Key Takeaways

- Rapid expansion, menu innovation, and digital enhancements are fueling revenue growth, margin improvement, and deeper engagement with younger consumer segments.

- International and licensed growth, combined with operational improvements and brand adaptation, offer diversification, higher-margin income, and increased resilience against changing consumer trends.

- Sustained urban market challenges, health-driven consumer trends, rising costs, and expansion risks threaten Shake Shack’s growth, profitability, and operational flexibility.

Catalysts

About Shake Shack- Owns, operates, and licenses Shake Shack restaurants (Shacks) in the United States and internationally.

- Accelerating new unit growth, with a rapidly expanding pipeline into high-growth urban and suburban markets, including drive-thrus and nontraditional locations, positions Shake Shack to capture more revenue as rising urbanization and shifting demographics boost demand for experiential, premium fast-casual dining.

- Robust menu innovation, featuring new beverage and premium sandwich platforms, and a disciplined approach to regional adaptation, is set to drive increased frequency and higher average check. This leverages changing consumer preferences for transparency and quality, enabling future menu pricing power while supporting top-line growth and gross profit expansion.

- Significant operational improvements, including new labor models, enhanced supply chain execution, and technology platforms such as digital ordering and advanced guest recognition, are delivering rapid restaurant-level margin expansion. These efforts are expected to boost net margins by at least 50 basis points annually, substantially increasing future earnings.

- Optimized digital capabilities, including the rollout of targeted loyalty initiatives and improved digital ordering, are designed to deepen engagement with millennial and Gen Z cohorts. This can materially lift revenue per location while supporting improved customer retention and spend.

- A strong runway for international and licensed expansion—leveraging the brand’s popularity and local innovation—will diversify income streams, provide additional high-margin revenue, and help Shake Shack capture global growth as consumer preference for quality, sustainability, and responsible brands accelerates.

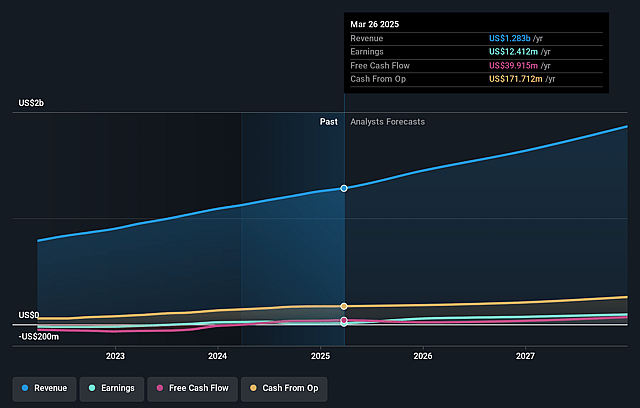

Shake Shack Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Shake Shack compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Shake Shack's revenue will grow by 17.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 1.0% today to 5.4% in 3 years time.

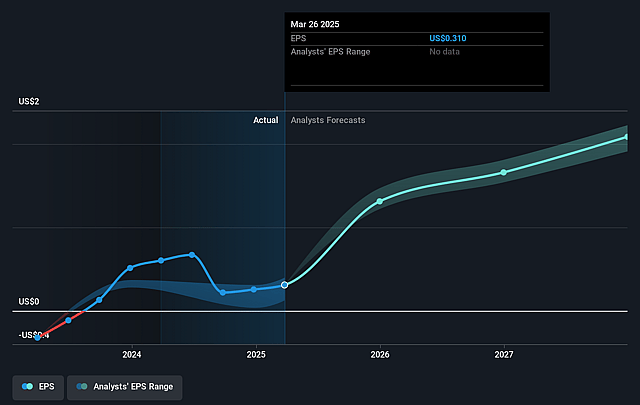

- The bullish analysts expect earnings to reach $110.4 million (and earnings per share of $2.58) by about July 2028, up from $12.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 83.0x on those 2028 earnings, down from 435.9x today. This future PE is greater than the current PE for the US Hospitality industry at 24.5x.

- Analysts expect the number of shares outstanding to grow by 0.6% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.24%, as per the Simply Wall St company report.

Shake Shack Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Declining traffic due to macroeconomic pressures, consumer sentiment, and unfavorable weather—especially in core urban markets like New York and Los Angeles—could persist or worsen, limiting comparable sales growth and putting sustained pressure on total revenues.

- A long-term consumer shift toward health and wellness, and away from indulgent fast-casual foods such as premium burgers and shakes, poses a risk to Shake Shack’s brand relevance and could dampen its ability to grow traffic and drive recurring sales.

- Ongoing high rents and labor costs in prime city locations, coupled with increasing regulatory pressures around wages and scheduling, threaten to compress net margins and may challenge Shake Shack’s ability to achieve sustained profitability as it expands its footprint.

- Heavy reliance on leased properties, particularly in high-cost urban markets that have recently underperformed due to factors such as tourism declines and regional macroeconomic pressures, exposes the company to rising occupancy costs and reduces flexibility, potentially impacting long-term EBITDA growth and operating margins.

- Rapid expansion plans, including the goal to more than quadruple company-operated units, faces execution risk if international expansion lags, new units fail to meet targeted returns, or if menu innovation does not sufficiently drive traffic—potentially leading to diluted returns on invested capital and lower overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Shake Shack is $168.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Shake Shack's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $168.0, and the most bearish reporting a price target of just $97.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $2.1 billion, earnings will come to $110.4 million, and it would be trading on a PE ratio of 83.0x, assuming you use a discount rate of 8.2%.

- Given the current share price of $134.51, the bullish analyst price target of $168.0 is 19.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.