- South Africa

- /

- Metals and Mining

- /

- JSE:AMS

Anglo American Platinum (JSE:AMS) Seems To Use Debt Rather Sparingly

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Anglo American Platinum Limited (JSE:AMS) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Anglo American Platinum

What Is Anglo American Platinum's Debt?

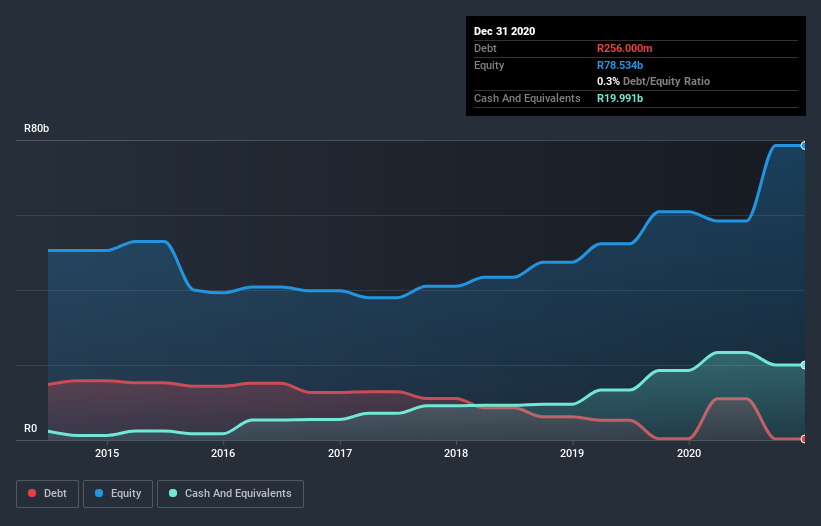

You can click the graphic below for the historical numbers, but it shows that Anglo American Platinum had R256.0m of debt in December 2020, down from R323.0m, one year before. However, it does have R20.0b in cash offsetting this, leading to net cash of R19.7b.

How Healthy Is Anglo American Platinum's Balance Sheet?

The latest balance sheet data shows that Anglo American Platinum had liabilities of R46.7b due within a year, and liabilities of R19.1b falling due after that. Offsetting this, it had R20.0b in cash and R6.95b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by R38.9b.

Given Anglo American Platinum has a humongous market capitalization of R564.4b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, Anglo American Platinum boasts net cash, so it's fair to say it does not have a heavy debt load!

On top of that, Anglo American Platinum grew its EBIT by 50% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Anglo American Platinum's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Anglo American Platinum may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, Anglo American Platinum recorded free cash flow worth 56% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

We could understand if investors are concerned about Anglo American Platinum's liabilities, but we can be reassured by the fact it has has net cash of R19.7b. And it impressed us with its EBIT growth of 50% over the last year. So is Anglo American Platinum's debt a risk? It doesn't seem so to us. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with Anglo American Platinum (at least 1 which shouldn't be ignored) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Anglo American Platinum or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About JSE:AMS

Anglo American Platinum

Engages in the production and supply of platinum group metals, base metals, and precious metals in South Africa, Asia, Europe, North America, and internationally.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Community Narratives