- United States

- /

- Auto Components

- /

- NYSE:LCII

Shareholders May Be Wary Of Increasing LCI Industries' (NYSE:LCII) CEO Compensation Package

Key Insights

- LCI Industries to hold its Annual General Meeting on 16th of May

- Salary of US$1.16m is part of CEO Jason Lippert's total remuneration

- The overall pay is 39% above the industry average

- LCI Industries' EPS declined by 23% over the past three years while total shareholder loss over the past three years was 7.8%

The results at LCI Industries (NYSE:LCII) have been quite disappointing recently and CEO Jason Lippert bears some responsibility for this. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 16th of May. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. From our analysis, we think CEO compensation may need a review in light of the recent performance.

View our latest analysis for LCI Industries

How Does Total Compensation For Jason Lippert Compare With Other Companies In The Industry?

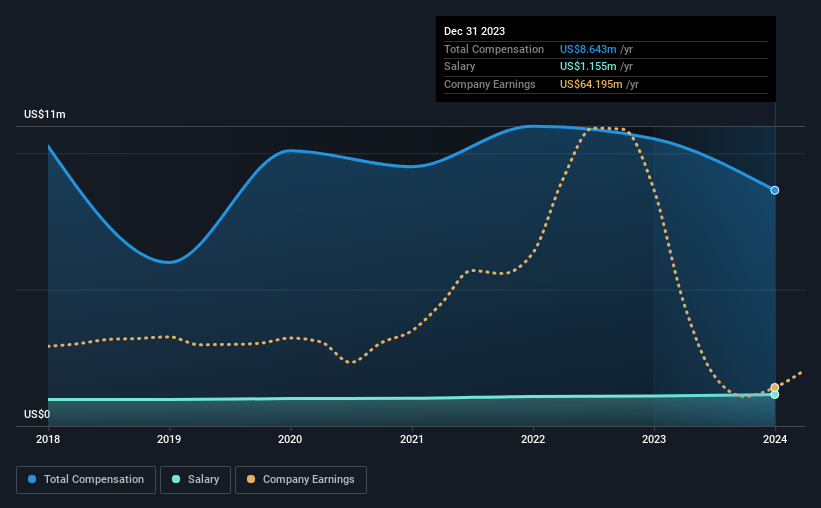

Our data indicates that LCI Industries has a market capitalization of US$2.8b, and total annual CEO compensation was reported as US$8.6m for the year to December 2023. That's a notable decrease of 18% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$1.2m.

For comparison, other companies in the American Auto Components industry with market capitalizations ranging between US$2.0b and US$6.4b had a median total CEO compensation of US$6.2m. Hence, we can conclude that Jason Lippert is remunerated higher than the industry median. Moreover, Jason Lippert also holds US$44m worth of LCI Industries stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$1.2m | US$1.1m | 13% |

| Other | US$7.5m | US$9.4m | 87% |

| Total Compensation | US$8.6m | US$11m | 100% |

Speaking on an industry level, nearly 13% of total compensation represents salary, while the remainder of 87% is other remuneration. Although there is a difference in how total compensation is set, LCI Industries more or less reflects the market in terms of setting the salary. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

LCI Industries' Growth

LCI Industries has reduced its earnings per share by 23% a year over the last three years. In the last year, its revenue is down 17%.

Few shareholders would be pleased to read that EPS have declined. This is compounded by the fact revenue is actually down on last year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has LCI Industries Been A Good Investment?

Since shareholders would have lost about 7.8% over three years, some LCI Industries investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 3 warning signs for LCI Industries that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:LCII

LCI Industries

Manufactures and supplies engineered components for the manufacturers of recreational vehicles (RVs) and adjacent industries in the United States and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion