Advertisement

- South Africa

- /

- Metals and Mining

- /

- JSE:AMS

Anglo American Platinum Limited's (JSE:AMS) Fundamentals Look Pretty Strong: Could The Market Be Wrong About The Stock?

It is hard to get excited after looking at Anglo American Platinum's (JSE:AMS) recent performance, when its stock has declined 30% over the past three months. But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. Specifically, we decided to study Anglo American Platinum's ROE in this article.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Anglo American Platinum

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Anglo American Platinum is:

51% = R49b ÷ R97b (Based on the trailing twelve months to December 2022).

The 'return' refers to a company's earnings over the last year. That means that for every ZAR1 worth of shareholders' equity, the company generated ZAR0.51 in profit.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Anglo American Platinum's Earnings Growth And 51% ROE

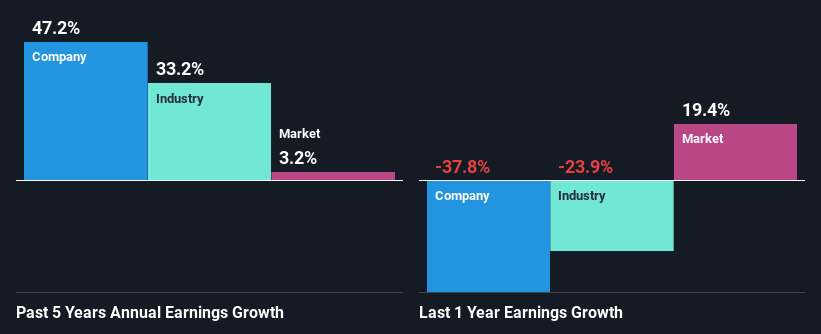

First thing first, we like that Anglo American Platinum has an impressive ROE. Secondly, even when compared to the industry average of 23% the company's ROE is quite impressive. As a result, Anglo American Platinum's exceptional 47% net income growth seen over the past five years, doesn't come as a surprise.

Next, on comparing with the industry net income growth, we found that Anglo American Platinum's growth is quite high when compared to the industry average growth of 33% in the same period, which is great to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about Anglo American Platinum's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Anglo American Platinum Efficiently Re-investing Its Profits?

The three-year median payout ratio for Anglo American Platinum is 40%, which is moderately low. The company is retaining the remaining 60%. This suggests that its dividend is well covered, and given the high growth we discussed above, it looks like Anglo American Platinum is reinvesting its earnings efficiently.

Additionally, Anglo American Platinum has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders. Looking at the current analyst consensus data, we can see that the company's future payout ratio is expected to rise to 63% over the next three years. Therefore, the expected rise in the payout ratio explains why the company's ROE is expected to decline to 22% over the same period.

Conclusion

In total, we are pretty happy with Anglo American Platinum's performance. In particular, it's great to see that the company is investing heavily into its business and along with a high rate of return, that has resulted in a sizeable growth in its earnings. Having said that, on studying current analyst estimates, we were concerned to see that while the company has grown its earnings in the past, analysts expect its earnings to shrink in the future. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:AMS

Anglo American Platinum

Engages in the production and supply of platinum group metals, base metals, and precious metals in South Africa, Asia, Europe, North America, and internationally.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|82.7% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|36.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|37.1% undervalued

UN

Community Contributor