- South Africa

- /

- Real Estate

- /

- JSE:TMT

Trematon Capital Investments Limited's (JSE:TMT) 30% Price Boost Is Out Of Tune With Earnings

Despite an already strong run, Trematon Capital Investments Limited (JSE:TMT) shares have been powering on, with a gain of 30% in the last thirty days. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 5.0% over the last year.

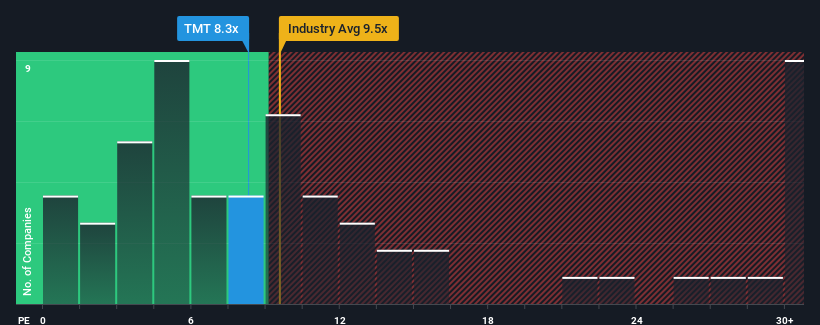

In spite of the firm bounce in price, it's still not a stretch to say that Trematon Capital Investments' price-to-earnings (or "P/E") ratio of 8.3x right now seems quite "middle-of-the-road" compared to the market in South Africa, where the median P/E ratio is around 10x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Recent times have been quite advantageous for Trematon Capital Investments as its earnings have been rising very briskly. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

View our latest analysis for Trematon Capital Investments

What Are Growth Metrics Telling Us About The P/E?

In order to justify its P/E ratio, Trematon Capital Investments would need to produce growth that's similar to the market.

Retrospectively, the last year delivered an exceptional 276% gain to the company's bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Comparing that to the market, which is predicted to deliver 16% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

With this information, we find it interesting that Trematon Capital Investments is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited recent growth rates and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as a continuation of recent earnings trends is likely to weigh down the shares eventually.

What We Can Learn From Trematon Capital Investments' P/E?

Its shares have lifted substantially and now Trematon Capital Investments' P/E is also back up to the market median. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Trematon Capital Investments revealed its three-year earnings trends aren't impacting its P/E as much as we would have predicted, given they look worse than current market expectations. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless the recent medium-term conditions improve, it's challenging to accept these prices as being reasonable.

Before you take the next step, you should know about the 5 warning signs for Trematon Capital Investments (1 is a bit concerning!) that we have uncovered.

You might be able to find a better investment than Trematon Capital Investments. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

If you're looking to trade Trematon Capital Investments, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Trematon Capital Investments might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:TMT

Excellent balance sheet second-rate dividend payer.

Market Insights

Community Narratives