Key Takeaways

- Advances in alternative and at-home dialysis technologies by competitors threaten to erode Rockwell Medical's market share and limit future revenue growth.

- Industry consolidation and healthcare cost pressures risk driving down prices and reimbursement rates, making sustainable profitability more challenging for Rockwell Medical.

- Heavy reliance on a few customers, ongoing losses, market headwinds, and disruptive technologies threaten both revenue stability and long-term viability.

Catalysts

About Rockwell Medical- Develops, manufactures, commercializes, and distributes various hemodialysis products for dialysis providers worldwide.

- While Rockwell Medical stands to benefit from the ongoing aging of the global population and rising prevalence of chronic kidney disease-trends that should support increased long-term demand for its dialysis concentrates and therapies-industry advances in alternative renal replacement options, such as wearable artificial kidneys, could sharply diminish the traditional in-center dialysis market, limiting potential future revenue growth.

- Although the shift toward home-based healthcare solutions and a preference for patient-friendly therapies should offer Rockwell Medical room for product innovation and expanded adoption of its portable solutions, rapid progress in advanced at-home dialysis technologies by competitors risks reducing Rockwell's share in this evolving segment and constraining increases in addressable revenue.

- Despite the company's successful execution of multi-year supply contracts with major customers, which may stabilize and provide greater predictability to revenue in the near term, delays in the development and regulatory approval of Rockwell's next-generation products would hinder its ability to diversify revenue streams and achieve meaningful margin expansion over the longer horizon.

- While Rockwell has effectively reduced customer concentration risk and improved operational efficiency, continued global cost pressures in healthcare funding may lead to lower reimbursement rates for dialysis-related treatments, directly impacting net margins and making sustainable profitability more challenging.

- Even as industry consolidation and vertical integration among large dialysis providers could grant more stable distribution channels for Rockwell, such consolidation also increases the bargaining power of these customers, potentially forcing down prices for Rockwell's products and thereby putting persistent downward pressure on both gross margin and future earnings.

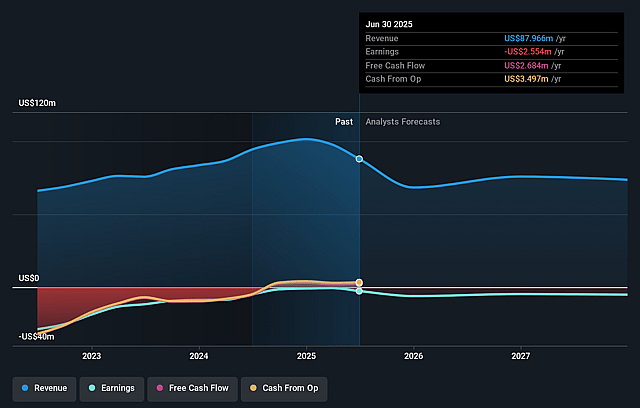

Rockwell Medical Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Rockwell Medical compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Rockwell Medical's revenue will decrease by 6.7% annually over the next 3 years.

- The bearish analysts are not forecasting that Rockwell Medical will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Rockwell Medical's profit margin will increase from -2.9% to the average US Medical Equipment industry of 12.5% in 3 years.

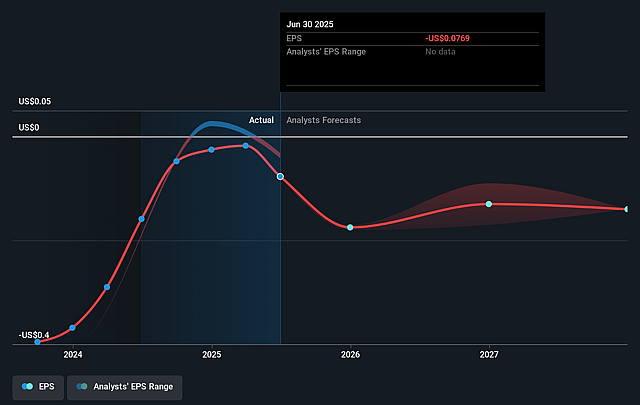

- If Rockwell Medical's profit margin were to converge on the industry average, you could expect earnings to reach $8.9 million (and earnings per share of $0.22) by about September 2028, up from $-2.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 17.4x on those 2028 earnings, up from -23.3x today. This future PE is lower than the current PE for the US Medical Equipment industry at 28.6x.

- Analysts expect the number of shares outstanding to grow by 6.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.96%, as per the Simply Wall St company report.

Rockwell Medical Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rockwell Medical's revenue and gross profit fell sharply year over year, driven primarily by the loss of its largest customer, which exposes the company to ongoing risks in customer retention and could further depress top-line revenue if customer acquisition efforts stall.

- Despite initiatives to diversify, the company remains heavily dependent on a concentrated customer base, and failure to secure new long-term contracts or renew existing ones may drive unpredictable swings in revenue and threaten margin stability in future periods.

- The dialysis market overall faces potential long-term headwinds from global healthcare cost contention, including pressures on reimbursement rates and potential cost cuts from providers, threatening the company's ability to achieve sustainable growth in both revenue and future net margins.

- Continuous net losses and negative adjusted EBITDA reflect challenges in reaching consistent profitability, and prolonged lack of profitability may force Rockwell Medical to rely on external capital raises, potentially diluting earnings per share and straining overall financial health.

- Medical device innovations and alternate renal therapies, such as wearable artificial kidneys or home-based technologies, may disrupt the traditional hemodialysis model Rockwell serves, ultimately reducing market demand for their core products and limiting the company's long-term revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Rockwell Medical is $3.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Rockwell Medical's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $5.0, and the most bearish reporting a price target of just $3.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $71.3 million, earnings will come to $8.9 million, and it would be trading on a PE ratio of 17.4x, assuming you use a discount rate of 8.0%.

- Given the current share price of $1.73, the bearish analyst price target of $3.0 is 42.3% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.