Key Takeaways

- Accelerated onboarding of major clients, AI adoption, and multisource integration may drive substantial revenue growth and strengthen Sabre's competitive position in digital travel retailing.

- Recent debt reduction and asset sales could enable reinvestment in high-margin cloud solutions, boosting operating leverage and expanding margins ahead of expectations.

- Growing direct bookings, agile new competitors, high debt, outdated tech, and heavy customer concentration threaten Sabre's revenue stability, competitive advantage, and long-term profitability.

Catalysts

About Sabre- Operates as a software and technology company for travel industry in the United States, Europe, Asia-Pacific, and internationally.

- Analyst consensus expects new business implementation and multisource content to drive modest transaction growth, but given Sabre's strong pipeline and accelerating onboarding of major clients, realized air distribution bookings could substantially exceed expectations, directly boosting revenue growth and market share through at least 2026.

- While analysts broadly view the recent debt reduction and Hospitality Solutions sale as simply improving credit metrics, the resulting $1 billion-plus debt paydown and $55–65 million annual interest savings could enable aggressive reinvestment in high-margin cloud and AI solutions, amplifying operating leverage and driving faster-than-expected expansion in both free cash flow and net margins.

- Sabre's rapid adoption and commercialization of AI-powered offer management tools (such as SabreMosaic) positions it to become the leading platform for data-driven, personalized travel retailing worldwide, which could unlock premium pricing power and margin accretion beyond current forecasts.

- The accelerating global middle class-especially in emerging markets-combined with Sabre's cloud-native platform, enables the company to capture a disproportionately large share of the explosive growth in digital-first travel, driving sustained double-digit revenue growth as global travel rebounds.

- Sabre's early-mover advantage in next-generation multisource distribution, including deep integration with long-tail low-cost carriers and alternative accommodations, not only diversifies its revenue streams but could transform it into the essential commerce infrastructure for a fragmented travel industry, driving both recurring revenue growth and durable competitive moats.

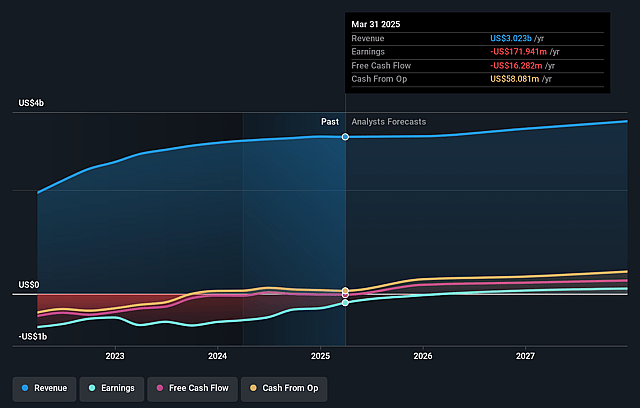

Sabre Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Sabre compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Sabre's revenue will decrease by 1.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -11.5% today to 0.7% in 3 years time.

- The bullish analysts expect earnings to reach $20.8 million (and earnings per share of $0.39) by about September 2028, up from $-345.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 111.8x on those 2028 earnings, up from -2.0x today. This future PE is greater than the current PE for the US Hospitality industry at 23.9x.

- Analysts expect the number of shares outstanding to grow by 2.24% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.32%, as per the Simply Wall St company report.

Sabre Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The accelerating industry trend of airlines and hotels adopting direct-to-consumer booking channels and bypassing global distribution systems like Sabre presents a structural threat that could reduce overall transaction volumes and long-term revenue growth opportunities for the company.

- Heightened competition from new, agile travel technology players leveraging open-source and cloud-native platforms increases the risk of Sabre's services being commoditized, which could lead to ongoing margin pressure and loss of pricing power affecting net margins and earnings.

- Sabre's continued reliance on legacy, mainframe-based infrastructure constrains its pace of innovation and increases its technology maintenance costs, limiting its ability to rapidly compete in a travel landscape that increasingly values flexibility and interoperability, which could weigh on future profitability and operational efficiency.

- Persistent high debt levels and significant interest expenses, despite recent efforts to deleverage, remain a major financial headwind, restricting Sabre's ability to invest aggressively in next-generation technologies and keep up with industry disruptions, thereby threatening sustained earnings growth and free cash flow.

- Sabre's heavy exposure to a concentrated base of large customers in corporate and government travel creates substantial vulnerability to shifts in the travel market or contract losses; this dependence leaves Sabre exposed to revenue volatility and downward pricing pressure as these clients gain more bargaining power through industry consolidation.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Sabre is $3.9, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Sabre's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $3.9, and the most bearish reporting a price target of just $2.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $3.1 billion, earnings will come to $20.8 million, and it would be trading on a PE ratio of 111.8x, assuming you use a discount rate of 12.3%.

- Given the current share price of $1.77, the bullish analyst price target of $3.9 is 54.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.