Advertisement

The board of Famous Brands Limited (JSE:FBR) has announced that it will pay a dividend on the 22nd of July, with investors receiving ZAR1.64 per share. Despite the cut, the dividend yield of 7.4% will still be comparable to other companies in the industry.

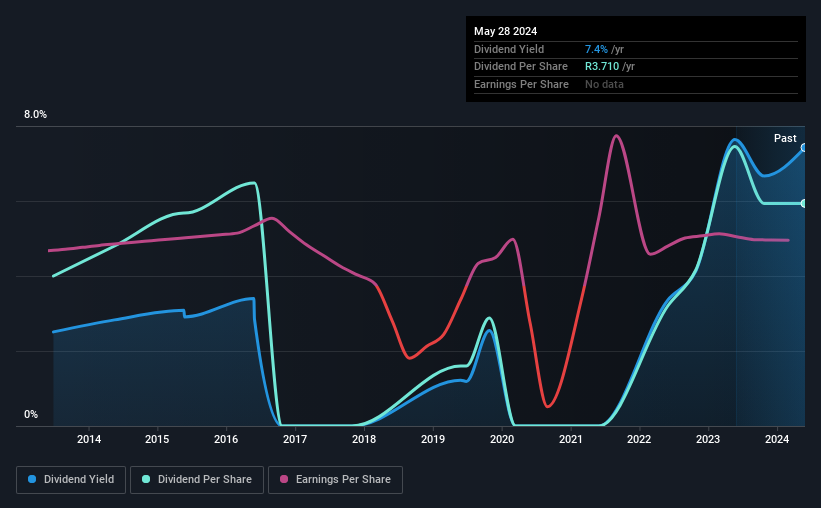

Check out our latest analysis for Famous Brands

Famous Brands' Payment Has Solid Earnings Coverage

Solid dividend yields are great, but they only really help us if the payment is sustainable. However, Famous Brands' earnings easily cover the dividend. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS could expand by 31.7% if recent trends continue. Assuming the dividend continues along recent trends, we think the payout ratio could be 49% by next year, which is in a pretty sustainable range.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was ZAR2.50 in 2014, and the most recent fiscal year payment was ZAR3.71. This implies that the company grew its distributions at a yearly rate of about 4.0% over that duration. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Famous Brands has seen EPS rising for the last five years, at 32% per annum. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

We Really Like Famous Brands' Dividend

Overall, we think that Famous Brands could be a great option for a dividend investment, although we would have preferred if the dividend wasn't cut this year. The cut will allow the company to continue paying out the dividend without putting the balance sheet under pressure, which means that it could remain sustainable for longer. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For example, we've picked out 2 warning signs for Famous Brands that investors should know about before committing capital to this stock. Is Famous Brands not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:FBR

Famous Brands

Through its subsidiaries, operates as a quick service and casual dining restaurant franchisor in the United Kingdom, South Africa, South African Development Community, Middle East, and Rest of Africa.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor