Advertisement

- South Africa

- /

- Food

- /

- JSE:CKS

We Think Some Shareholders May Hesitate To Increase Crookes Brothers Limited's (JSE:CKS) CEO Compensation

Key Insights

- Crookes Brothers' Annual General Meeting to take place on 30th of August

- CEO Kennett Sinclair's total compensation includes salary of R3.75m

- Total compensation is similar to the industry average

- Crookes Brothers' EPS declined by 0.9% over the past three years while total shareholder loss over the past three years was 24%

The underwhelming share price performance of Crookes Brothers Limited (JSE:CKS) in the past three years would have disappointed many shareholders. Per share earnings growth is also poor, despite revenues growing. The AGM coming up on 30th of August will be an opportunity for shareholders to have their concerns addressed by the board and for them to exercise their influence on management through voting on resolutions such as executive remuneration. We think shareholders may be cautious of approving a pay rise for the CEO at the moment, based on our analysis below.

Check out our latest analysis for Crookes Brothers

Comparing Crookes Brothers Limited's CEO Compensation With The Industry

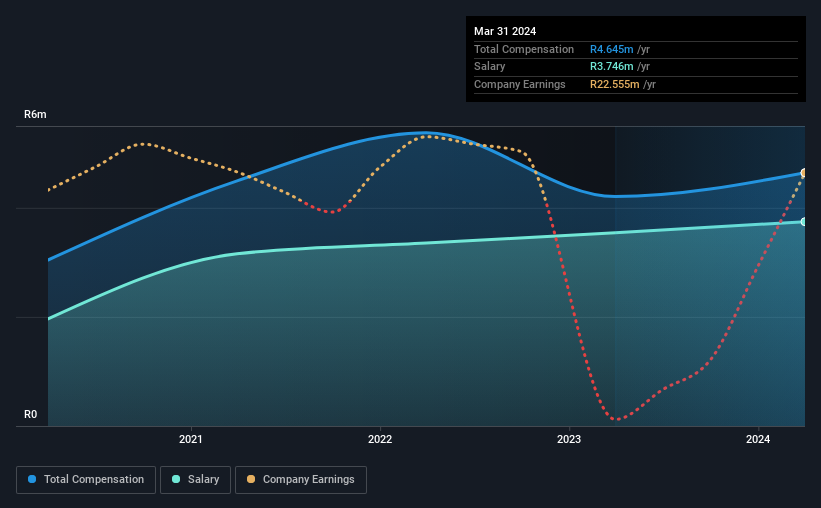

Our data indicates that Crookes Brothers Limited has a market capitalization of R465m, and total annual CEO compensation was reported as R4.6m for the year to March 2024. Notably, that's an increase of 10% over the year before. We note that the salary portion, which stands at R3.75m constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the South African Food industry with market capitalizations below R3.5b, reported a median total CEO compensation of R5.5m. This suggests that Crookes Brothers remunerates its CEO largely in line with the industry average. What's more, Kennett Sinclair holds R2.6m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | R3.7m | R3.5m | 81% |

| Other | R899k | R666k | 19% |

| Total Compensation | R4.6m | R4.2m | 100% |

On an industry level, around 46% of total compensation represents salary and 54% is other remuneration. Crookes Brothers is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Crookes Brothers Limited's Growth Numbers

Crookes Brothers Limited saw earnings per share stay pretty flat over the last three years. It achieved revenue growth of 18% over the last year.

The decrease in EPS could be a concern for some investors. But on the other hand, revenue growth is strong, suggesting a brighter future. It's hard to reach a conclusion about business performance right now. This may be one to watch. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Crookes Brothers Limited Been A Good Investment?

Since shareholders would have lost about 24% over three years, some Crookes Brothers Limited investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

The company's earnings haven't grown and possibly because of that, the stock has performed poorly, resulting in a loss for the company's shareholders. In the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan is in line with their expectations.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 3 warning signs for Crookes Brothers you should be aware of, and 1 of them shouldn't be ignored.

Switching gears from Crookes Brothers, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:CKS

Crookes Brothers

An investment holding company, engages in the agricultural business in South Africa, Eswatini, Zambia, and Mozambique.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

102 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative