could compress net margins if not managed effectively.

- Dependency on sponsorships is high, and while there is strong demand, any weakening in this area or failure to replace existing deals could affect revenue streams significantly, especially if expectations for top-line improvements from events like the Las Vegas Grand Prix are not realized.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Formula One Group is $90.68, which represents one standard deviation below the consensus price target of $104.56. This valuation is based on what can be assumed as the expectations of Formula One Group's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $125.0, and the most bearish reporting a price target of just $80.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $4.3 billion, earnings will come to $408.6 million, and it would be trading on a PE ratio of 84.4x, assuming you use a discount rate of 8.6%.

- Given the current share price of $86.59, the bearish analyst price target of $90.68 is 4.5% higher. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:FWON.K. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.