Last Update 22 Jun 26

MS1: Stable Margins And Ultra Low Future P/E Will Support Bullish Thesis

Analysts have kept their fair value and discount rate assumptions for Marley Spoon Group unchanged, so the latest narrative update focuses on reaffirming the existing €0.25 analyst price target, which is based on steady forecasts for revenue, profit margins and future P/E.

What's in the News

- Marley Spoon Group SE announced that Chief Executive Officer Daniel Raab stepped down by mutual agreement with the Supervisory Board, effective at the end of June 8, 2026. (Source: Company announcement)

- The Supervisory Board appointed Dr. Daniel Koch as Interim Chief Executive Officer of Marley Spoon Group SE, effective June 9, 2026. (Source: Company announcement)

- Marley Spoon Group SE appointed Bastian F. Stoehr as member of the Management Board and Chief Financial Officer, effective June 8, 2026, following a structured succession process and planned finance leadership transition. (Source: Company announcement)

- The company filed its annual report on April 30, 2026, for the period ending December 31, 2025, in which auditor Forvis Mazars, LLP issued an unqualified opinion while expressing doubt about Marley Spoon Group SE's ability to continue as a going concern. (Source: Annual report)

Valuation Changes for Marley Spoon Group

- Fair Value: Analyst fair value remains steady at €0.25 per share, with no change from prior assumptions.

- Discount Rate: The discount rate used in the valuation is unchanged at 10.34%.

- Revenue: Forecast revenue expectations are effectively unchanged, with a projected 2.63% decline.

- Net Profit Margin: The projected net profit margin remains broadly the same at 10.30%.

- Future P/E: The expected future P/E multiple is stable at 0.34x, indicating no revision to the earnings multiple applied to Marley Spoon Group.

Key Takeaways

- Transition to an integrated platform model and refined marketing boost customer lifetime value and improve revenue growth and net margins.

- Cost reduction and asset-light model in U.S. enhance operational efficiency, potentially driving future earnings and improved EBITDA.

- Concerns over declining revenue, subscriber numbers, liquidity, integration risks, and marketing strategy effectiveness could challenge Marley Spoon's long-term financial stability and growth.

Catalysts

About Marley Spoon Group- Through its subsidiary, Marley Spoon SE, operates as a direct-to-consumer meal-kit company.

- The transition to an integrated platform model allows for easier expansion of products and services, diversification of revenue streams, and potentially lower marginal costs, which can improve future revenue and net margins.

- The acquisition of BistroMD and the transition to an asset-light model in the U.S. are expected to enhance product offerings and operational efficiency, driving customer lifetime value and improving earnings.

- The consolidation and brand integration strategy, exemplified by integrating the Dinnerly brand into Marley Spoon in Europe, aims to improve operational efficiency and customer experience, potentially boosting net margins and earnings.

- A refined marketing strategy focused on higher-quality customer acquisition and reduced discounting is resulting in increased average order value and order frequency, positively impacting revenue growth and net margins.

- Continued focus on cost reduction and marketing efficiency, with a 24% reduction in general administrative expenses in Q4 '24, supports the ongoing improvement in operating EBITDA, potentially enhancing future earnings.

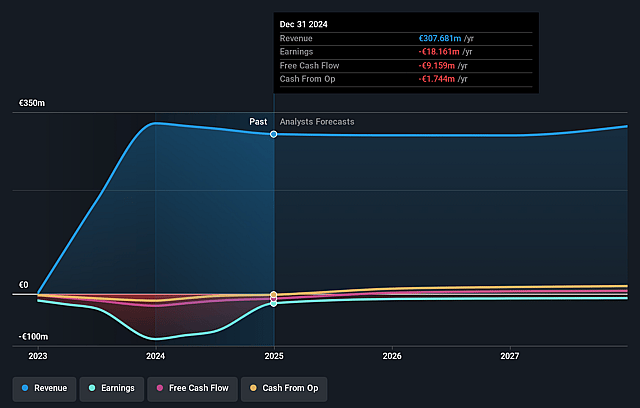

Marley Spoon Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Marley Spoon Group's revenue will decrease by 2.6% annually over the next 3 years.

- Analysts are not forecasting that Marley Spoon Group will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Marley Spoon Group's profit margin will increase from -7.7% to the average DE Hospitality industry of 10.3% in 3 years.

- If Marley Spoon Group's profit margin were to converge on the industry average, you could expect earnings to reach €22.7 million (and earnings per share of €0.97) by about June 2029, up from -€18.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 0.3x on those 2029 earnings, up from -0.0x today. This future PE is lower than the current PE for the DE Hospitality industry at 14.4x.

- Analysts expect the number of shares outstanding to grow by 6.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.34%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Despite cost-cutting measures and improved operating efficiencies, Marley Spoon is guiding for a single-digit revenue decline in 2025, which could negatively impact overall revenue growth and financial stability.

- Active subscriber numbers have declined year-over-year, especially in the U.S., indicating potential challenges in maintaining or growing the customer base, which could affect future revenue and earnings.

- With only €6 million in cash at the end of 2024 and no clear timeline for achieving cash flow positivity, there are concerns over liquidity and the ability to fund future operations, potentially impacting overall financial health and investor confidence.

- The integration of acquired businesses, like BistroMD, involves execution risks, and if not managed well, could lead to operational inefficiencies or fail to realize anticipated synergies, affecting profit margins and overall earnings.

- The company's reliance on changing marketing strategies and reducing voucher incentives for customer acquisition may not sustain long-term growth if the quality improvements and cost efficiencies do not translate into increased customer engagement and retention, potentially impacting revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €0.25 for Marley Spoon Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €220.0 million, earnings will come to €22.7 million, and it would be trading on a PE ratio of 0.3x, assuming you use a discount rate of 10.3%.

- Given the current share price of €0.04, the analyst price target of €0.25 is 84.6% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Marley Spoon Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.