Key Takeaways

- Growing health concerns, strict regulations, and volatile ingredient costs threaten demand, gross margins, and the viability of international growth.

- Labor shortages, wage inflation, and intensifying delivery competition erode profitability and challenge franchise and company-owned store performance.

- Ongoing tech investment, international growth, strategic refranchising, and operational improvements position the company for strengthened margins, enhanced profitability, and diversified long-term earnings.

Catalysts

About Papa John's International- Operates and franchises pizza delivery and carryout restaurants under the Papa Johns trademark in the United States, Canada, and internationally.

- As health-conscious consumer preferences strengthen and more stringent regulations around unhealthy ingredients are implemented, Papa John’s core offering of calorie-dense, processed fast food may face declining demand, eroding same-store sales growth and limiting long-term expansion potential in key markets, which would pressure top-line revenue and hamper the company’s international ambitions.

- Persistent labor shortages and rising wage pressures across the United States and global markets will continue to drive up operational costs, compressing restaurant-level profitability and putting sustained downward pressure on net margins for both company-owned and franchised stores.

- Despite investments in digital and technology partnerships such as Google Cloud, intensifying competition from third-party delivery disruptors and an explosion of virtual brands threaten to fragment customer attention and siphon off a growing portion of delivery revenue, challenging Papa John’s ability to sustain customer frequency and maintain its share of off-premise dining, undermining both revenue growth and profitability.

- Papa John’s relatively limited global scale compared to larger quick-service restaurant competitors will inhibit its ability to achieve broad international reach and benefit from economies of scale, resulting in higher per-unit operating costs and a muted impact from ongoing international expansion, limiting potential for material long-term earnings growth.

- Increased volatility in commodity prices for core ingredients like cheese and wheat—exacerbated by climate change and ongoing supply chain disruptions—will create continuous pressure on gross margins, reduce pricing flexibility, and add further unpredictability to earnings, especially as price-sensitive consumers resist menu price increases.

Papa John's International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Papa John's International compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

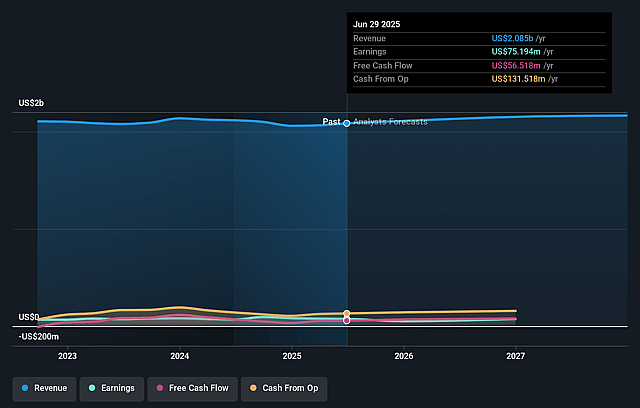

- The bearish analysts are assuming Papa John's International's revenue will grow by 2.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 3.8% today to 2.7% in 3 years time.

- The bearish analysts expect earnings to reach $59.3 million (and earnings per share of $1.79) by about July 2028, down from $77.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 27.9x on those 2028 earnings, up from 19.2x today. This future PE is greater than the current PE for the US Hospitality industry at 24.5x.

- Analysts expect the number of shares outstanding to grow by 0.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.67%, as per the Simply Wall St company report.

Papa John's International Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Papa John’s is experiencing sequential improvements in transaction share, increased pizza orders, and momentum from menu innovation, which suggest the potential for stabilizing or growing revenue and EBITDA in the long term.

- Aggressive investment in technology infrastructure, including a major partnership with Google Cloud and a data-driven CRM, is expected to boost customer engagement, order conversion, and personalization—contributing to higher frequency, repeat purchases, and potentially expanding digital-driven margins.

- International markets are driving mid-single to double-digit growth in select focus countries, with share gains noted in regions experiencing market consolidation, which could offset plateauing North American sales and diversify earnings streams over time.

- Franchisee interest in refranchising company-owned stores remains high, with quality-oriented operators driving better 4-wall economics, suggesting that optimized unit economics and strategic refranchising could enhance profitability and support earnings growth.

- Planned multi-year supply chain optimization, menu simplification, and restaurant reimaging initiatives are designed to improve efficiency, brand perception, and operational consistency, which are likely to strengthen margins, reduce costs, and support sustained long-term earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Papa John's International is $38.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Papa John's International's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $60.0, and the most bearish reporting a price target of just $38.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $2.2 billion, earnings will come to $59.3 million, and it would be trading on a PE ratio of 27.9x, assuming you use a discount rate of 9.7%.

- Given the current share price of $45.53, the bearish analyst price target of $38.0 is 19.8% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.