Key Takeaways

- The R2 platform and manufacturing expansion could significantly enhance production efficiency and margins, positively impacting revenue and profitability.

- Strategic partnerships and a focus on autonomous driving technology are positioned to bolster financial strength and enhance consumer appeal.

- Complex trade regulations, tariffs, and supply chain risks could pressure Rivian's costs and profitability amid a sensitive market environment.

Catalysts

About Rivian Automotive- Designs, develops, manufactures, and sells electric vehicles and accessories.

- Rivian's upcoming R2 platform launch is expected to start at $45,000, substantially lowering the market entry point and potentially increasing volumes significantly, which could improve revenue and spread fixed manufacturing costs over more units, positively impacting net margins and earnings.

- The development and introduction of the Rivian Autonomy Platform with a focus on AI-centric autonomous driving technology could enhance the product experience and drive consumer preference, potentially boosting sales and revenue.

- The planned expansion of Rivian's manufacturing capacity, including a new facility in Georgia and a supplier park in Illinois, could help escalate production efficiency and reduce costs, benefiting gross profit margins and overall profitability.

- Anticipated $1 billion investment from Volkswagen Group, tied to achieving gross profit milestones, could bolster Rivian's financial position and support further technological and production developments, positively impacting earnings.

- Strategic adjustments in sourcing, particularly for battery production to move to the U.S. by 2027, could mitigate tariff impacts and contribute to cost stability in battery sourcing, enhancing future net margins and earnings predictability.

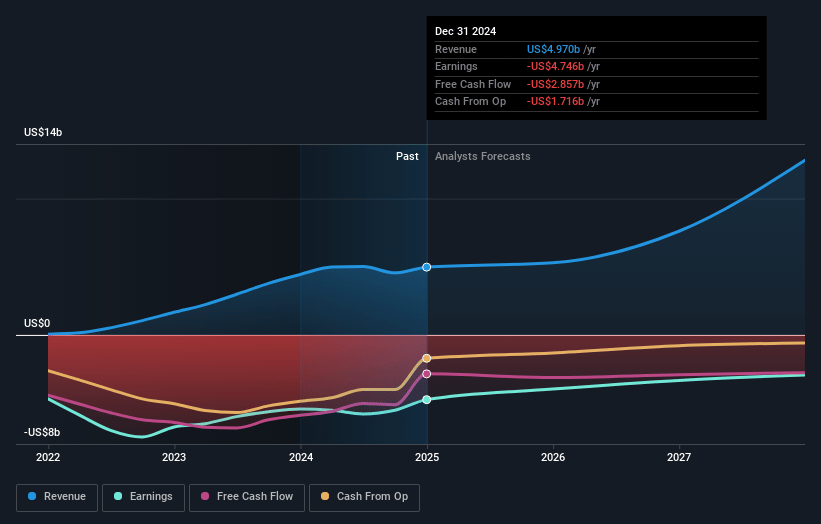

Rivian Automotive Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Rivian Automotive's revenue will grow by 39.6% annually over the next 3 years.

- Analysts are not forecasting that Rivian Automotive will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Rivian Automotive's profit margin will increase from -76.8% to the average US Auto industry of 5.3% in 3 years.

- If Rivian Automotive's profit margin were to converge on the industry average, you could expect earnings to reach $727.3 million (and earnings per share of $0.5) by about July 2028, up from $-3.8 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 41.5x on those 2028 earnings, up from -4.4x today. This future PE is greater than the current PE for the US Auto industry at 15.7x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.6%, as per the Simply Wall St company report.

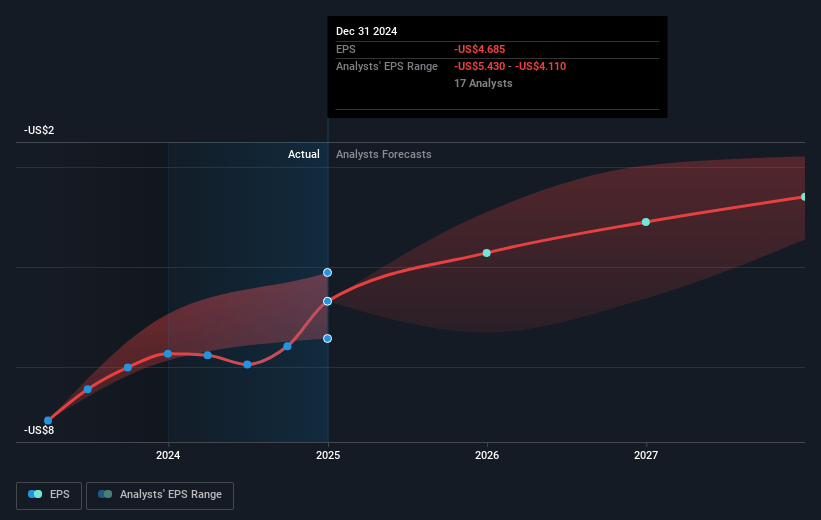

Rivian Automotive Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The global trade regulation and policy environment is complex and rapidly evolving, impacting Rivian's material costs, availability, capital expenditures, and demand, which may affect net margins and earnings.

- The planned tariffs on batteries could lead to increased costs per unit, with a direct impact anticipated to be a couple of thousand dollars per vehicle in 2025, potentially affecting Rivian's gross margins and overall profitability.

- There is a significant dependence on LG battery cells initially produced outside the U.S., with tariff implications posing a risk to the cost structure of the R2, which could impact net margins.

- Exposure to changes in rare earth supply dynamics, particularly with the processing concentrated in China, poses a risk to production costs and supply chain reliability, potentially impacting earnings.

- The consumer price sensitivity and reduction in deliverable guidance indicate a demanding market environment, potentially affecting revenues and earnings outlook.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $14.79 for Rivian Automotive based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $23.0, and the most bearish reporting a price target of just $7.05.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $13.6 billion, earnings will come to $727.3 million, and it would be trading on a PE ratio of 41.5x, assuming you use a discount rate of 11.6%.

- Given the current share price of $14.12, the analyst price target of $14.79 is 4.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.