Key Takeaways

- Expansion of proprietary platforms and games supports margin growth, but genre reliance and rising compliance costs threaten revenue stability and future earnings.

- Industry headwinds like global taxation and app store fees may offset gains from mobile growth and digital payments, dampening long-term profitability.

- Reliance on a shrinking base of high-spending users, rising acquisition costs, currency exposure, slow store ramp-up, and limited genre innovation threaten revenue stability and growth.

Catalysts

About G5 Entertainment- Develops and publishes free-to-play games for smartphones, tablets, and personal computers in Sweden.

- While the company is leveraging the expansion of its own G5 Store-with lower payment processing fees and strong growth providing meaningful potential upside to gross margins over time-the shift in global digital regulations may raise compliance costs and restrict data-driven user acquisition, potentially pressuring both margins and future revenue growth.

- Although G5 Entertainment is positioned to benefit from the proliferation of smartphones and growing digital payments, broader industry headwinds such as rising global digital taxation and platform fees for mobile app stores risk offsetting improvements in average revenue per user and could dampen long-term net earnings.

- While the company's increased focus on proprietary games and IP supports higher earnings quality and margin expansion, the continued reliance on a narrow portfolio in hidden object and puzzle segments exposes G5 to the risk of genre fatigue and revenue concentration, which could undermine the stability of top-line growth if consumer preferences shift.

- Even as the expansion of the G5 Store and planned onboarding of third-party games point to diversified and recurring revenue streams, the ramp-up is expected to be gradual-so near-term contributions to revenue and gross profit may be modest, especially as user acquisition costs climb due to an increasingly saturated and competitive market.

- Although advances in AI and a disciplined approach to user acquisition are improving player monetization and engagement, the ongoing increase in user acquisition costs and the challenge of achieving meaningful success outside core markets continue to threaten long-term net margins and earnings resilience.

G5 Entertainment Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on G5 Entertainment compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming G5 Entertainment's revenue will decrease by 3.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 7.4% today to 11.2% in 3 years time.

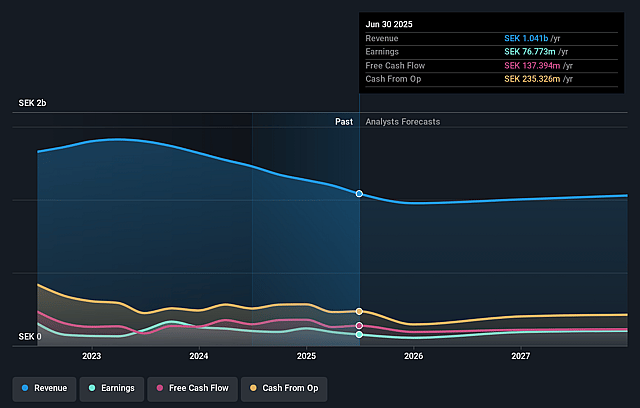

- The bearish analysts expect earnings to reach SEK 105.5 million (and earnings per share of SEK 13.52) by about September 2028, up from SEK 76.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 10.9x on those 2028 earnings, up from 9.0x today. This future PE is lower than the current PE for the GB Entertainment industry at 27.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.87%, as per the Simply Wall St company report.

G5 Entertainment Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- G5 Entertainment's increasing reliance on a smaller number of high-spending users, amid a broader decline in overall player numbers, exposes revenues and earnings to greater volatility if these high-value users reduce spending or churn.

- User acquisition costs are rising as the ecosystem becomes more competitive and organic growth declines, which could pressure net margins and make it increasingly expensive to sustain or grow the paying user base.

- The company remains exposed to significant foreign exchange risks due to its primarily USD-based operations but SEK reporting, as seen in recent periods where negative currency movements have materially impacted earnings and EBIT margins.

- The top-line growth is heavily dependent on the continued expansion and successful scaling of the G5 Store, yet management acknowledges the ramp-up is gradual, not explosive, and the ultimate impact of third-party distribution initiatives is still unproven, introducing risk to both future revenue and gross margin targets.

- The majority of new game development remains within familiar genres, and growth prospects tied to new launches such as Twilight Land are uncertain; slow innovation or failed launches in G5's core genres could result in revenue concentration risk and stagnating earnings over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for G5 Entertainment is SEK135.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of G5 Entertainment's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK240.0, and the most bearish reporting a price target of just SEK135.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be SEK942.0 million, earnings will come to SEK105.5 million, and it would be trading on a PE ratio of 10.9x, assuming you use a discount rate of 6.9%.

- Given the current share price of SEK88.7, the bearish analyst price target of SEK135.0 is 34.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.