- South Africa

- /

- Real Estate

- /

- JSE:TMT

We Think The Compensation For Trematon Capital Investments Limited's (JSE:TMT) CEO Looks About Right

CEO Arnold Shapiro has done a decent job of delivering relatively good performance at Trematon Capital Investments Limited (JSE:TMT) recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 25 January 2023. Here is our take on why we think the CEO compensation looks appropriate.

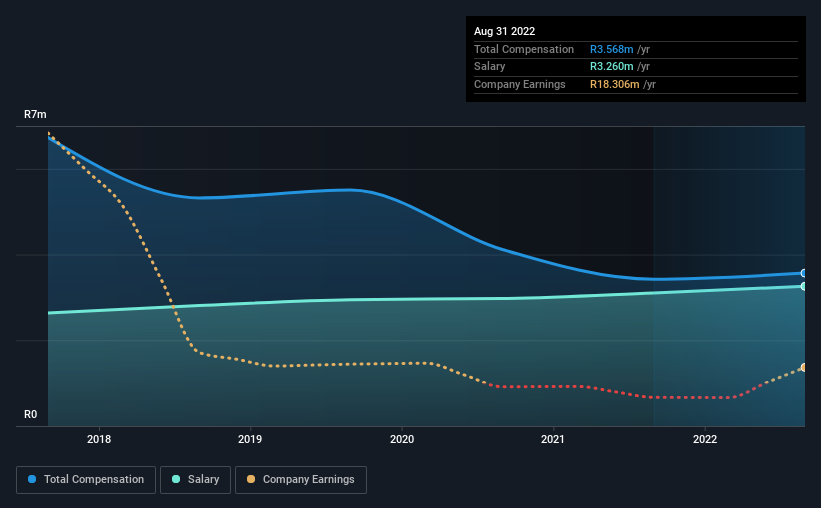

See our latest analysis for Trematon Capital Investments

How Does Total Compensation For Arnold Shapiro Compare With Other Companies In The Industry?

At the time of writing, our data shows that Trematon Capital Investments Limited has a market capitalization of R768m, and reported total annual CEO compensation of R3.6m for the year to August 2022. That's just a smallish increase of 4.2% on last year. Notably, the salary which is R3.26m, represents most of the total compensation being paid.

On comparing similar-sized companies in the South Africa Real Estate industry with market capitalizations below R3.4b, we found that the median total CEO compensation was R3.6m. So it looks like Trematon Capital Investments compensates Arnold Shapiro in line with the median for the industry. Moreover, Arnold Shapiro also holds R64m worth of Trematon Capital Investments stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | R3.3m | R3.1m | 91% |

| Other | R308k | R320k | 9% |

| Total Compensation | R3.6m | R3.4m | 100% |

Talking in terms of the industry, salary represented approximately 84% of total compensation out of all the companies we analyzed, while other remuneration made up 16% of the pie. There isn't a significant difference between Trematon Capital Investments and the broader market, in terms of salary allocation in the overall compensation package. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Trematon Capital Investments Limited's Growth

Over the last three years, Trematon Capital Investments Limited has shrunk its earnings per share by 7.5% per year. It achieved revenue growth of 22% over the last year.

Investors would be a bit wary of companies that have lower EPS But in contrast the revenue growth is strong, suggesting future potential for EPS growth. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Trematon Capital Investments Limited Been A Good Investment?

Most shareholders would probably be pleased with Trematon Capital Investments Limited for providing a total return of 66% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Although the company has performed relatively well, we still think there are some areas that could be improved. Despite robust revenue growth, until EPS growth improves, shareholders may be hesitant to increase CEO pay by too much.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. That's why we did our research, and identified 6 warning signs for Trematon Capital Investments (of which 2 don't sit too well with us!) that you should know about in order to have a holistic understanding of the stock.

Important note: Trematon Capital Investments is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you're looking to trade Trematon Capital Investments, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Trematon Capital Investments might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:TMT

Slight and slightly overvalued.