Advertisement

- South Africa

- /

- Pharma

- /

- JSE:APN

Aspen Pharmacare Holdings Limited's (JSE:APN) CEO Compensation Is Looking A Bit Stretched At The Moment

Key Insights

- Aspen Pharmacare Holdings to hold its Annual General Meeting on 7th of December

- Salary of R9.17m is part of CEO Stephen Saad's total remuneration

- The overall pay is 148% above the industry average

- Aspen Pharmacare Holdings' EPS grew by 17% over the past three years while total shareholder return over the past three years was 57%

CEO Stephen Saad has done a decent job of delivering relatively good performance at Aspen Pharmacare Holdings Limited (JSE:APN) recently. As shareholders go into the upcoming AGM on 7th of December, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders will still be cautious of paying the CEO excessively.

Check out our latest analysis for Aspen Pharmacare Holdings

Comparing Aspen Pharmacare Holdings Limited's CEO Compensation With The Industry

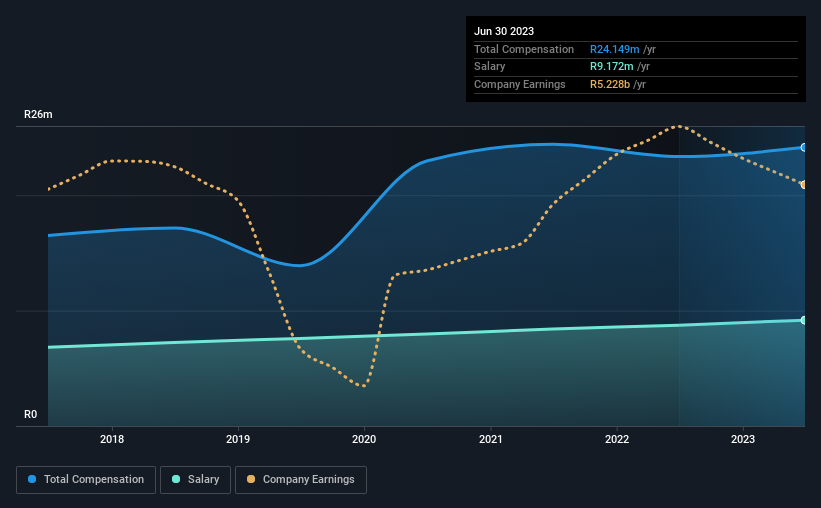

At the time of writing, our data shows that Aspen Pharmacare Holdings Limited has a market capitalization of R82b, and reported total annual CEO compensation of R24m for the year to June 2023. That's just a smallish increase of 3.4% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at R9.2m.

On examining similar-sized companies in the South Africa Pharmaceuticals industry with market capitalizations between R38b and R121b, we discovered that the median CEO total compensation of that group was R9.8m. Hence, we can conclude that Stephen Saad is remunerated higher than the industry median. What's more, Stephen Saad holds R11b worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | R9.2m | R8.7m | 38% |

| Other | R15m | R15m | 62% |

| Total Compensation | R24m | R23m | 100% |

On an industry level, roughly 56% of total compensation represents salary and 44% is other remuneration. In Aspen Pharmacare Holdings' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Aspen Pharmacare Holdings Limited's Growth

Aspen Pharmacare Holdings Limited has seen its earnings per share (EPS) increase by 17% a year over the past three years. Its revenue is up 5.4% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's nice to see revenue heading northwards, as this is consistent with healthy business conditions. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Aspen Pharmacare Holdings Limited Been A Good Investment?

Boasting a total shareholder return of 57% over three years, Aspen Pharmacare Holdings Limited has done well by shareholders. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

If you think CEO compensation levels are interesting you will probably really like this free visualization of insider trading at Aspen Pharmacare Holdings.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:APN

Aspen Pharmacare Holdings

Manufactures and supplies specialty and branded pharmaceutical products worldwide.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor