Key Takeaways

- Anticipated approvals, expansions, and rebranding may boost revenue and market reach, driving future growth in media and sponsorship sectors.

- Strategic organizational changes and regionalization efforts aim to enhance financial results, improve cost efficiency, and increase net margins.

- Challenges in race-specific performance, media negotiations, regulatory processes, and new team dynamics pose risks to revenue growth and market engagement success.

Catalysts

About Formula One Group- Through its subsidiary Formula 1, engages in the motorsports business in the United States and internationally.

- The anticipated approval of the Dorna acquisition and the expansion of the MotoGP calendar to 22 races, along with rebranding efforts, are expected to boost revenue and expand cultural relevance, potentially increasing Formula One Group's market reach and revenue streams.

- The organizational restructuring of the Las Vegas Grand Prix and strategic changes in ticketing and cost management are projected to improve financial results for the event, enhancing revenue and net margins in 2025.

- The launch of a new premium tier for F1 TV offering high-definition content and multi-device capability aims to capture avid fans, which could drive subscriber growth and increase earnings from the media rights segment.

- The signing of new high-profile sponsorship deals, including partnerships with LVMH, Pirelli, and Crypto.com, is expected to drive significant revenue growth in 2025 and provide momentum for future sponsorship opportunities, impacting revenue positively.

- Efforts to regionalize the F1 calendar to support net-zero goals and improve freight logistics efficiency could result in cost savings, potentially enhancing net margins and earnings in the long term.

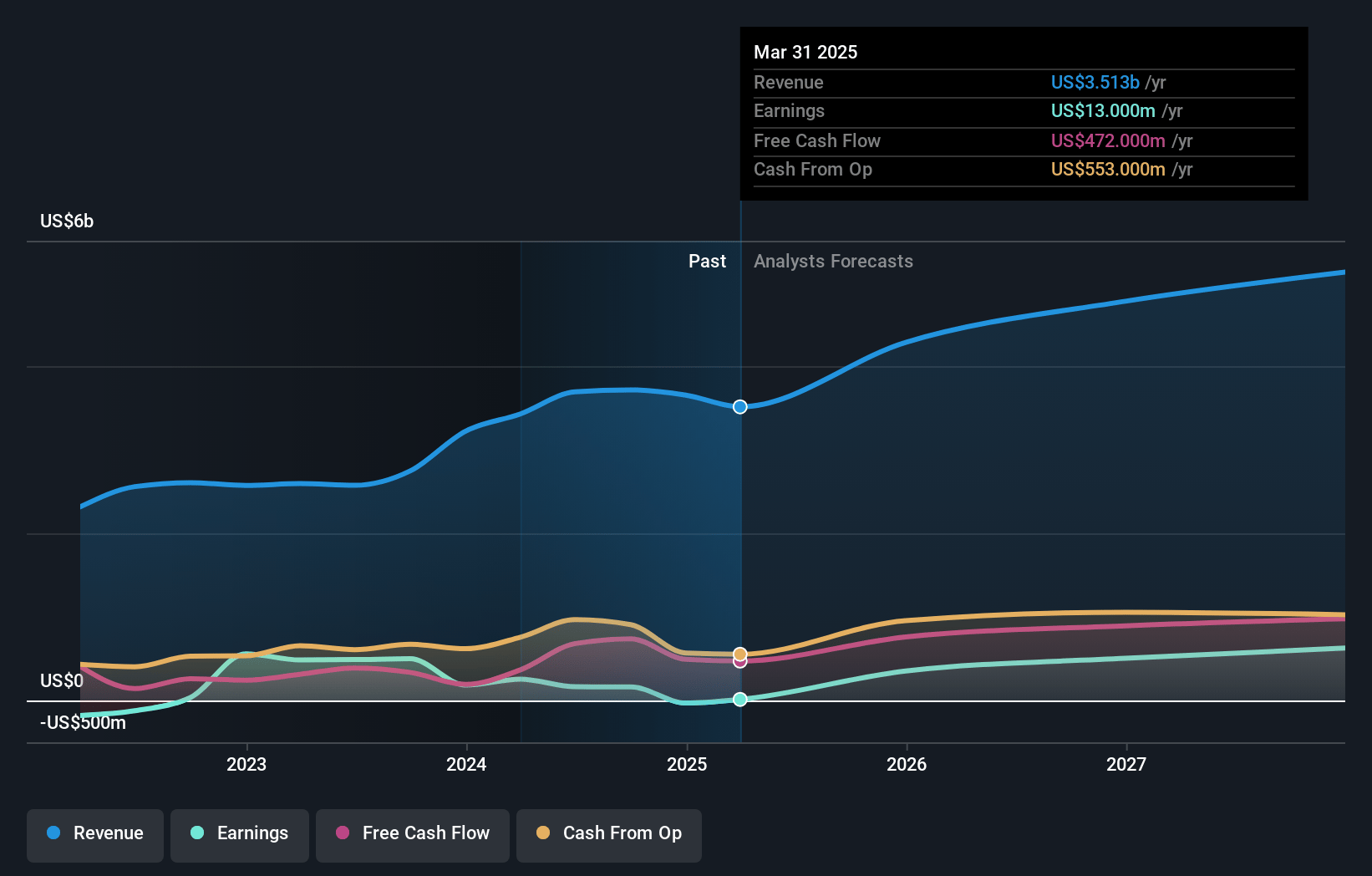

Formula One Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Formula One Group's revenue will grow by 9.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.8% today to 12.8% in 3 years time.

- Analysts expect earnings to reach $608.6 million (and earnings per share of $2.38) by about May 2028, up from $-30.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $814.8 million in earnings, and the most bearish expecting $428.0 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 65.9x on those 2028 earnings, up from -759.2x today. This future PE is greater than the current PE for the US Entertainment industry at 22.4x.

- Analysts expect the number of shares outstanding to grow by 6.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.63%, as per the Simply Wall St company report.

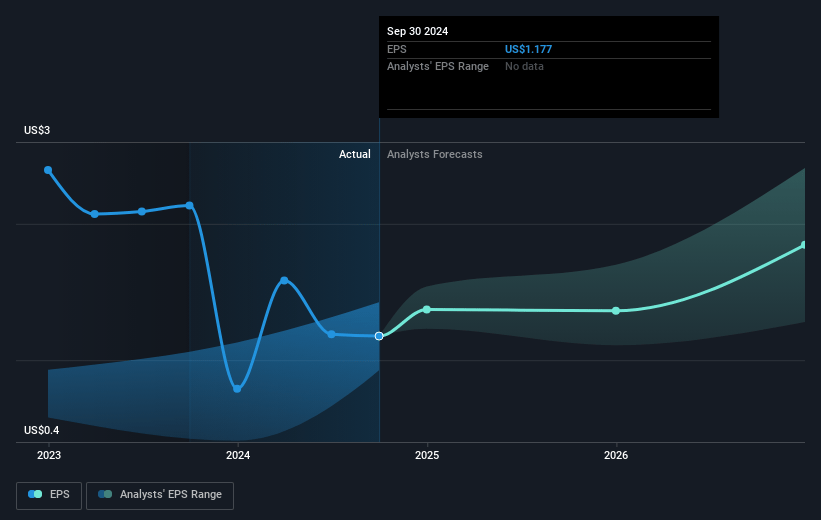

Formula One Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The Las Vegas Grand Prix did not meet internal expectations on revenue and OIBDA, which suggests potential volatility in race-specific financial performance and can impact future margins if not rectified.

- Media rights negotiations, particularly with ESPN, reveal competitive tension and dependency on reaching deals that balance monetization and viewership reach; failure to secure favorable terms could affect revenue growth.

- The ongoing regulatory process for the Dorna acquisition represents a risk of delays or complications, impacting projected timelines and associated revenue from this transaction.

- The entry of a new team, GM Cadillac, raises questions regarding team payment allocations under the Concorde Agreement, potentially affecting the financial dynamics within Formula One’s current revenue sharing model.

- While expanding into new geographical race promotions, such as adding tracks in Hungary and the Czech Republic, there is inherent execution risk; failure to capture anticipated market engagement could impact overall revenue projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $105.365 for Formula One Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $125.0, and the most bearish reporting a price target of just $80.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $4.7 billion, earnings will come to $608.6 million, and it would be trading on a PE ratio of 65.9x, assuming you use a discount rate of 8.6%.

- Given the current share price of $91.37, the analyst price target of $105.37 is 13.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.