Advertisement

- United States

- /

- Renewable Energy

- /

- NYSE:VST

The Bull Case For Vistra (VST) Could Change Following Major Natural Gas Expansion and Battery Storage Focus

Simply Wall St

Reviewed by Simply Wall St

- Melius Research recently initiated coverage on Vistra Corp., spotlighting the company's 41 GW of diverse generation capacity and its recent acquisition of seven natural gas plants from Lotus Infrastructure Partners.

- An important highlight is Vistra’s ownership of the Moss Landing energy storage complex, one of the world’s largest battery storage systems, signaling its leadership in grid-scale storage innovation.

- We'll now explore how Vistra's expansion of its natural gas portfolio could influence its investment outlook and growth potential.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Vistra Investment Narrative Recap

For investors to be long-term shareholders in Vistra, they need to believe that rising electricity demand from data centers, AI, and manufacturing will support sustained utilization of its generation assets, while disciplined capital allocation and a diverse portfolio help manage risks. The recent acquisition of seven natural gas plants from Lotus Infrastructure Partners further diversifies Vistra's fleet and expands its scale, but it does not materially alter the near-term importance of keeping leverage in check or ease the pressure from elevated debt, which remains the biggest risk.

Among recent announcements, the update on share buybacks stands out: Vistra has repurchased more than 163.9 million shares for US$5.38 billion, retiring over 40 percent of total shares since the program began. This ongoing return of capital underscores the company's commitment to shareholder value and provides incremental support to its investment narrative amid growth initiatives such as the latest natural gas portfolio expansion.

In contrast, investors should still be aware of the lingering risks tied to high leverage and potential refinancing pressures, especially if credit markets shift unexpectedly...

Read the full narrative on Vistra (it's free!)

Vistra's outlook anticipates $24.5 billion in revenue and $3.4 billion in earnings by 2028. This projection assumes a 9.8% annual revenue growth and a $1.2 billion increase in earnings from the current $2.2 billion level.

Uncover how Vistra's forecasts yield a $218.24 fair value, a 11% upside to its current price.

Exploring Other Perspectives

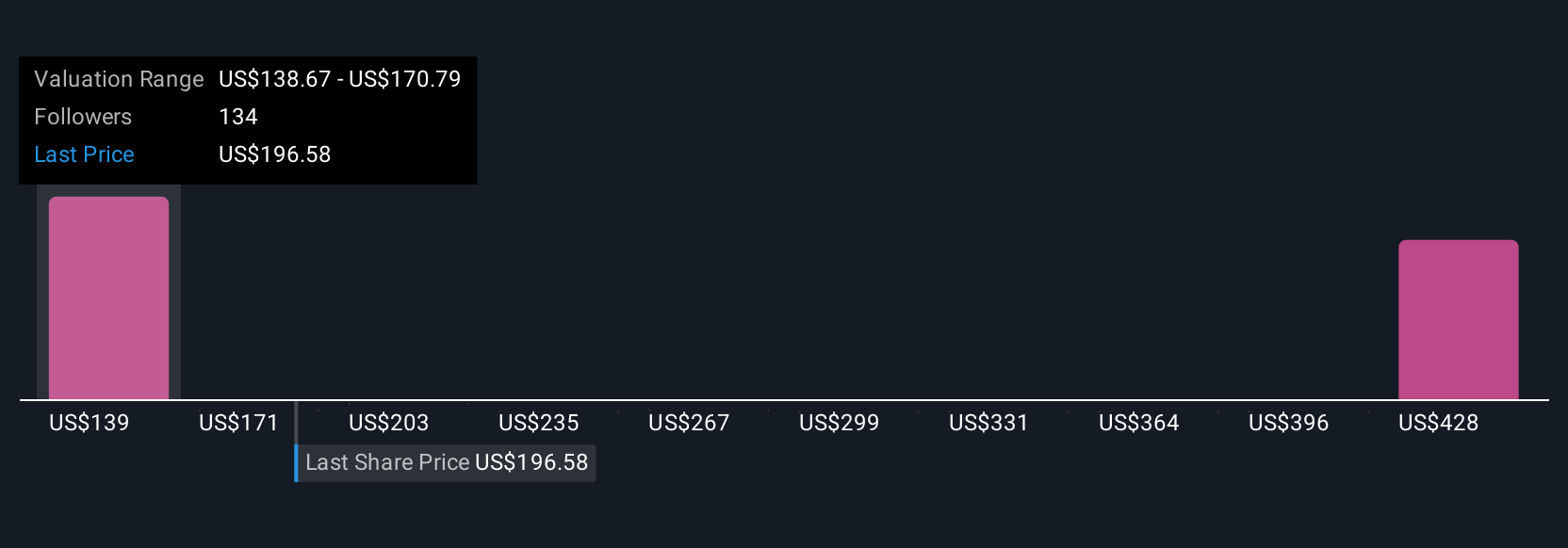

Fifteen Simply Wall St Community members estimate Vistra’s fair value from US$138.67 to US$384.22, with varied views on growth. While opinions differ widely, Vistra’s debt-fueled expansion continues to shape investor debates over risk and long-term resilience.

Explore 15 other fair value estimates on Vistra - why the stock might be worth 30% less than the current price!

Build Your Own Vistra Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Vistra research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Vistra research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vistra's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VST

Vistra

Operates as an integrated retail electricity and power generation company in the United States.

Solid track record and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|50.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|8.5% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|18.4% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor