Key Takeaways

- Demographic shifts, regulatory pressures, and higher financing costs challenge Instone's growth, margin resilience, and revenue stability in a concentrated German residential market.

- Supply chain disruptions and escalating construction costs threaten project delivery, margin expectations, and the company's ability to generate consistent cash flow.

- Robust demand, pricing power, and a strong project pipeline drive long-term earnings stability and margin expansion, supported by cost discipline and favorable government incentives.

Catalysts

About Instone Real Estate Group- Develops residential real estate properties in Germany.

- The ongoing aging population and declining birth rates in Germany and Europe are likely to significantly weaken long-term demand for new residential developments, making Instone's expansive land bank and project pipeline more of a liability, which will negatively impact revenue visibility and growth in the next decade.

- Persistently higher interest rates are expected to increase financing costs for both Instone and its buyer base, eroding affordability and forcing Instone to either lower prices or accept weaker sales volume, resulting in thinner net margins and lower earnings across project cycles.

- Strict and escalating energy efficiency and climate change regulations will drive up construction and compliance costs, with Instone forced to redesign and retrofit projects to satisfy increasingly ambitious government requirements, causing project complexity, margin compression, and possible revenue recognition delays.

- Heavy geographic concentration in the German urban residential development sector leaves Instone highly exposed to any stagflation or recession in key regions, amplifying revenue volatility and undermining long-term earnings resilience, especially if urbanization rates plateau.

- Supply chain disruptions and persistent construction cost inflation driven by labor shortages and rising raw material prices are likely to pressure Instone's ability to deliver projects at current margin expectations, causing cost overruns, delays, and an adverse impact on EBITDA and free cash flow.

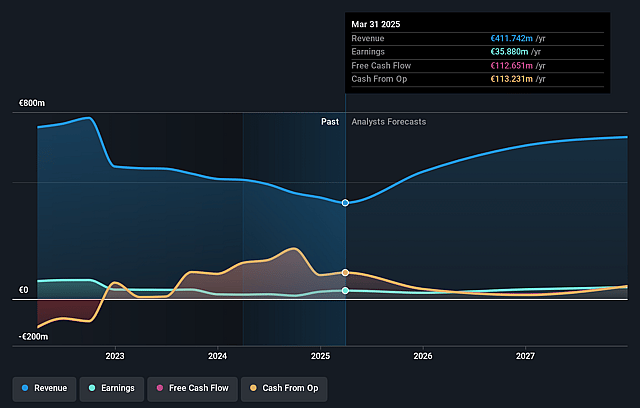

Instone Real Estate Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Instone Real Estate Group compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Instone Real Estate Group's revenue will grow by 18.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 7.2% today to 6.8% in 3 years time.

- The bearish analysts expect earnings to reach €49.0 million (and earnings per share of €nan) by about August 2028, up from €31.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 11.1x on those 2028 earnings, down from 13.6x today. This future PE is lower than the current PE for the DE Real Estate industry at 16.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.9%, as per the Simply Wall St company report.

Instone Real Estate Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent urbanization, demographic shifts, and continued population growth in German metropolitan regions are driving robust demand for new residential units, which supports revenue growth and provides long-term earnings visibility for Instone.

- Ongoing severe housing supply shortages in key cities lead to sustained upward pressure on both rents and new build prices, granting Instone pricing power and strong occupancy rates that can help maintain or expand margins.

- Favorable tax incentive programs, such as the Growth Opportunities Act and special depreciation schemes for energy-efficient buildings, are stimulating significant private investor demand and accelerating retail sales, directly boosting top line revenue and supporting strong project margins.

- Instone's large, diversified and high-quality land bank-combined with an extensive secured project pipeline and a high presales ratio of 92% on projects under construction-ensures stable future revenues, predictable free cash flow, and resilience in earnings generation.

- Sound cost discipline and an asset-light project management approach have enabled consistently high gross margins above 23%, with the capacity to capitalize on current market opportunities and improved financing access, supporting long-term profitability and reducing balance sheet risk.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Instone Real Estate Group is €9.8, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Instone Real Estate Group's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €16.0, and the most bearish reporting a price target of just €9.8.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be €725.3 million, earnings will come to €49.0 million, and it would be trading on a PE ratio of 11.1x, assuming you use a discount rate of 8.9%.

- Given the current share price of €9.8, the bearish analyst price target of €9.8 is 0.0% different. The relatively low difference between the current share price and the analyst bearish price target indicates that the bearish analysts believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.