- United States

- /

- Other Utilities

- /

- NYSE:NI

What Do Recent Gains and Dividend Growth Mean for NiSource’s Share Price in 2025?

Reviewed by Bailey Pemberton

If you are looking at NiSource and wondering whether now is the time to buy, hold, or reconsider, you are not alone. The stock has been delivering some impressive returns, up 3.1% in just the past week, adding another 2.4% for the month, and a robust 18.5% so far this year. Looking further back, the one-year return is a striking 27.9%, and over the past five years, the shares have surged a remarkable 129.0%. This strong momentum has certainly caught the eye of investors seeking both stability and growth potential within the utilities sector.

What stands out even more is how consistently these gains have been accumulated, despite broader market volatility and shifts in investor sentiment around defensive stocks like utilities. Since utilities stocks often serve as a safe haven during uncertain times, the continued strength in NiSource may reflect a broader rethinking of the company's growth prospects and risk profile by market participants.

However, impressive returns can sometimes obscure the true value of a business. When NiSource is evaluated using widely-used valuation measures, the company does not qualify as undervalued, earning a value score of zero out of six. That may be surprising, especially after such a noteworthy run. So how should NiSource's current price really be evaluated? Next, let’s break down the major valuation approaches and explore an alternative method to gauge the stock’s underlying value that you may not have considered.

NiSource scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: NiSource Dividend Discount Model (DDM) Analysis

The Dividend Discount Model (DDM) is a valuation method focused on estimating a stock's intrinsic value by projecting future dividends and discounting them back to the present. This approach is especially relevant for companies in stable sectors such as utilities, where steady and predictable dividend payments are common.

For NiSource, the most recent data shows an annual dividend per share of $1.25, with a dividend payout ratio of 61.6%. The company's return on equity stands at about 9.13%, and dividend growth is projected to be roughly 3.1% per year. These figures suggest a company that is prioritizing consistent returns to shareholders, relying on gradual earnings growth to sustain future dividend hikes.

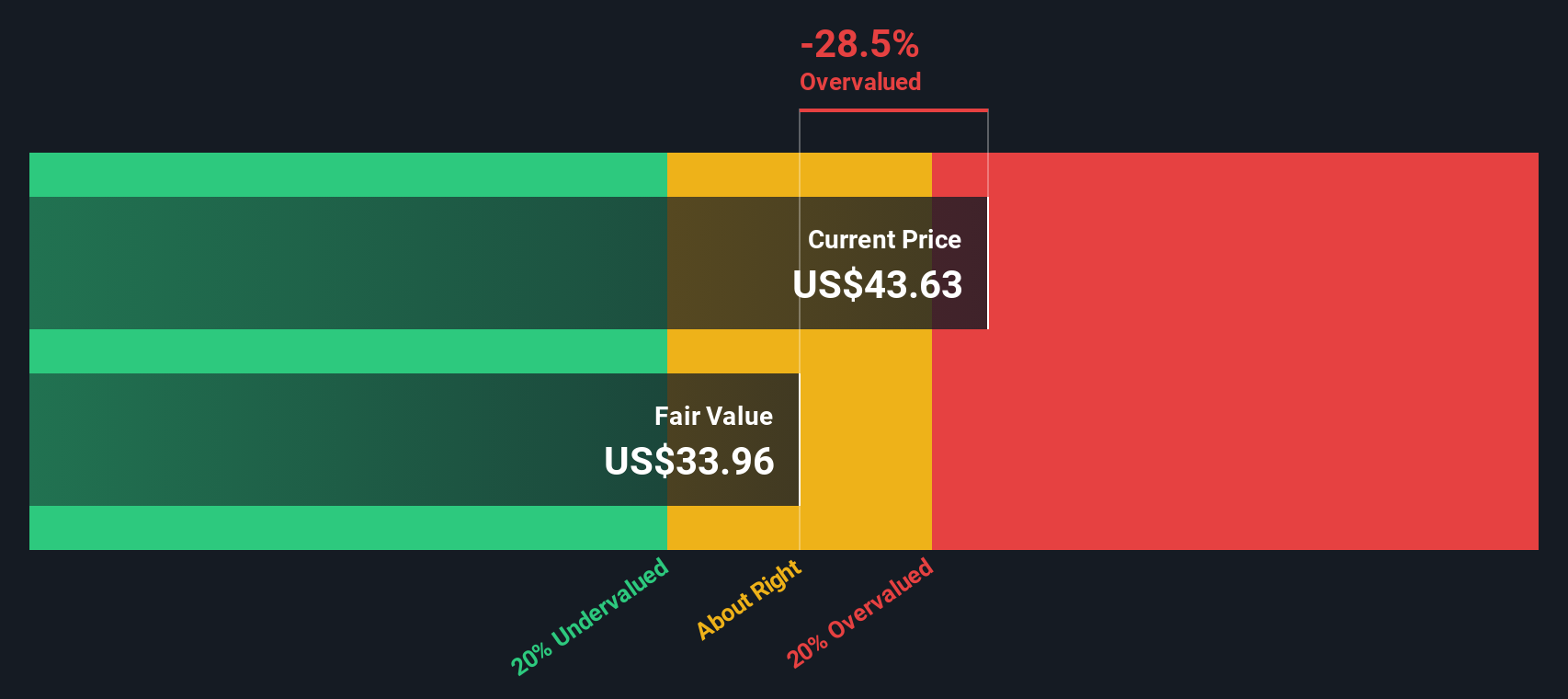

Based on these dividend projections and growth expectations, the DDM estimates NiSource's intrinsic value at $33.80 per share. However, when compared to the current market price, this implies the stock is roughly 27.5% above its fair value as calculated by this model. This indicates that at today’s price, NiSource is trading at a premium to what is justified by its long-term dividend prospects alone.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests NiSource may be overvalued by 27.5%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: NiSource Price vs Earnings Analysis

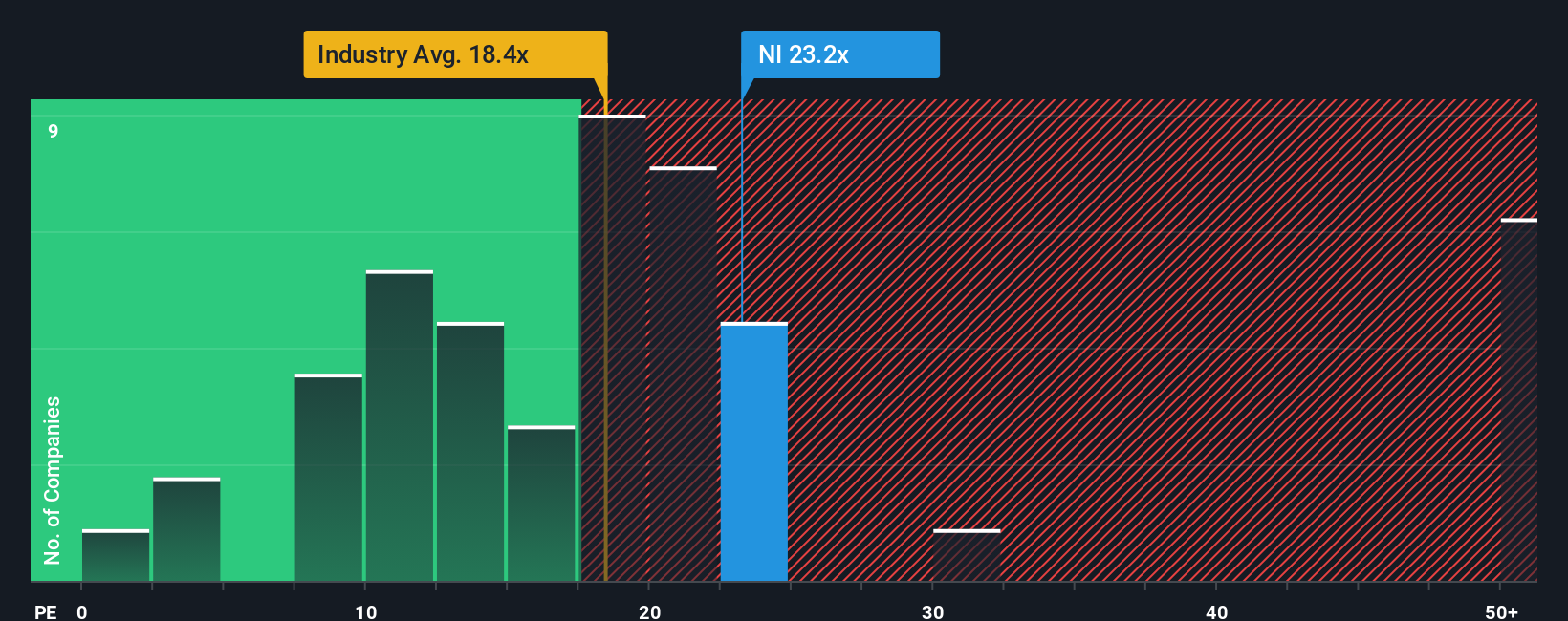

For profitable companies like NiSource, the price-to-earnings (PE) ratio is a widely used metric for valuation. It offers a simple way to assess how much investors are willing to pay for each dollar of earnings, and is especially effective for mature businesses generating consistent profits. Investors commonly rely on this ratio to compare similar companies and gauge whether a stock looks expensive or cheap relative to its earnings power.

It is important to note, though, that what qualifies as a “normal” or “fair” PE ratio depends on several factors. Companies expected to grow earnings faster, or that carry less risk, can justify higher PE ratios. Likewise, businesses in more cyclical or higher-risk industries might trade at a discount, since their earnings could be less reliable over time.

Currently, NiSource trades at a PE ratio of 22.9x. That figure is above the Integrated Utilities industry average of 18.2x, and slightly higher than its direct peers, which average 22.2x. To provide more context, Simply Wall St’s proprietary “Fair Ratio” model incorporates not only these benchmarks, but also NiSource’s unique combination of earnings growth potential, profit margins, risks, and market cap. According to this metric, the fair multiple for NiSource is 20.3x. Based on underlying fundamentals rather than just peer comparison, the stock is assigned a somewhat lower multiple than where it currently trades.

Because NiSource’s PE ratio is moderately above its Fair Ratio, this suggests the market is pricing in a bit too much optimism. With fundamentals taken into account, the stock appears somewhat expensive using this valuation method.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your NiSource Narrative

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story or perspective about a company. It's where you connect your own assumptions about NiSource's future revenue, earnings, and profit margins to a fair value estimate that captures your unique outlook.

Narratives go beyond crunching the numbers; they let you clearly spell out what you think will drive the company's success or risks, then link those beliefs directly to a forecast and a sensible price for the stock. You don’t need to be an expert. Simply Wall St’s platform makes Narratives an easy and accessible tool, allowing millions of investors to create, share, and update their views right from the Community page.

The power of Narratives comes from their flexibility and transparency. You can see in real time how any updates, such as new earnings results or important news, automatically adjust your valuation and investment stance. By comparing the Fair Value that results from your Narrative to NiSource’s current share price, you can quickly decide whether the stock looks attractive or if it might be time to wait.

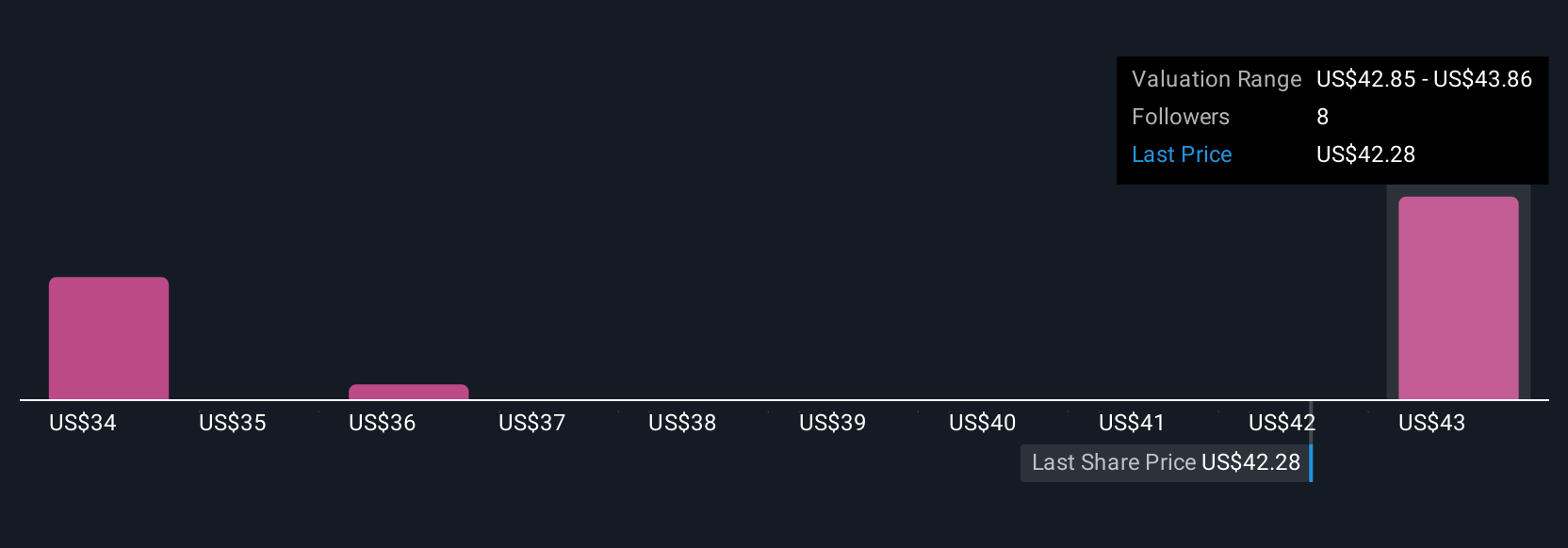

For example, some investors see strong growth from grid modernization projects and set a Fair Value of $46.00, while others focus on regulatory risks and use $36.00 instead.

Do you think there's more to the story for NiSource? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NiSource might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NI

NiSource

An energy holding company, operates as a regulated natural gas and electric utility company in the United States.

Proven track record second-rate dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Positioned to Win as the Streaming Wars Settle

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion