Key Takeaways

- Geopolitical tensions, regulatory changes, and new digital competitors threaten UBS's international growth, client loyalty, and overall fee-based income.

- Integration challenges and policy risks post-Credit Suisse acquisition could inflate costs, trigger client outflows, and constrain future profit improvements.

- Growth in wealth management, successful integration of Credit Suisse, and tech-driven efficiency are boosting profitability, with strong positions in key global and emerging markets.

Catalysts

About UBS Group- Provides financial advice and solutions to private, institutional, and corporate clients worldwide.

- Intensifying geopolitical fragmentation and escalating trade barriers, such as new tariffs and increased regulatory friction, are set to constrain UBS's ability to grow its international wealth management business or maintain cross-border asset flows. This will likely result in slower future revenue growth and diminish profit opportunities in key emerging markets.

- Accelerated adoption of advanced digital finance and decentralized platforms is fueling new, non-traditional competition, undermining UBS's capacity to protect its client base, eroding brand loyalty and traditional banking margins. This shift threatens to structurally compress net margins and fee-based income as clients migrate to lower-fee or alternative providers.

- The significant integration risks following the Credit Suisse acquisition remain unresolved, with the potential for protracted elevated operating costs, unexpected restructuring charges, and stubborn client attrition. These factors could persist for years, jeopardizing the anticipated improvement in profit margins and delaying any sustainable uplift in earnings.

- UBS's high dependency on ultra-high-net-worth and high-net-worth clients makes its fee and revenue streams acutely vulnerable to adverse shifts in global wealth policy, including increased taxation or financial transaction levies. Such policy actions could shrink the investible asset pool and accelerate outflows, exerting downward pressure on both revenue and net profit over time.

- Ongoing tightening of global banking regulations and heightened capital requirements, especially in Switzerland post-Credit Suisse integration, will continue to increase compliance costs and limit financial leverage. This environment is poised to suppress return on equity and hinder long-term earnings growth, particularly as leverage constraints become more binding and difficult to optimize further.

UBS Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on UBS Group compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

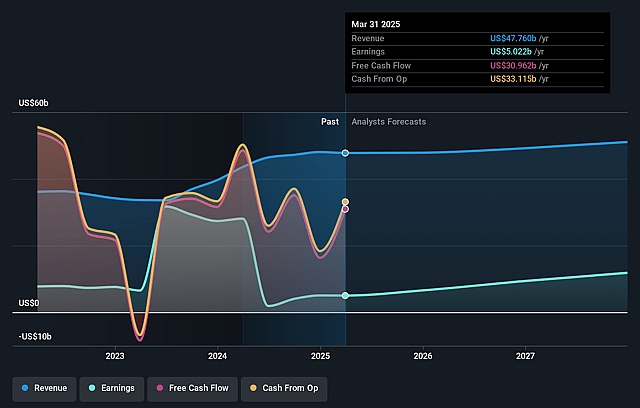

- The bearish analysts are assuming UBS Group's revenue will decrease by 1.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 10.5% today to 24.5% in 3 years time.

- The bearish analysts expect earnings to reach $12.0 billion (and earnings per share of $4.35) by about July 2028, up from $5.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 8.9x on those 2028 earnings, down from 23.2x today. This future PE is lower than the current PE for the GB Capital Markets industry at 23.1x.

- Analysts expect the number of shares outstanding to decline by 0.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.08%, as per the Simply Wall St company report.

UBS Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Robust growth in Global Wealth Management, driven by strong net new asset inflows across all regions, successful client migration, and record growth rates in APAC and the Americas, is supporting recurring fee income and top-line revenue expansion.

- Accelerated progress in Credit Suisse integration, evidenced by substantial cost synergies, streamlined technology infrastructure, and upgrades in risk-weighted asset targets, is already delivering significant underlying cost reductions, which enhances future net margins and profitability.

- Continued investment and adoption of technology, including generative AI and unified digital platforms, is increasing operational efficiency and productivity, enabling scalable client engagement and supporting cost-to-income improvements over the medium to long term.

- UBS's leadership in fast-growing markets, especially Asia-Pacific and India (via partnerships and local expansion), is positioning the firm to capture secular increases in wealth and drive asset and revenue growth from emerging markets.

- Strengthened capital position, resilient balance sheet, and stable funding allow for continued share repurchases and dividend returns, as well as strategic capital deployment, all of which support per-share earnings growth and increased shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for UBS Group is CHF21.99, which represents two standard deviations below the consensus price target of CHF30.1. This valuation is based on what can be assumed as the expectations of UBS Group's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF37.0, and the most bearish reporting a price target of just CHF21.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $49.2 billion, earnings will come to $12.0 billion, and it would be trading on a PE ratio of 8.9x, assuming you use a discount rate of 9.1%.

- Given the current share price of CHF30.62, the bearish analyst price target of CHF21.99 is 39.3% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives