Last Update01 May 25Fair value Decreased 6.06%

Key Takeaways

- Focused strategy on user engagement and safety features aims to enhance user retention, boosting conversion rates and revenue growth.

- Streamlining resources towards core offerings and optimizing monetization strategies supports operational efficiency and improved earnings potential.

- Efforts to improve ecosystem health and strategic pivoting may hinder short-term revenue and earnings, with falling user metrics compounding margin pressures.

Catalysts

About Bumble- Provides online dating and social networking applications in North America, Europe, internationally.

- Bumble is implementing a focused strategy to optimize user engagement and attract the right kind of users, which is expected to enhance the quality of matches and increase user satisfaction, potentially boosting conversion rates and future revenue growth.

- The significant investment in safety and trust features, such as ID verification and AI-assisted tools, aims to improve the user experience and increase user retention, which can drive higher engagement and longer-term revenue growth.

- Innovation in the product road map, including the introduction of a Discover tab and improved matching algorithms, is expected to improve user engagement and relevance, which could positively impact conversion rates and, ultimately, revenue growth.

- Strategically sunsetting non-core apps like Fruitz and Official allows Bumble to concentrate its resources and efforts on its core offerings, potentially improving operational efficiency and supporting margin expansion as revenue growth resumes.

- A strategic focus on enhancing the revenue model by rebalancing subscription tiers and optimizing free-to-paid conversion strategies is being pursued, which aims to support Bumble's monetization efforts and potentially increase average revenue per paying user, positively impacting earnings growth.

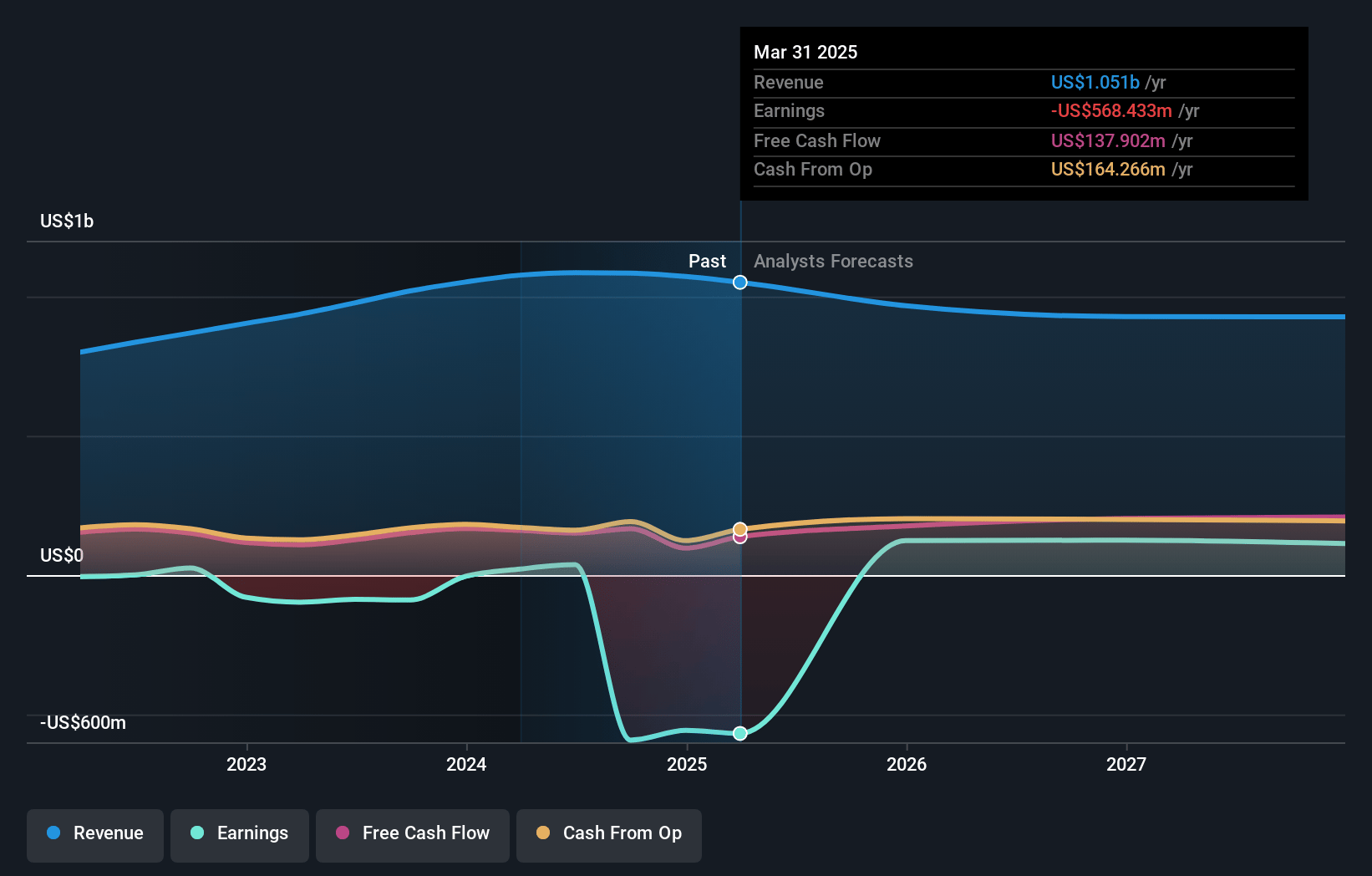

Bumble Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Bumble's revenue will decrease by 2.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from -52.0% today to 10.1% in 3 years time.

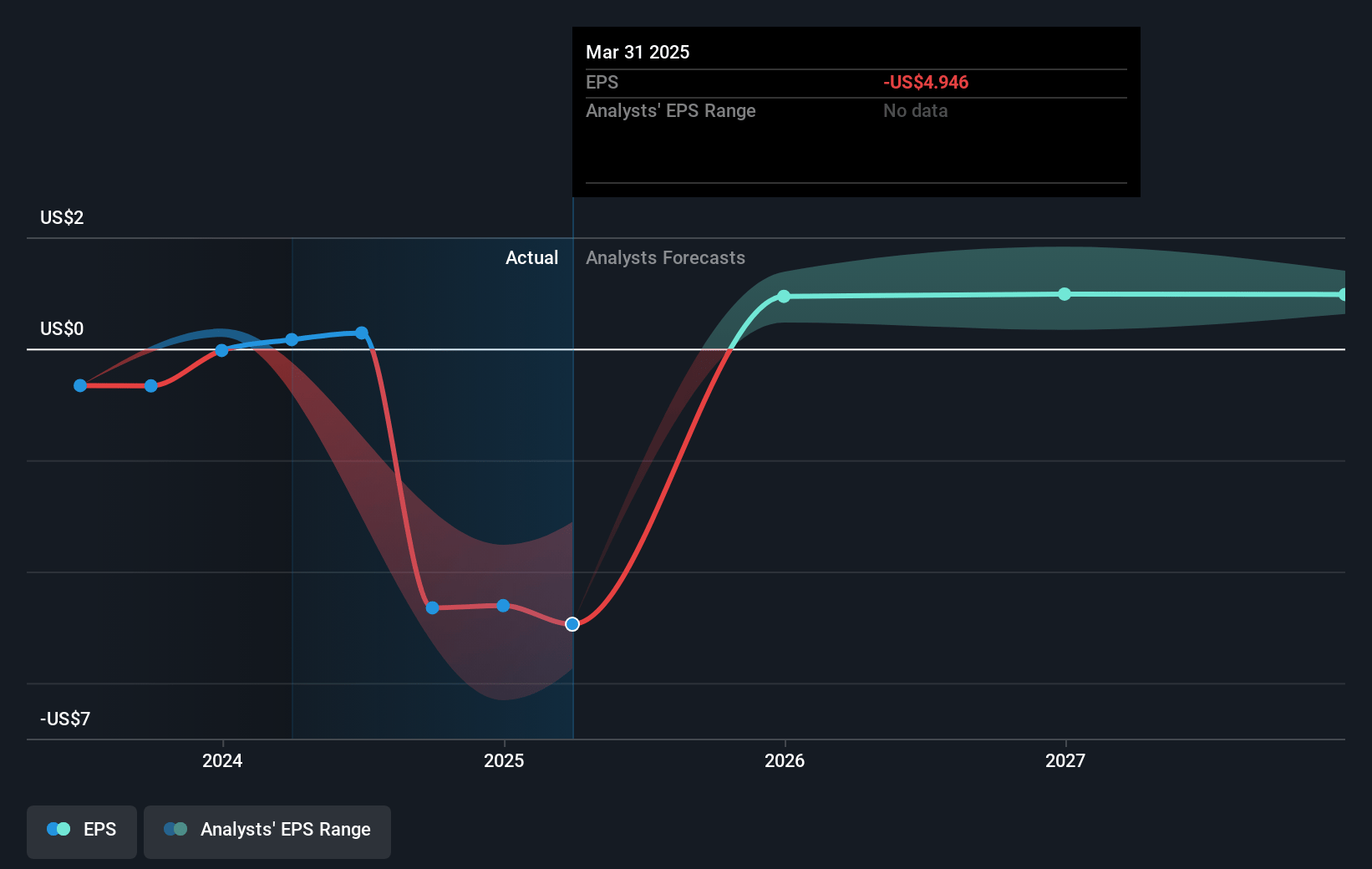

- Analysts expect earnings to reach $101.5 million (and earnings per share of $0.71) by about May 2028, up from $-557.3 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $156.6 million in earnings, and the most bearish expecting $33 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.1x on those 2028 earnings, up from -0.8x today. This future PE is lower than the current PE for the US Interactive Media and Services industry at 16.9x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.78%, as per the Simply Wall St company report.

Bumble Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ecosystem health initiatives, such as removing unhealthy and bad actor accounts, are likely to create headwinds to paying user growth in the coming quarters. This could negatively impact revenue.

- Strategic decisions to sunset Fruitz and Official could result in a $12 million revenue headwind for the year, potentially affecting overall earnings.

- Adjusted EBITDA margins are expected to contract as they navigate revenue headwinds and invest in product and technology to reignite usage and engagement. This investment may put pressure on net margins.

- The decline in Average Revenue Per Paying User (ARPPU) by 8% for the Bumble App and 12% for Badoo App, driven primarily by geographic mix shifts, can negatively impact revenue per user, affecting overall earnings.

- Near-term guidance projects a sequential decline in paying users by 100,000 to 120,000 as they prioritize strengthening their ecosystem, which may lead to a decrease in short-term revenue and lower earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $5.8 for Bumble based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $8.0, and the most bearish reporting a price target of just $4.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.0 billion, earnings will come to $101.5 million, and it would be trading on a PE ratio of 9.1x, assuming you use a discount rate of 9.8%.

- Given the current share price of $4.28, the analyst price target of $5.8 is 26.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.